Few have watched the development of the Chinese economy as closely as Arthur Kroeber.

Few have watched the development of the Chinese economy as closely as Arthur Kroeber.

His new book, published last month, is a wide-ranging and authoritative primer on the history and development of China’s unique blend of decentralized economic authoritarianism.

It’s an idiosyncratic system, developed in defiance of the advice of western-trained economists in the wake of the collapse of the Soviet Union. And it generated perhaps the world’s greatest-ever economic boom, a three-decade stretch of growth that lifted roughly .

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

As editor of China Economic Quarterly, and managing director at respected research firm Gavekal Dragonomics, Kroeber watched as that growth transformed the People’s Republic into the world’s second largest economy.

More recently, China has transformed again. It is now the world’s No. 1 economic concern, amid widespread evidence of slowing growth, capital flight, and a worrisome rise in debt. And it’s the topic of Kroeber’s new book, China’s Economy: What Everyone Needs to Know.

Kroeber, also a non-resident senior fellow at the Brookings-Tsinghua Center, splits his time between Beijing and New York. He recently stopped by Quartz’s New York office to explain China’s surging debt, to tell us why the People’s Republic won’t have a classic emerging market crisis, and to warn us about the risk of China becoming a new, poorer version of a sclerotic Japan. Here are edited excerpts from our conversation.

Quartz: The basic recipe for Chinese growth, until recently, was to take hundreds of millions of people from the countryside and move them to cities, where China built thousands and thousands of factories, roads, ports, and infrastructure.

But you write that the recipe doesn’t really work anymore. Why is that?

Arthur Kroeber: I think there are two reasons why it doesn’t work anymore. One is that when you’re in that phase of growth, a lot of what you’re doing is building the enabling infrastructure. So you’re not just building the factories. You’re building the housing. You’re building the roads. You’re building the power plants. You’re building the ports. You’re building the airports.

You’re building a lot of stuff.

That’s right. And eventually you get to the point where you don’t really need to build any more of that stuff. You can continue to grow your economy without additional power plants or that additional port. You can just use [what you have] more efficiently.

And it doesn’t actually help to build a third power plant when you’re already getting enough power from the first two.

Yeah that’s exactly right. So, part of the growth over the last 30 years was building all the infrastructure. And that job isn’t completely done. But it’s done enough so that it becomes a much much smaller part of the equation.

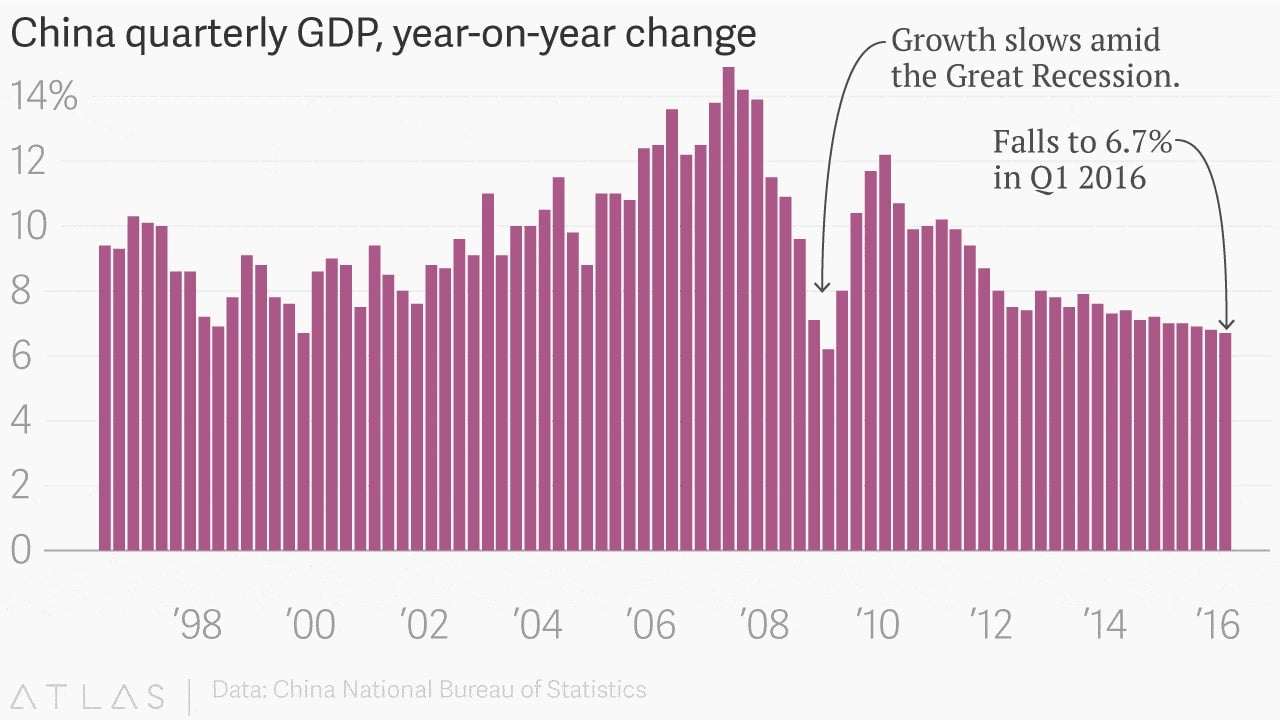

So is that why China’s GDP growth has slowed down? They’re still building a lot of infrastructure as we speak, but those large projects don’t generate the GDP pop that they used to?

Well I think there’s a couple ways you can look at this. The simplest way is to say that for 30 years roughly, from 1980 until four or five years ago, China was growing at about 10% a year on average. And roughly speaking, half of that growth came from the creation of new capital—new roads, new ports, etc. And the other half of that came, essentially, from productivity growth.

So you take someone off the farm where he’s producing a value of maybe $300 a year, and you put him into a factory and automatically he’s producing $3,000 a year. So you get a huge productivity jump.

And that by the way is the classic story of economics, whether it’s a Scottish guy going to work in the textile mills of northern England in the 19th century or an American farmer moving to Pittsburgh to work in a steel mill.

Exactly. Now we’re at a point where because you built all this capital, you have basically the capital stock that you need. You can’t get five points of growth by adding capital. It just doesn’t produce that much value.

So you lose roughly speaking half of your growth, because half of it was simply capital accumulation. And you probably lose a little bit of the productivity too, because eventually you get to the point where you moved everyone off the farm and into factories.

So you have a natural evolution where China is at the stage where it’s just impossible to keep growing at 10% a year. And all of the growth that you get, essentially, has to come from using your resources better rather than throwing new resources into the system.

One of the things that I thought was really helpful about your book was that you talk about China’s rising debt load—its debt-to-GDP ratio. And you say this is clear evidence that the economy can’t grow just by adding more infrastructure. Can you explain that a little bit?

So the point is that China had a pretty stable debt-to-GDP ratio fro a long time. But over the last few years its gone up really fast it’s gone up from 140% of GDP to 240% in seven years.

And that’s always a warning sign. If it rises very rapidly in a short period of time, that is almost always a sign that something is wrong. Because it’s very unusual—it’s almost impossible—for an economy to suddenly double its capacity to carry that much debt. So likely what’s going on is that a lot more debt is going into less and less productive investments.

And so the debt rises very quickly, but GDP—which is a function of productivity—is growing much more slowly.

When we drill down into the corporate sector data, it becomes very obvious where the problem is. Starting in 2008, if you look at the return-on-assets among industrial companies, you see that there is a severe deterioration among state-owned companies. And this basically has to do with the global financial crisis and the Chinese response to it.

One of the things I learned from your book was just how massive China’s fiscal response to the crisis was.

It was by far the biggest fiscal stimulus in the world.

In the US we did a stimulus but it was politically very difficult to get it through, because there was a lot of the political spectrum which was just ideologically opposed to increased government spending.

In China, which is a government-driven, command economy, there was no one to say, “Oh no, we don’t think the government should spend money.” So they just poured it on. And it was a reasonable thing to do, because everyone was scared. No one know exactly what was going on.

And they had the money.

And they were facing a very serious problem. In the year after the financial crisis, China’s exports fell by 20%. There were over 20 million workers in export-oriented factories who lost their jobs. Twenty million, in the space of a few months.

So from the Chinese government’s perspective they said look, “We’ve got a huge problem. We’re just going to pour in as much money as we can to finance infrastructure and housing and anything to get some demand going. And yeah that could create a mess, but we can clean that up later.”

The problem was that, because of the nature of the Chinese system, the way they did it was not by the government spending they money. Instead, they told the banks, “Go and lend to your friendly, local, state-owned enterprise, as much money as they want, for whatever they want to do.”

That’s the quickest way to get money out the door.

But it’s not a recipe for productive investment.

Some of the money did go into productive infrastructure. It was reasonably well spent. There was just too much of it.

And it really strengthened the state-owned enterprises, and brought to a halt the process that had been going on for 10 or 15 years of gradually reducing the role of the state sector.

My sense of the gloomy scenario for China’s debt problems isn’t a Lehman-style financial crisis brought on by excess debt. It looks to me that the risk would be a Japanese-style lost decade.

I think that is the biggest concern right now. Some people have looked at China and said, “This debt is out of control, there’s an attack on the currency. This looks like an emerging market financial crisis, like Brazil in the 1980s or the Southeast Asian economies in the 1990s. This could end very badly, very quickly, in a big financial crisis.”

That’s superficially plausible. But it doesn’t really hang together. And the basic reason is that the country doesn’t really have any external debt. All the debt is domestic and that’s very similar to Japan.

And also unlike places like Thailand and Brazil, which were running big current account deficits, China runs a huge current account surplus, so they can always generate the foreign exchange that they need to keep the foreign creditors at bay. And they have have a lot of resources to keep things from blowing up.

So, for instance their giant cash stockpile of foreign exchange reserves.

Yeah. The likelihood that China would just blow up in the classic emerging-market crisis, with a financial system blow-up, is not likely.

What is much more likely is that they end up in a situation comparable to what Japan got into in the early 1990s, where you have this huge unproductive debt problem and basically the banks become technically insolvent. But you don’t want to admit that.

So, you have zombie banks, zombie companies, but the government has enough money to sort of keep everyone afloat.

And you can wind up in a situation, which is basically what Japan got to, which is that there’s this very, very high debt level, and growth that has gone down to a very low level because most of this debt is going into totally unproductive stuff, and you basically have no way to get out of that.

The problem in Japan is you had this sort of cozy relationship between the government and the banks and the companies, and no one really wanted to shake things up too much.

For China, the issues are similar. You’ve got this comfortable arrangement between the government and the state-owned enterprises, they don’t want to change that. To get productivity growth, they’d really have to take an axe to the state-owned enterprise sector and allow much more private-sector activity. That’s scary if you’re the Communist Party. You think, “Can I actually hang onto power if there’s all this private wealth being created that I can’t control? Maybe this is politically too dangerous. Maybe it’s just safer to keep things tightly controlled.”