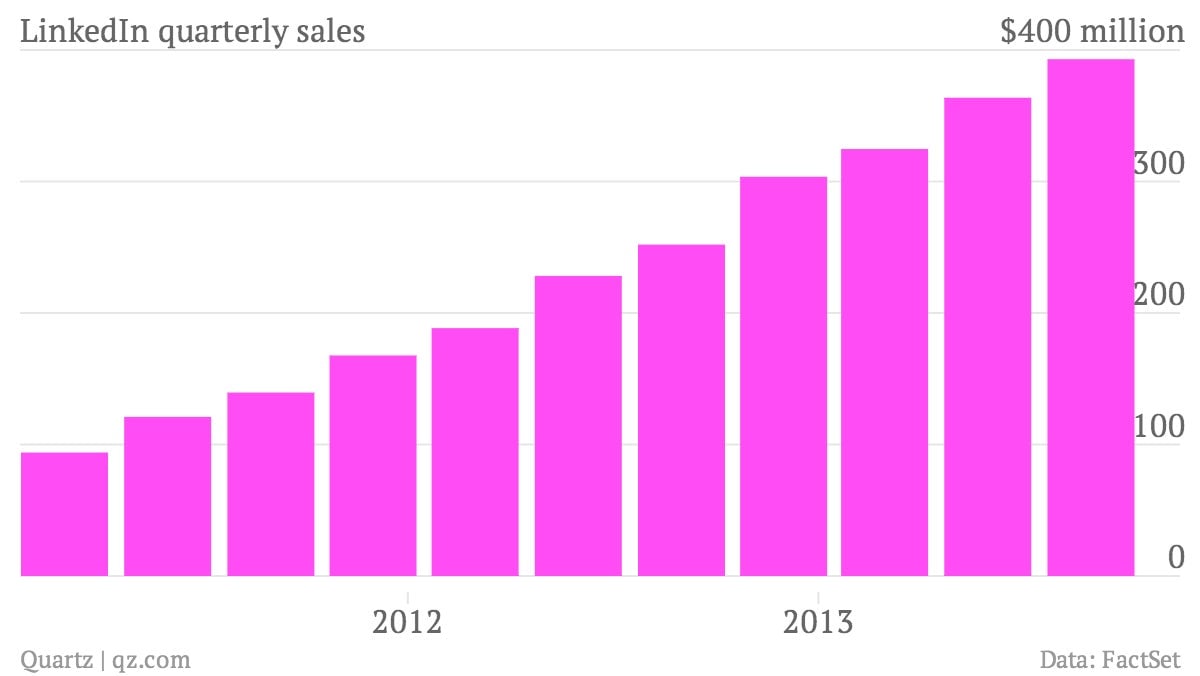

The numbers: LinkedIn swung to a third quarter net loss of $3.4 million, from a profit of $2.3 million last year, as the corporate social network ramped up investment in its platforms. But revenue for the third quarter surged 56% to $393 million. Together with an upbeat forecast for the next quarter, this was enough to drive shares up by 1.7% in after hours trading.

The takeaway: Those pesky emails from LinkedIn asking you to upgrade from free to paid service may drive you mad, but they appear to be working. Revenue from premium subscriptions jumped 61% to $79.8 million. The talent solutions division, which is mainly specialist products for recruiters, still accounts for the bulk of the business, with revenue growing by 62% to $224.7 million. Marketing solutions—mainly advertising—was up 38% to $88.5 million.

What’s interesting: During the quarter, LinkedIn membership climbed through the 259 million mark, an increase of 38% on last year. The gap with Twitter $TWTR, which has 218 million monthly active users, has widened. But the corporate social network is still way behind Google $GOOGL Plus, with 540 million active monthly users, and Facebook $META, with a whopping 1.2 billion.