Under its new governor, Haruhiko Kuroda, the Bank of Japan has not only become a lot more aggressive; it’s also acting a lot more bullish.

Under its new governor, Haruhiko Kuroda, the Bank of Japan has not only become a lot more aggressive; it’s also acting a lot more bullish.

As expected, in its policy meeting announcement today (pdf) the bank added nothing to the bold program of “quantitative and qualitative“ easing (QE) it announced on April 4, after Kuroda took over. But it did update its economic projections for the next few years. And though QE—the biggest of the three pillars of Abenomics, prime minister Shinzo Abe’s plan to break 15 years of deflationary trends—hasn’t even gotten off the ground yet, the bank is already projecting big improvements:

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

The reasons for the revisions are QE, an upturn in financial market conditions, and fiscal stimulus, said the BoJ report. “Japan’s economy has stopped weakening and has shown some signs of picking up,” the bank wrote, adding “it is expected to return to a moderate recovery path around mid-2013.”

That’s big. The Japanese economy grew exactly not at all in the last quarter of 2012. The inflation estimates, too, are way more optimistic than they were under former BoJ governor Masaaki Shirakawa.

However, the BoJ also projected that inflation will hit only 1.9% by April 2016, shy of the 2% inflation target it just adopted. That underscores that QE will be around for a long time.

As FT Alphaville points out, these forecasts rest atop some big assumptions that obscure exactly how QE alone is supposed to work. But the idea here is to alter expectations, as we recently discussed. Talking a big game like this should, in theory, encourage Japanese businesses and consumers to be confident in economic growth, so that they start spending to keep up with it.

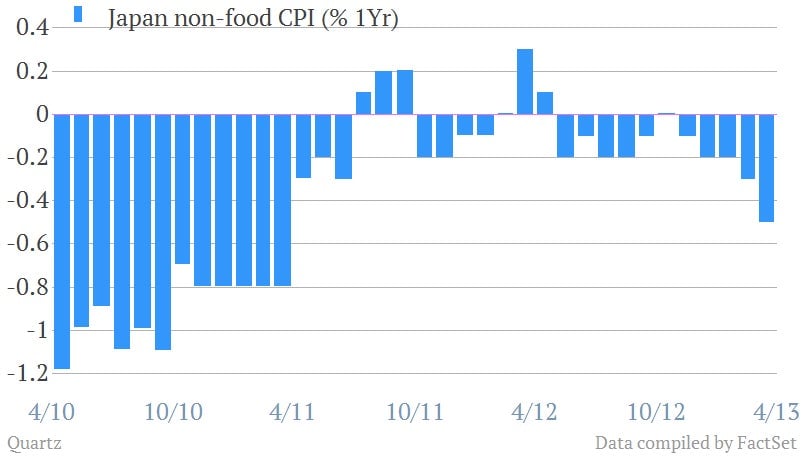

However, this will be no mean feat, as inflation data out today show. Deflation got worse in March, as core CPI shrank 0.5% year-on year, having fallen 0.3% in February. (And recall that Japan’s “core” CPI measure includes energy, the imports of which have been rising). Here’s a look at that trend:

Turning that into 0.7% price growth within a year from now, as the latest projections call for, is going to be tricky. However, Tokyo’s inflation number for April also came out today, and, as the Financial Times highlights, that’s seen as a leading indicator (paywall). Core CPI in Tokyo fell only 0.3% year-on-year in April, after having shrunk 0.5% in March. That sign, along with rising profitability of Japanese companies and the fact that aggressive asset-purchasing begins in earnest only in May (pdf), are reminders that it’s still way too early to be reading much into CPI data.