This is an updated version of an article first published on Sept. 26, 2013.

This is an updated version of an article first published on Sept. 26, 2013.

The US Postal Service (USPS) has made it official: Anybody who wants to turn a quick profit at its expense will have an opportunity to do so come January.

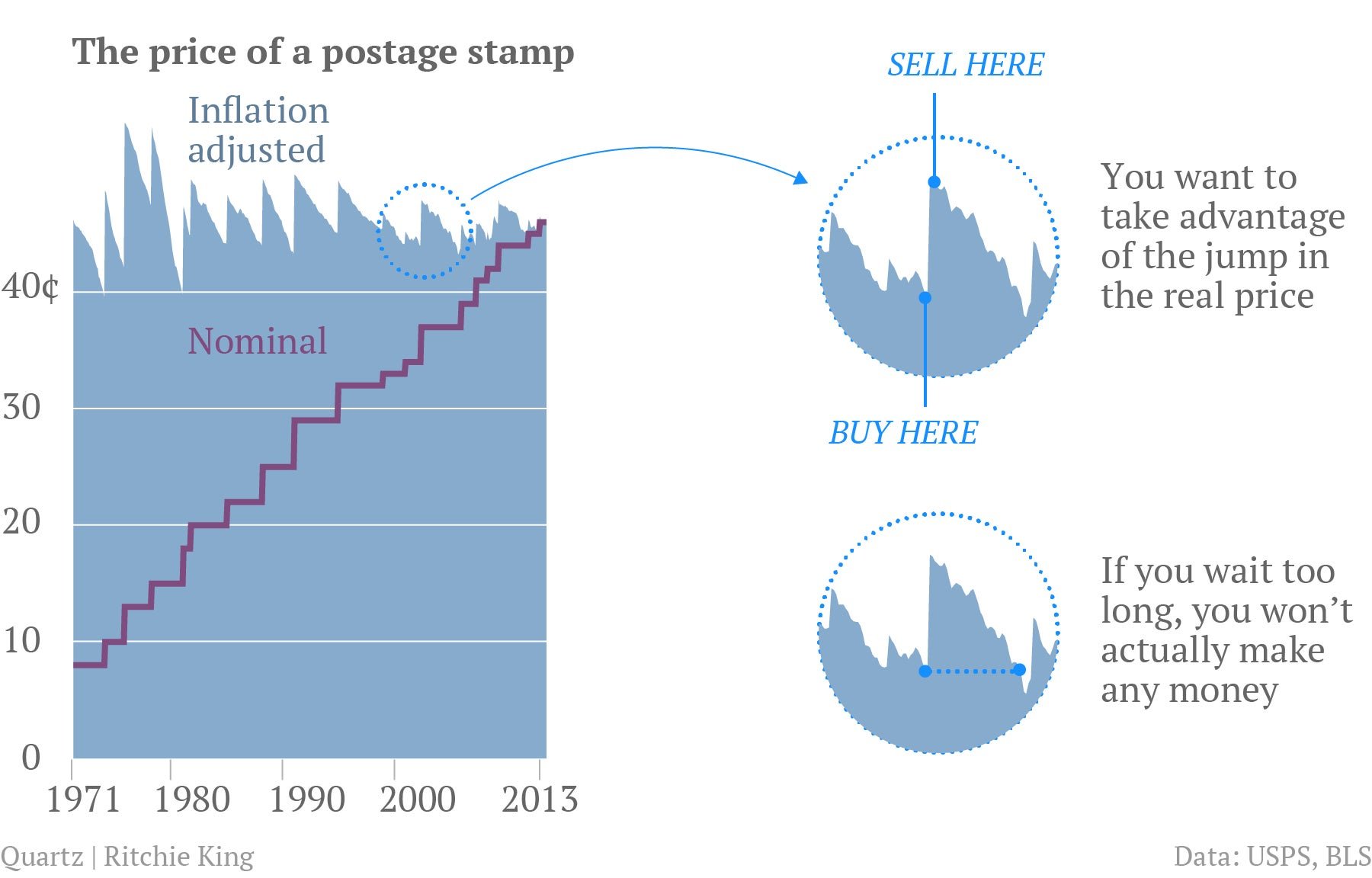

As of January 26 next year, it will hike the price of a first-class stamp from $0.46 to $0.49. Stamp prices are normally increased by about 1 or 2 cents a year to match inflation. This 3-cent increase, by the US Postal Regulatory Commission, is large enough that it creates an opportunity for arbitrage in so-called “forever” stamps, which hold their value regardless of changes in postage price. (The Postal Regulatory Commission stressed that the increase would be temporary, to be phased out in less than two years, when the Postal Service has made up the $2.8 billion it lost during the recession.)

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Before forever stamps were introduced in 2007, all stamps in the US were denominated. In other words, the price paid was printed on the stamp. If the stamp was old, and the denomination was less than the current cost of postage, then a letter-mailer would have to supplement it with smaller stamps to make up the difference. A forever stamp can be used, well, forever.

So what’s stopping stamp peddlers from buying up forever stamps at $0.46 before the price hike on Jan. 26, 2014, and selling them afterwards at a profit for less than $0.49?

We hashed out a hypothetical plan to see whether forever-stamp arbitrage is worth it.

First of all, timing is key. It’s best to buy the stamps right before the price increase, and flip them shortly afterwards. The longer you hang onto the stamps, the less you make in real terms, because of inflation:

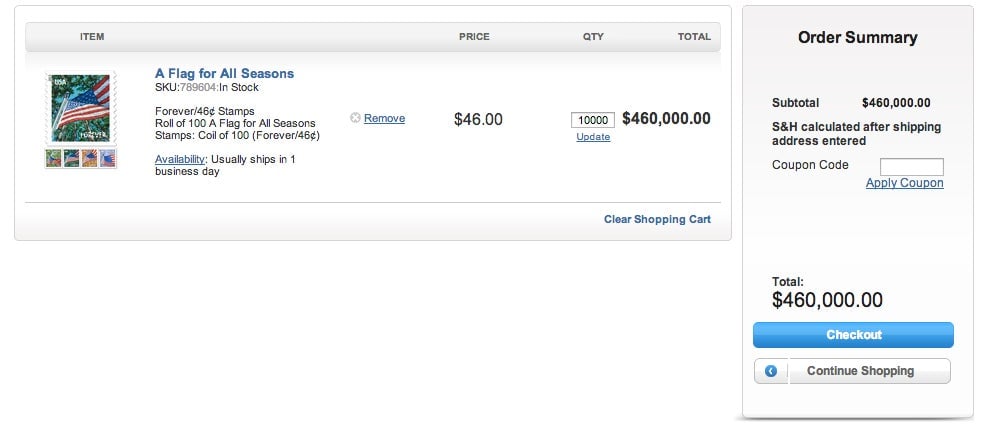

Our plan is to buy 10 million stamps at $0.46 each and sell them at $0.48. The margins, of course, are small. If we buy 10 million stamps, spending $4.6 million, we’ll earn $200,000—a 4.3% profit.

The good news is that you can buy up to 1 million stamps in a single order from the USPS, and pay a mere $1.75 in shipping (shipping is their business, after all).

But $4.6 million (or $4,600,001.75 with shipping) is a lot of money, especially for folks like us (an economist and a journalist) who’ve never raised money before and don’t have many assets. Ideally we’d borrow it all at once, but given our limited financial means, securing a $4.6 million loan would be tough, at least at an interest rate that would still leave room for us to make money.

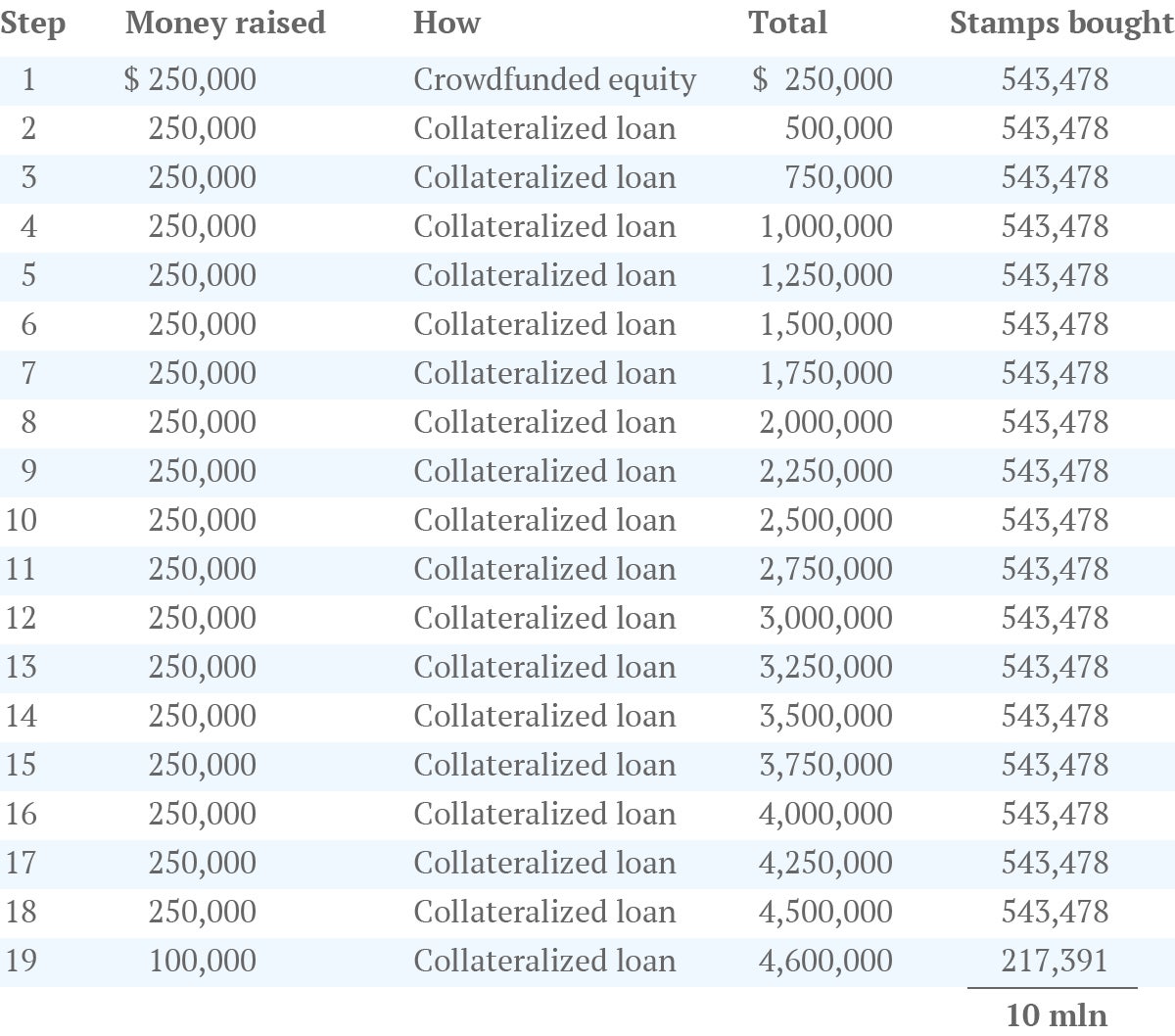

We’d get better terms on the loan if we had some collateral. But all we can offer is the stamps we plan to buy. So the trick is to get our seed funding by selling equity (we’d like to start with $250,000) and then securing loans for the rest using the stamps as collateral. It may seem a little far-fetched, but it’s not all that different from the kind of leveraged trading that goes on in the financial world.

In the past, our journey would probably end here. There’s no way we could convince our friends and family or millionaires to invest a total of $100,000 in this hare-brained scheme. But thanks to the recent US JOBS Act, we don’t need them. We can crowd-fund all of our equity from the general public on sites such as Crowdfunder. This would be our offer: We’ll split the profits 50/50, with half going to our shareholders and the other half to us.

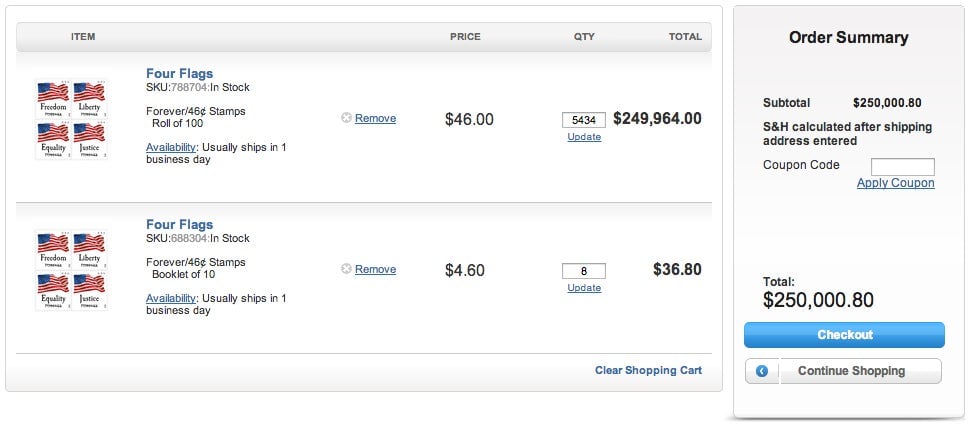

Once we’ve raised the $250,000, we can order some stamps: 5,434 rolls of 100 stamps for $249,964, plus 8 strips of 10 stamps for $36.80.

Including the $1.75 in shipping, that’s $250,002.55.

Those stamps won’t be enough collateral for a $4.6 million loan, so we’d need to take out a smaller loan and use that money to buy more stamps. Then we use those stamps to take out yet another loan and buy even more stamps. We estimate that we’ll need to take out 18 loans to get our hands on 10 million stamps.

That’s a total of 19 separate stamp orders, which will cost $33.25 in shipping. We can front that money ourselves. So, what about interest? Even though our loan is collateralized, it’s a risky proposition, so we expect to have to pay a fairly high interest rate—8% on an annual basis.

Getting the stamps is one thing; selling them is another. There’s no way we could convince a buyer to purchase our stamps before the price increase actually happens in January. Who would agree to buy more expensive stamps in the future when they could buy cheaper ones now? So, we’ll have to cut all of our deals after we’ve already put ourselves on the hook for $4.6 million. This is our biggest source of risk.

Ten million is a lot of stamps for us to move. It wouldn’t make sense for us to sell them directly to people, because people don’t typically keep a lot of stamps around. We could try to find an organization or company that does a lot of mass mailing, but such an organization would probably either print its own stamps or, if it’s a non-profit, buy them at a special discount rate from the USPS.

What we really need is a distributor—someone who can sell all of the stamps to convenience stores and drug stores, which usually sell stamps for $0.60 each or more. There is a company called C Store Distributors Directory that maintains a database of almost 1,000 convenience store distributors: names, email addresses, phone numbers. It sells copies of the database for $399. Our first step would be to buy one and get on the phone. The 3-cent spread gives us some room to negotiate. We can offer a cheaper price, say $0.475 a stamp, if they are willing to buy in bulk.

There’s always a chance distributors will be wary about working with a couple of unfamiliar people selling discount stamps. But there’s another avenue we could try: A company called Check Stand Program works with distributors across the country and helps anybody with a new product get that product into stores. If you pay it $3,500 and make 100 promotional displays, it will send its sales reps out to those stores to push whatever it is you’re trying to sell. The stamps we own would be out of our hands, but Check Stand increases the size our sales force to include people who actually have relationships with stores.

We might want to take both approaches. To avoid refinancing our loans and paying more interest, we would need to offload all the stamps in a month.

So, if we’re able to pull this off, how much will we make?

Assuming we sell all 10 million stamps for the bulk discount price of $0.475 each, our profit will be $150,000. Subtract out the $399 for the distributor database. Let’s also assume we spent the $3,500 for Check Stand Program plus, say, $300 to make the 100 displays for advertising in stores. That gives us $145,801.

If we do manage to shift the stamps in a month, the interest on our debt will be $29,000. That brings our profits to $116,801. Then we’ll return the equity to our shareholders, along with 50% of the profits.

That leaves us with the other 50%: $58,400.50. If you look at that as a profit on the $4.6 million initial outlay, it’s not very much: less than 1.3%. But remember, all that outlay was leveraged. So if you look at it as a return on our investment—$33.25 for shipping—it’s 175,541%.

So the ultimate forever-stamp arbitrage may indeed be worth it.