Editor’s note: This post was updated on April 19, 2013, to reflect an error in the referenced study on debt levels by Carmen Reinhart and Ken Rogoff.

Editor’s note: This post was updated on April 19, 2013, to reflect an error in the referenced study on debt levels by Carmen Reinhart and Ken Rogoff.

In the last few days, while the US political debate centers on ways to deal with burgeoning debt, UK government debt has been downgraded and investors are demanding much higher yields on Italian debt in the wake of the Italian election results (paywall). As concerns about national credit ratings push economies around the world toward austerity–government spending cuts and tax hikes–some commentators are still calling for economic stimulus at any cost. Joe Weisenthal wrote that David Cameron must spend more money in order to save the British economy. Paul Krugman wrote in “Austerity, Italian Style” that austerity policies simply don’t work. The downside of their prescription of more spending—and perhaps lower taxes—is that it would add to the United Kingdom’s and to Italy’s national debt.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

And despite the recent revelation of errors in Carmen Reinhart and Ken Rogoff’s famous study of debt levels and economic growth, which I discuss here and which motivated the update you are reading (the original passage can be found here), there are reasons to think that high levels of debt are worth worrying about.

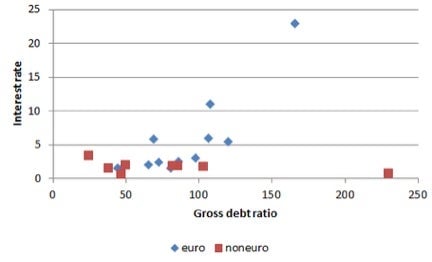

First, for a country like Italy that does not have its own currency (since it shares the euro with many other countries), Paul Krugman’s own graph shows a correlation between national debt as a percentage of GDP and the interest rate that a country pays.

Second, the paper by Thomas Herndon, Michael Ash and Robert Pollin that criticizes Reinhart and Rogoff finds that, on average, growth rates do decline with debt levels. Divide debt levels into medium high (60% to 90% of GDP), high (90% to 120% of GDP), and very high (above 120% of GDP). Then the growth rates are 3.2% with medium-high debt, 2.4% with high debt, and 1.4% with very high debt. (I got these numbers by combining the 4.2% growth rate for countries in the 0 to 30% debt-to-GDP ratio range from Table 3 with the estimates in Table 4 for how things are different at higher debt levels.) Moreover, contrary to the impression one would get from the column here, Herndon, Ash and Pollin’s Table 4 indicates that the differences between low levels of debt and high levels of debt are not just due to chance, though what Herndon, Ash and Pollin emphasize is that very low levels of debt, below 30% of GDP, have a strong association with higher growth rates. Overall, with the data we have, we don’t know what causes what, so there is no definitive answer to how much we should worry about debt, but ample reason not to treat debt as if it were a nothing.

In an environment in which stimulus is needed, but extra debt is a problem, there should be a laser-like focus on the ratio of stimulus any measure provides relative to the amount of debt it adds. In every one of my proposals for stimulating the economy, I have been careful to avoid proposals that would make a large addition to national debt. So I do not follow Joe Weisenthal and Paul Krugman in their recommendations.

First, instead of raising spending or cutting taxes, the Italian and UK governments can directly provide lines of credit to households, as I have proposed for troubled euro-zone countries and for the UK, as well as for the US. Although there would be some loan losses, the better ratio of stimulus to the addition to the national debt would lead to a much better outcome. In particular, after full economic recovery in the short run, there would be much less debt overhang to cause long-run problems after such a national lines of credit policy than under Weisenthal’s or Krugman’s prescriptions.

But for the UK, it is an even more important mistake to think that monetary policy can’t cut short-term interest rates below zero. Weisenthal quotes a post on Barnejek’s blog, “Has Britain Finally Cornered Itself?” that illustrates the faulty thinking I’m talking about:

Before I start, however, I would like to thank the British government for conducting a massive social experiment, which will be used in decades to come as a proof that a tight fiscal/loose monetary policy mix does not work in an environment of a liquidity trap. We sort of knew that from the theory anyway but now we have plenty of data to base that on.

“Liquidity trap” is code for the inability of the Bank of England to lower interest rates below zero. The faulty thinking is to treat the “liquidity trap” or the “Zero Lower Bound,” as modern macroeconomists are more likely to call it, as if it were a law of nature. The Zero Lower Bound is not a law of nature! It is a consequence of treating money in bank accounts and paper currency as interchangeable. As I explain in a series of Quartz columns (1, 2, 3 and 4) and posts on my blog—that is a matter of economic policy and law that can easily be changed. As soon as paper pounds are treated as different creatures from electronic pounds in bank accounts, it is easy to keep paper pounds from interfering with the conduct of monetary policy. In times when the Bank of England needs to lower short-term interest rates below zero, the effective rate of return on paper pounds can be kept below zero by announcing a crawling peg “exchange rate” between paper pounds and electronic pounds that has the paper pounds gradually depreciating relative to electronic pounds.

In his advice for the UK, Weisenthal should either explain why having an exchange rate between paper pounds and pounds in bank accounts is worse than a massive explosion of debt or join me in tilting against a windmill less tilted against. And for those who read Krugman’s columns, it would take a bad memory indeed not to recall that he gives the corresponding advice of stimulus by additional government spending for the US, which faces its own debt problem. I hope Paul Krugman will join me too in attacking the Zero Lower Bound.

In 1896 William Jennings Bryan famously declared: “… you shall not crucify mankind on a cross of gold.”

In our time it is not gold that is crucifying the world economy (though some would return us to the problems that were caused by the gold standard), but the unthinking worldwide policy of treating paper currency as interchangeable with money in bank accounts. So for our era, let us say: You shall not crucify humankind on a paper cross.