If you lend somebody money, they have to pay you back with interest.

If you lend somebody money, they have to pay you back with interest.

This is the basic premise of all finance, from street corner loan sharks to Wall Street loan sharks.

Bonds are sort of like loans—except you can trade them. Normally, if you buy a bond, the issuing government or corporation agrees to pay you interest. They don’t always make those payments—they default, go bankrupt, etc.—but that’s the way things are supposed to work.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

No longer. With central banks pushing the limits of their ability to stoke growth, interest rates on many bonds are in negative territory, effectively turning the core rule of finance on its head. When investors buy bonds with negative interest rates, they’re agreeing to pay a borrower to take their money.

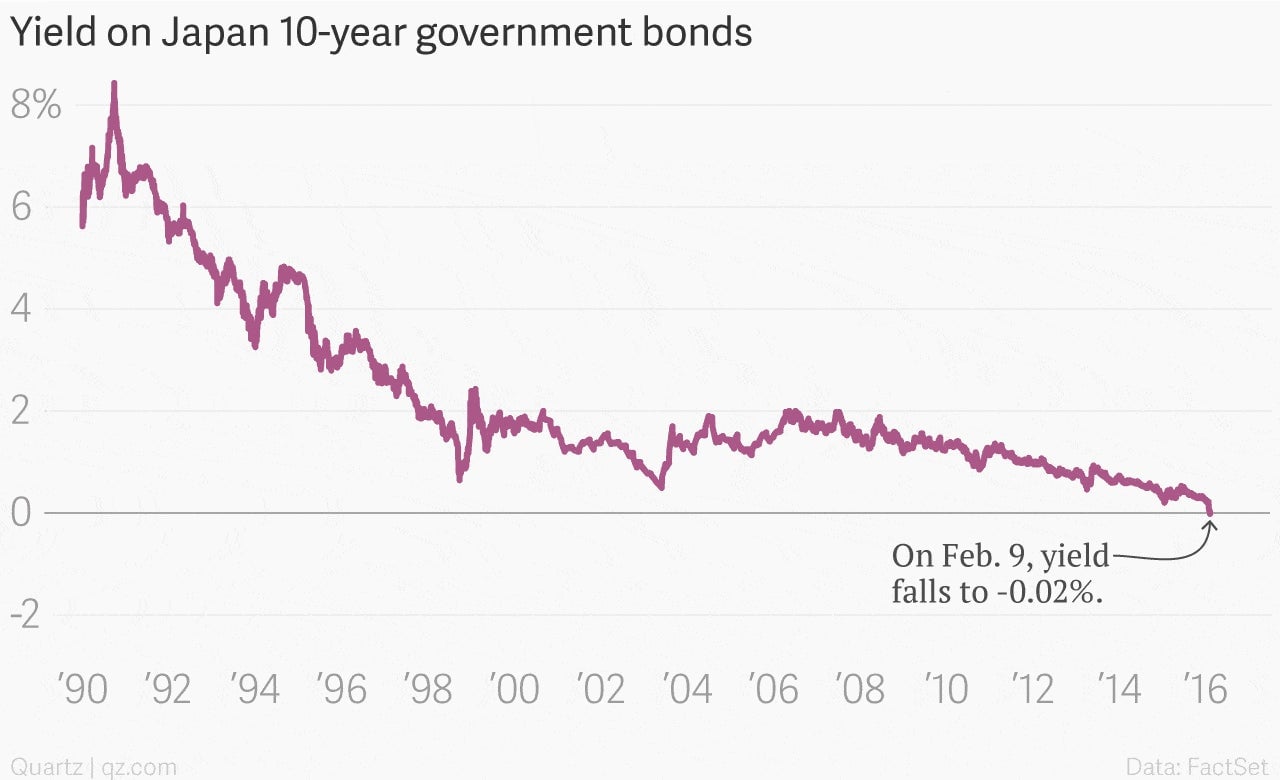

While odd, this is now the situation for large swaths of the market for government bonds. Central banks in the euro zone, Sweden, Switzerland, and Denmark have all pushed their benchmark short-term interest rates into negative territory. That’s rippled out to longer-term bonds. For instance, yields on German government bonds that mature over the next seven years are negative. Swiss 10-year bonds offer negative yields. And after the Bank of Japan moved to negative short-term yields earlier this year, the yield on the Japanese 10-year note fell into negative territory Tuesday (Feb. 9).

On the face of it, paying someone to borrow your money seems like a bad idea. But it isn’t, necessarily. Why? Deflation.

Generally speaking, interest rates on bonds are fixed. (That’s why bonds are called “fixed income” instruments.) For the most part, they don’t account for changes in prices. So an investor who is expecting prices to decline can buy a bond with a negative interest rate, and still expect to make a return in “real,” that is price-adjusted, terms.

Moreover, currency fluctuations can also turn bonds with negative interest rates into profitable investments. For example, say the yen appreciates strongly against the dollar. That appreciation could be enough to turn a bet on a negative-yielding Japanese government bond into a positive yielding investment, at least for a US-based investor.

Oh, one other thing to know: bonds that pay very low yields tend to have higher interest rate sensitivity—what bond geeks call duration. That means very small movements in interest rates generate big swings in the price of a bond. Since bond returns are a combination of price swings—capital appreciation—and interest payments, you can still make money on a bond with a negative interest rate if the price gets a nice pop. (This is basically what’s been happening lately due to the global markets meltdown.)

In fact, paying people to borrow your money has been a pretty good trade so far this year.

In US dollar terms, buying an index of Japanese government bonds or Swiss government bonds has returned more than 6% so far in 2016. That’s far better than a rather ugly 9% decline—including dividends—that investors got from investing in the US stock market.

So paying a borrower to take your money isn’t a sucker’s bet after all. At least not lately.