A spate of new analysis of global bank stocks by global banks suggests that their business models are in trouble—and that shareholders might want to break them up for that reason. Not because the banks are too risky, they say, but because regulators aren’t letting them take enough risk. While the average investor seeking to avoid a systemic crisis might consider less risk a good thing, it’s a problem for bank heads who want pre-2008 profits in a post-2008 world.

A spate of new analysis of global bank stocks by global banks suggests that their business models are in trouble—and that shareholders might want to break them up for that reason. Not because the banks are too risky, they say, but because regulators aren’t letting them take enough risk. While the average investor seeking to avoid a systemic crisis might consider less risk a good thing, it’s a problem for bank heads who want pre-2008 profits in a post-2008 world.

First, a JP Morgan analysis of bank stocks was reported in the New York Times:

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

“We see Tier I investment banks as un-investable. The viability of running a global Tier I investment bank business as part of a universal banking business is starting to be put in question.”

Then, this Bloomberg story on a Wells Fargo $WFC analysis of the largest US banks, the stocks of which are trading below book value in many cases, suggesting investors would make out better if they were broken up:

“Given the challenges posed by increasing regulation, higher capital requirements, and well-publicized trading/market challenges, it’s not surprising that investors remain reluctant to assign a ‘full’ valuation to the universal banks. If regulators and/or legislators don’t demand it, shareholders could also intensify demands to ‘break up the banks.’ ”

Finally, the Financial Times shares this more positive Morgan Stanley $MS/Oliver Wyman analysis (pdf) of global big banks:

“We think the industry and the market have yet to get to grips with the forces fracturing global wholesale banking. In particular we now anticipate a 2-3% point drag on RoE from regulatory Balkanisation. … With diverging national regulatory agendas, it poses a major risk to the global banking model.”

All the reports blame post-financial crisis regulation for these problems. Is that a fair claim? Here’s what we can take away.

Yes, regulation is working. Aside from giving regulators better views of the financial system and more tools to shut down failing banks, the best the architects of the US Dodd-Frank reforms could hope to achieve against the Too Big To Fail problem was to make it too expensive to be a huge global bank. And what these reports are saying is that, indeed, it is becoming more expensive to be a huge global bank that carries lots of risk. Whether or not society needs huge global banks is a question for another day, but if breaking up large banks might now be in the interest of shareholders, the bank reform crowd should see that as a win.

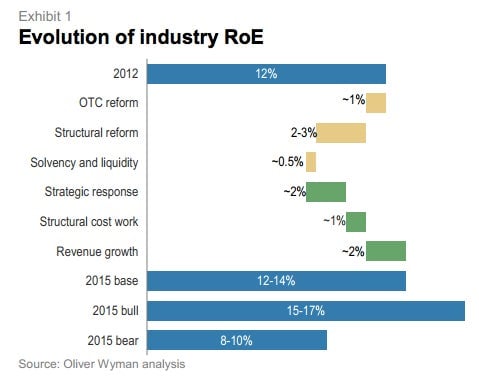

But it’s not because of equity and capital requirements. This is an interesting chart from the Oliver Wyman report, which estimates how regulatory costs (yellow) and business decisions (green) affect their forecasts for banks’ return on equity, or RoE. (It also shows the predicted RoE for 2015 as against that for 2012.)

If you look at the costs, the biggest comes from structural reform, like the Volcker Rule that prohibits proprietary trading. The second biggest cost is from “OTC reform,” which refers to requirements that banks clear derivatives through central exchanges. The third, “solvency and liquidity,” refers to the new rules for equity and liquidity reserves in Basel III—a regulatory change about which banks have complained loudly. This has had the lowest impact of all, although admittedly banks are still only about 60% of the way to meeting the new standards.

Which might mean that regulation isn’t working. If equity requirements are costing banks so little, it suggests that either critics are right that they are too weak, or that banks are too good at getting around them. Banks are coming up with new trades that allow them to maintain the assets on their books while shifting the risk off the books, reducing the impact of new equity and reserve requirements.

Some argue that this is a good thing. It pushes risk away from insured institutions and towards independent money managers. But this “collateral transformation” may be just disguising risk. The Morgan Stanley report notes that this kind of work is one of the bright spots in banking in the next few years, potentially generating $5-$8 billion in revenue. But like many responses to regulation at financial institutions, it raises the question of what business exactly banks are in—efficiently directing capital, or regulatory arbitrage?

But don’t feel too bad. The projections for 12%-14% return on equity in 2015 would put the biggest global banks around the average for US businesses, which is 12.89%. And that’s a good deal higher, according to NYU finance professor Aswath Damodaran, than the average RoE for American banks, of 7.46%.