Although Cyprus may be a tiny country and an offshore Russian tax haven, the implications for the rest of the euro area of the plan to bail out its banks by imposing a levy on depositors are very real.

It all has to do with how Greece’s bailout was handled last year. In February 2012, EU leaders and the IMF agreed to allow Greece a “managed default,” giving it more aid only as long as private investors agreed to take a 68.5% writedown on their holdings of Greek debt. But bonds bought by the public sector—European countries, the European Central Bank (ECB), and the IMF, collectively known as the “troika”—would have to be honored, even if they were purchased at a price less than face value. These organizations will not only be repaid, they actually stand to make money on some of those investments.

Analysts generally agree this wasn’t handled well. It set an uneasy precedent, signaling that private sector investors would bear the full brunt of any default wherever the troika got involved in buying sovereign debt. EU leaders recognized that this was a bad model, and was hurting other countries on aid programs, so they vowed that Greece’s situation was “unique” and would not be repeated elsewhere.

EU leaders have made a concerted effort to do things differently this time. They’re not forcing Cyprus to default. They’re also dealing with Cypriot banks, not holders of Cypriot government debt. Instead, they’re forcing all private depositors—both rich and poor—in the country’s banks to pay a one-time tax that would bring down the country’s debt level. (Cyprus’s parliament may try to soften the blow to smaller depositors when it meets tomorrow.)

But trying to get away from the Greek precedent, European leaders are doing something that might be equally as bad: risking bank runs. Essentially, it’s like getting rid of deposit insurance; if there’s any possibility that your money won’t be there when you want it, why put it in a bank that’s subject to any risk? The FT’s Wolfgang Münchau points out that hitting small-time investors in Cyprus has collateral effects on small-time investors (paywall) elsewhere in peripheral Europe:

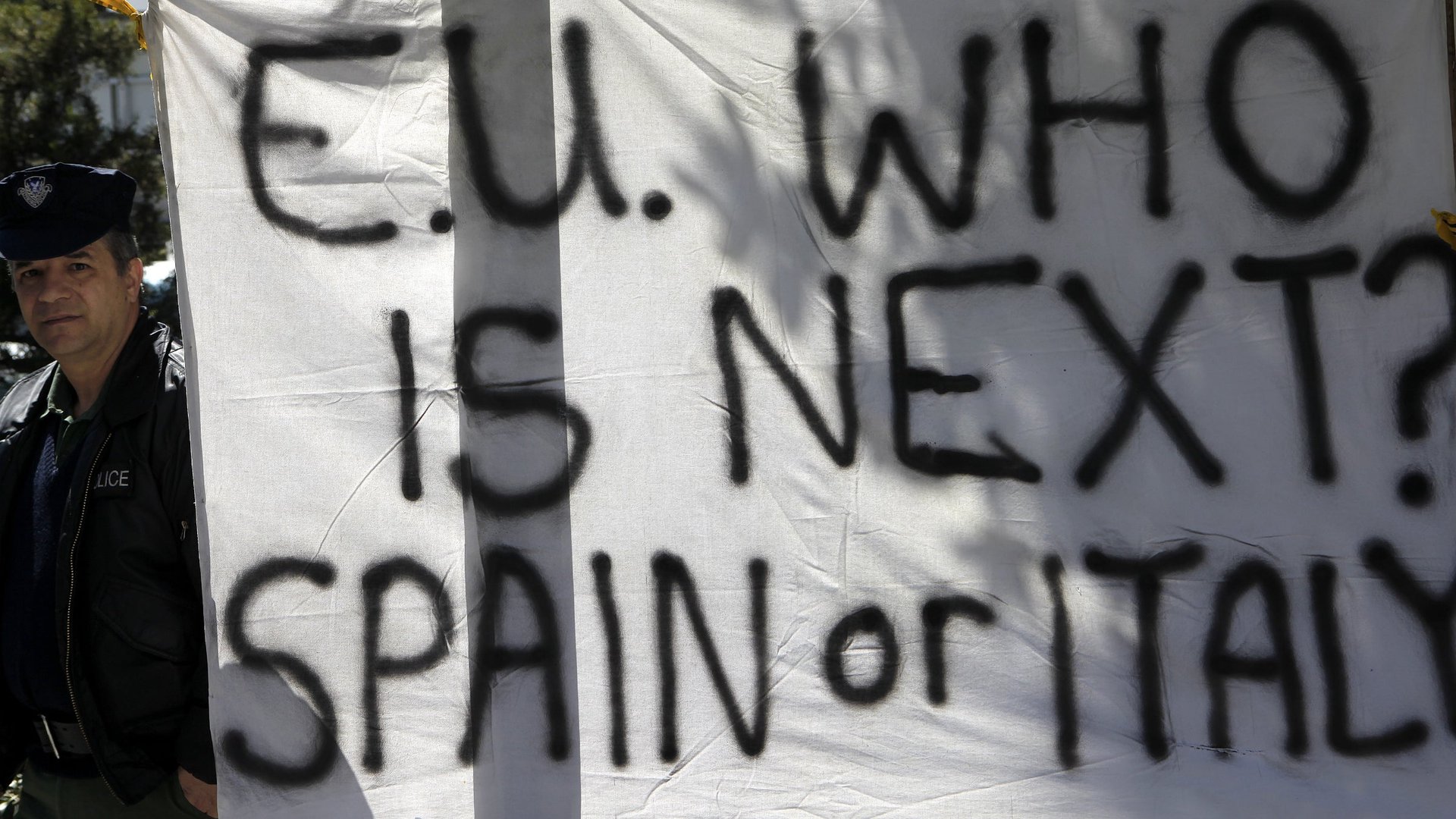

Unless there is a last-minute reprieve for small savers, most Cypriot savers would act rationally if they withdrew the rest of their money simply to protect them from further haircuts or taxes. It would be equally rational for savers elsewhere in southern Europe to join them. The experience of Cyprus tells them that the solvency of a deposit insurance scheme is only as good as that of the state. In view of Italy’s public sector debt ratio, or the combined public and private sector indebtedness of Spain and Portugal, there is no way that these governments can insure all banks’ deposits on their own.

The Cyprus rescue has shown that the creditor nations will insist from now that any bank rescue must be co-funded by depositors.

For that reason, banks in Cyprus are closed today, and will remain shut through Wednesday, according to the Wall Street Journal.

It also shows that the poorly managed Greek scenario is not unique, write Morgan Stanley $MS analysts; whether it’s depositors or sovereign bondholders, the private sector will once again bear the full burden of some kind of debt restructuring:

Although the levy on Cypriot deposits may be a ‘unique’ action due to the particular characteristics of its banking sector, investors may take that as a new template for countries with similar challenges. In other words, levy on deposits for countries with oversized banking sector and PSI countries with sovereign leverage…

The Cypriot taboo-breaking solution of hitting depositors takes us further along the road of new ways to spare taxpayers’ money.

It may be that just as they tried to avoid repeating the exact formula they used in Greece, Europe’s leaders will not allow a carbon-copy repeat of Cyprus. In particular, political turmoil risks reflating concerns about the stability of the massive Spanish and Italian economies. Cyprus’s bailout establishes a pattern of trying to make private investors in a country stomach all the pain of its restructuring. That reduces their incentive to keep money in peripheral European banks or invested in struggling countries’ sovereign bonds—which weakens the countries further and makes their need for a bailout even more likely. So although EU leaders have deviated from the Greek plan, the Cypriot solution really isn’t much better at inspiring confidence.