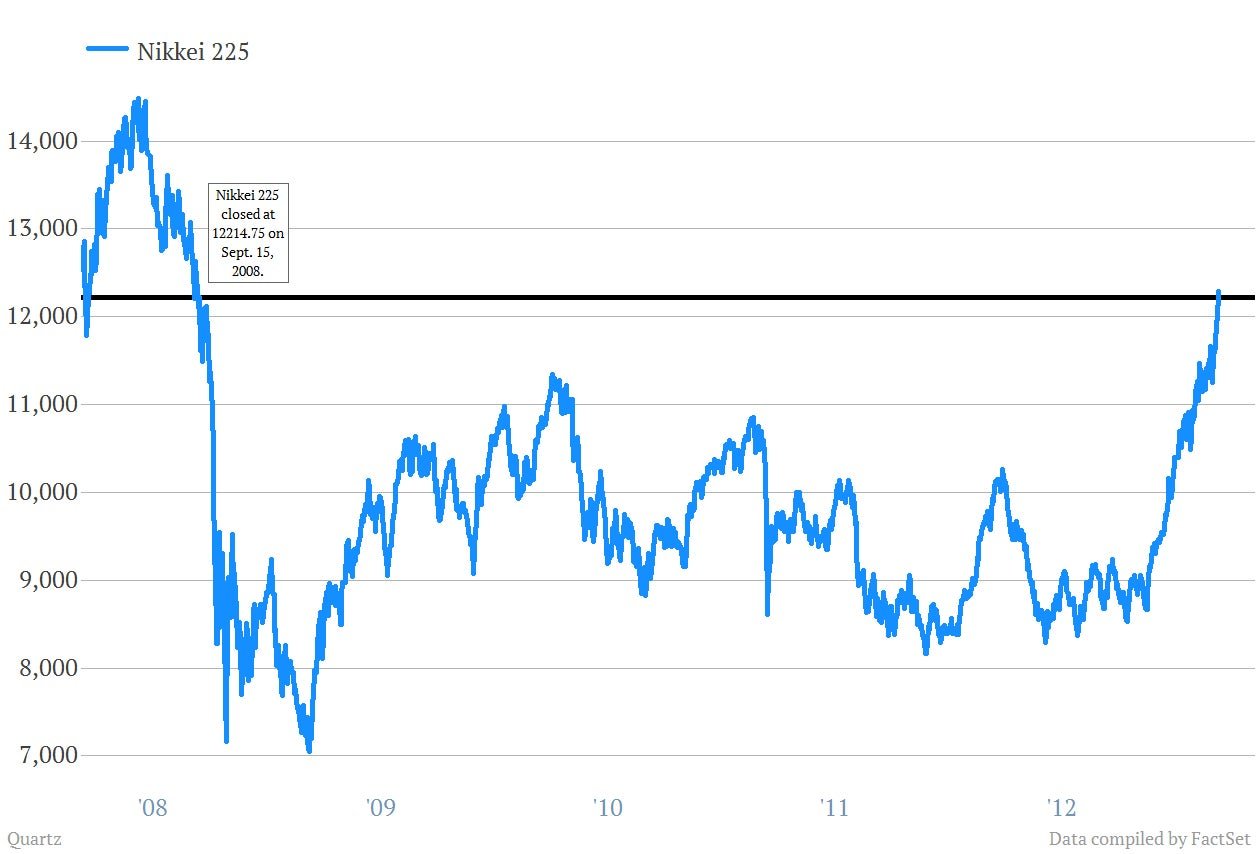

Nobody knows if Abenomics will be able to defeat the deflationary dragon Japan has been fighting for decades. But Prime Minister Shinzo Abe’s single-minded push toward an activist monetary policy is already having an effect. Just look at the stock market: Year-to-date it’s up 18%, roughly doubling the S&P 500’s 8.5% gain over the same period. Today’s 2.6% gain helped the Nikkei 225 regain territory it hasn’t seen since the collapse of Lehman Brothers back in 2008. Take a look:

Nobody knows if Abenomics will be able to defeat the deflationary dragon Japan has been fighting for decades. But Prime Minister Shinzo Abe’s single-minded push toward an activist monetary policy is already having an effect. Just look at the stock market: Year-to-date it’s up 18%, roughly doubling the S&P 500’s 8.5% gain over the same period. Today’s 2.6% gain helped the Nikkei 225 regain territory it hasn’t seen since the collapse of Lehman Brothers back in 2008. Take a look:

Now, cynics can pooh-pooh the run-up of Japanese stocks as just another example of a central bank’s promise of money printing pushing asset prices higher—and they’d be right. But they’d also be missing the point. The crash of the Japanese stock market was an important psychological domino that sent the Japanese economy into its downward spiral, :

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

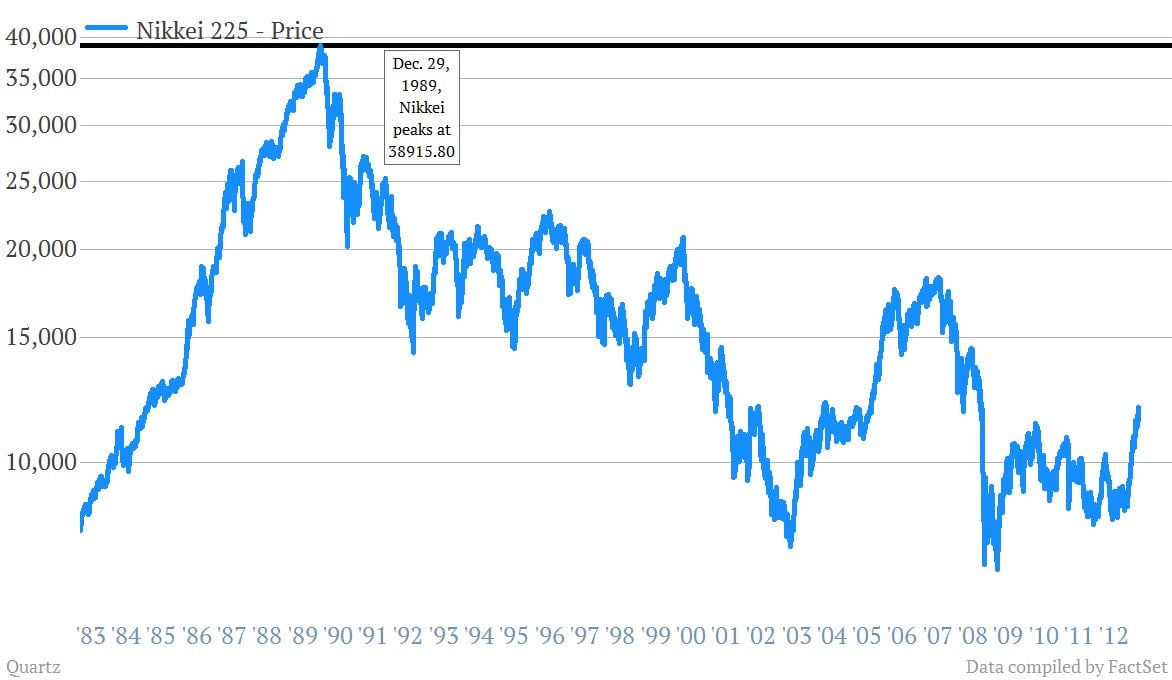

Japan’s Great Recession was, of course, preceded by a dramatic collapse of its stock market, which fell by over 60 percent between the start of 1990 and the end of 1991. Stock market losses and lower land prices eventually accumulated to a wealth loss in Japan of ¥15 trillion, which is about three years’income. That is substantial and should, perhaps, suggest some empirical evidence with respect to the wealth effect, because a shortage of demand has been a critical and chronic problem in Japan, as evidenced by its accelerating deflation

The current rally not withstanding, Japan’s stock market remains ridiculously depressed more than 20 years after the initial crash. As of Friday’s close the Japanese index remains roughly 68% lower than Nikkei’s peak of 38915.80 on Dec. 29, 1989. Ouch. If Abenomics shows progress in turning asset prices around, that will be an important step towards drastically altering Japan’s deflationary psychology.