The Washington game of chicken on the US borrowing limit is starting to make China, the US’s biggest creditor, a little nervous. Zhu Guangyao, vice finance minister, today exhorted the US to “to ensure safety of Chinese investments” (link in Chinese), saying that the Chinese government “hopes the United States fully understands the lessons of history.” An Oct. 2 editorial in Communist Party mouthpiece Xinhua scolded that the US “has engaged in irresponsible spending for years.”

The Washington game of chicken on the US borrowing limit is starting to make China, the US’s biggest creditor, a little nervous. Zhu Guangyao, vice finance minister, today exhorted the US to “to ensure safety of Chinese investments” (link in Chinese), saying that the Chinese government “hopes the United States fully understands the lessons of history.” An Oct. 2 editorial in Communist Party mouthpiece Xinhua scolded that the US “has engaged in irresponsible spending for years.”

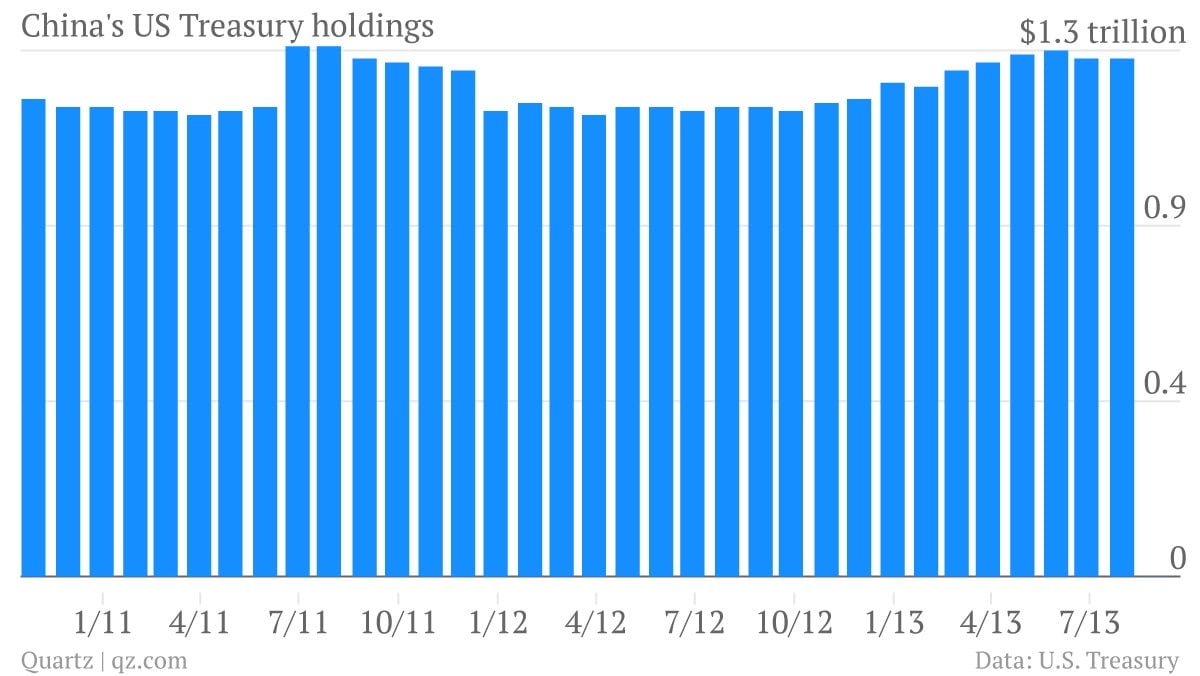

By “lessons of history” Zhu presumably meant the July 2011 budget showdown that prompted the rating agency Standard & Poors to downgrade US debt. After that point China’s holding of US Treasurys declined significantly (see chart below). It then rose again, but has recently fallen back. Zhu seemed to be hinting today that if the US continues to engage in debt brinkmanship it’s at risk of losing its biggest creditor. That would drive up the interest it has to pay and worsen its debt situation.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

However, the truth is that whether China buys US government debt has far more to do with its trade balance and capital flows than with the shenanigans in Washington. First, here’s a look at China’s Treasury holdings:

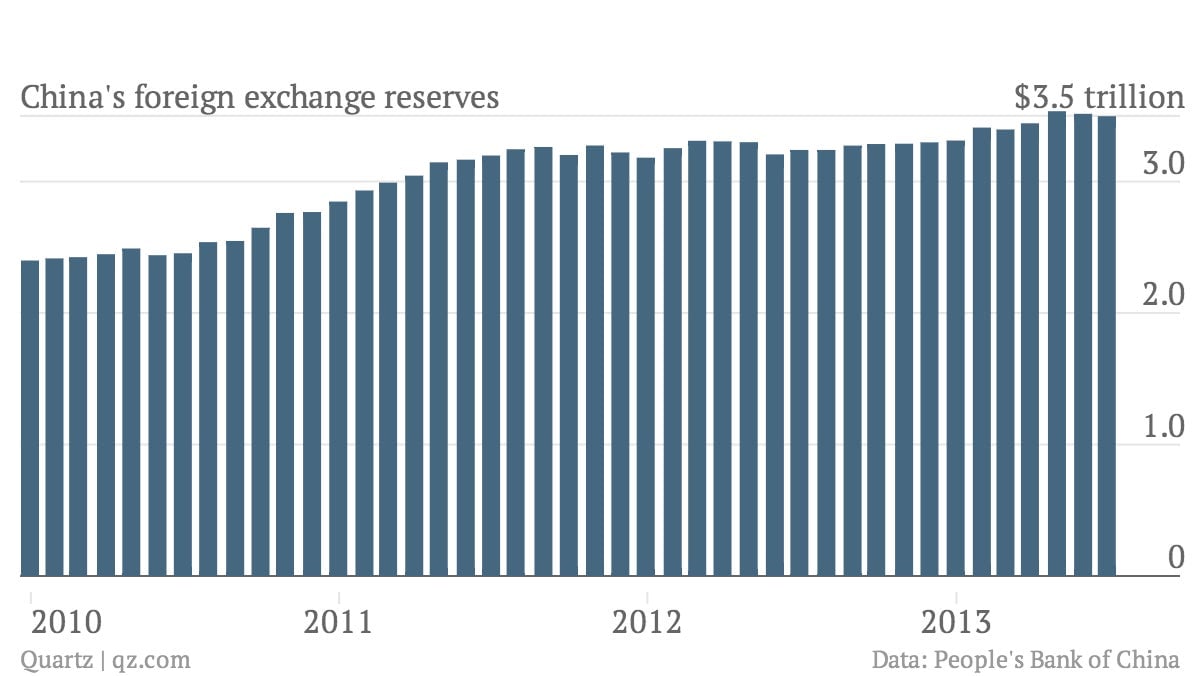

China’s central bank, the People’s Bank of China (PBOC), ties the yuan’s value closely to the US dollar. To do so it must buy dollars that come into the country from exporters and foreign investors when China exports more to the US than it imports, and when more investment is flowing into China than is flowing out. Those dollars go into the PBOC’s reserves. In order to make some return on them, it invests them in US government debt, the only market big and liquid enough for the size of its purchases.

But the central bank’s foreign-exchange reserves plateaued around mid 2011, shooting up again in the beginning of 2013:

So China stopped buying Treasurys in 2011 not because of the US debt wrangling but because it had more or less stopped accumulating extra reserves with which to buy them. And that didn’t change until January 2013, in the wake of a new wave of speculative money flowing into China.

This all tells you how little the US needs China to run its deficit, says China expert Gordon Chang. “The Chinese have not in fact been funding the Federal deficit since the middle of 2011,” writes Chang in a blog post on Forbes.com, noting that markets didn’t panic as a result.

Plus, China’s finger-wagging is absurd, given that its own currency manipulation has caused it to amass so many dollars. As we’ve argued before, the less China manipulates its currency to run a trade surplus, the greater the benefit to the US economy—and the less debt the US will need to issue in the first place.