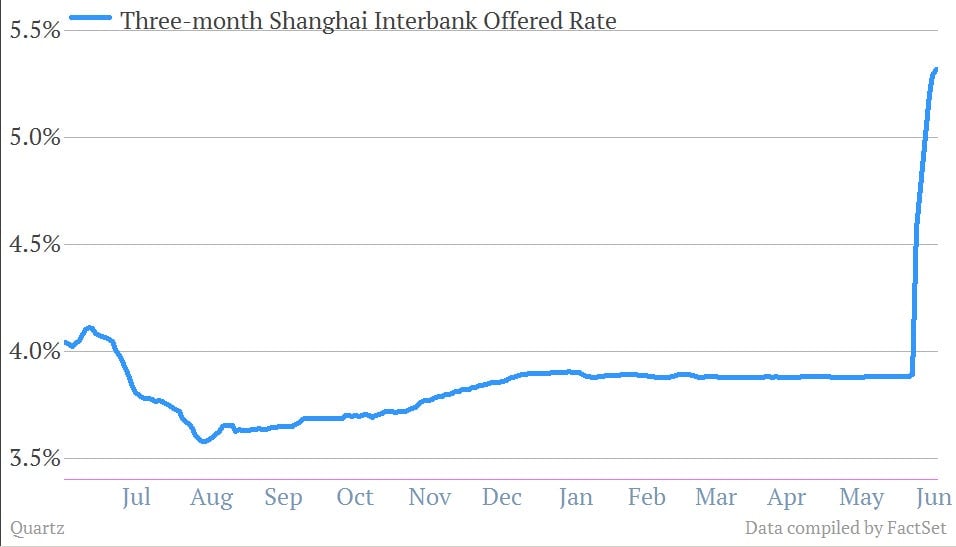

Remember Libor? When that once obscure measure of short-term interest rates shot higher in 2007 and 2008, it was one of the earliest warnings signs of what would eventually become the financial crisis. Now, its Chinese cousin—known as Shibor—is telegraphing the rising stress in the opaque financial system of the world’s second largest economy. Behold:

What does the spike in rates mean? Large banks are increasingly leery of tapping into their pools of cash to lend to each other. Recent reports that China Everbright Bank failed to repay a short-term loan to Industrial Bank Co. aren’t helping. Industrial Bank says that report is “untrue and exaggerated.” But short-term lending markets suggest other bankers are skeptical.

So what’s the solution? Chinese authorities tamed short-term interest rate spikes before. They could create new cash to lubricate lending, or lower reserve requirements for banks, which would boost liquidity. According to the Wall Street Journal, that’s what bankers are hoping for.

But remember, those reserves are supposed to protect Chinese banks against losses from bad loans. (And there are plenty of bad loans floating around in the Chinese banking system.) So both of those solutions would actually just be a bandaid to reduce short-term rates; they would do little to reduce the underlying systemic risks. Stay tuned.