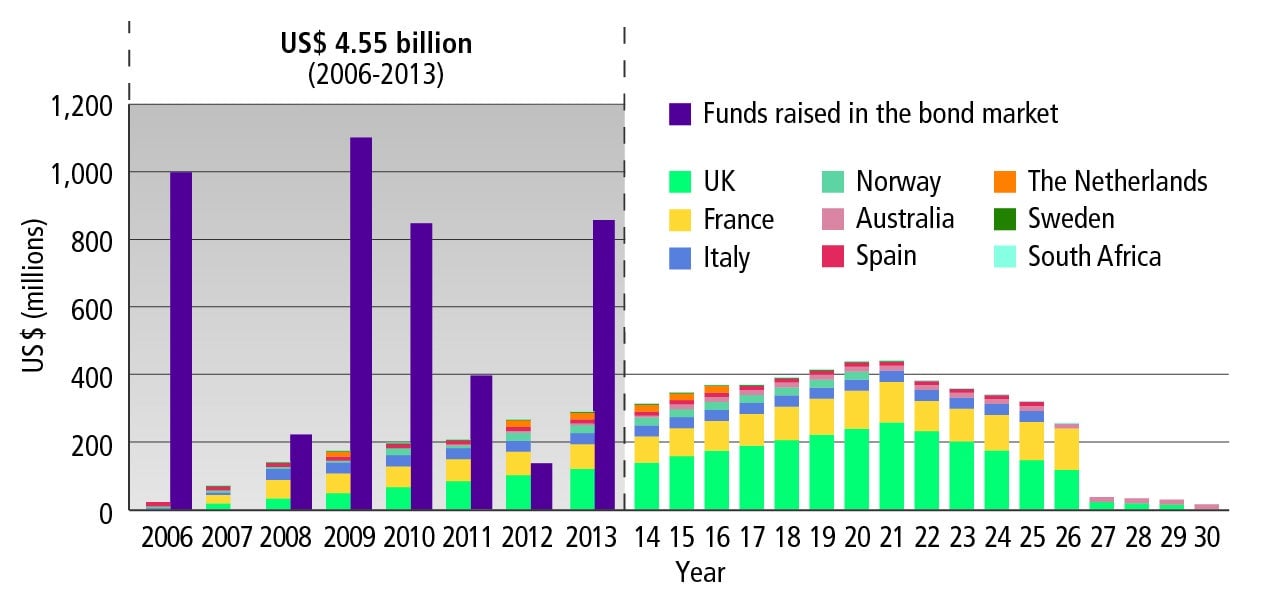

How to invest in a vaccine

With the help of nine countries, GAVI set up the International Finance Facility for Immunisation. IFFIm is a structured-finance vehicle, like the mortgage-backed securities that blew up the economy in 2008. In this case, the intent isn’t to turn tomorrow’s mortgage payments into cash today, but to turn future donations into vaccines today. The cash flow comes from long-term donation contracts, often twenty years or more, signed by the nine nations, including the UK, South Africa, and Australia.