It’s been a tremendous year for stock markets in large, developed economies.

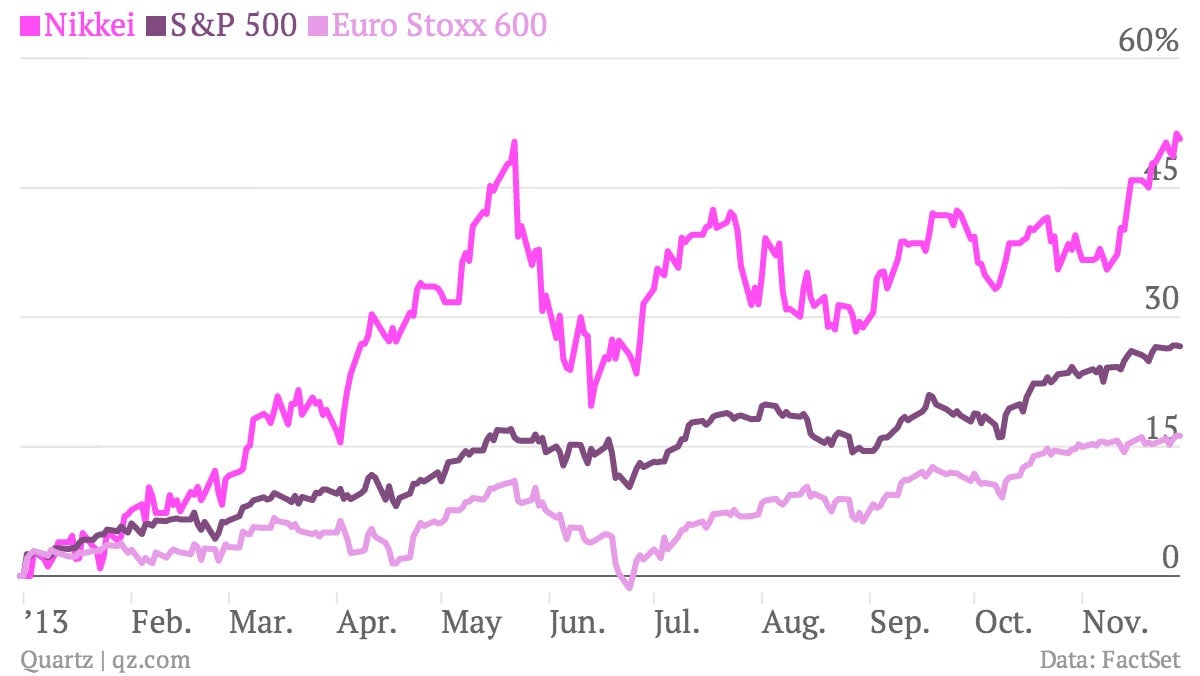

In the US, the S&P is up about 27%, the Nasdaq $NDAQ is up 34.5%. Japan did even better. The Nikkei is up 51% year-to-date. Even in economically plagued Europe, the equities markets had a terrific run, with the Euro Stoxx 600 up nearly 16%, through the start of December. After such broad-based increases, might it be time to take some of your winnings off the table?

No, say Wall Street analysts, who traditionally take some time late in the year to publish their outlooks for where they think the market’s headed. And after weighing up the options, it seems like most everybody still prefers stocks to other asset classes such as commodities, corporate bonds and government debt. Here’s a smattering of what they’re saying.

-Citi Global Asset Allocation

-Morgan Stanley $MS Research Global Strategy

-Credit Suisse Global Fixed Income & Economics Research

-JP Morgan Asset Allocation

Of course, the full analyses accompanying these projections are replete with conditionals, qualifications and all sorts of other hedges. And no wonder: Investors in the US have squeezed a lot out of S&P 500 already. At roughly 15 times earnings, the average forward price-to-earnings ratio for stocks in the S&P, a gauge of priciness, suggests that equities are verging on expensive, or at least no longer cheap. And retail investors are piling into the stock market, which is usually a good indication that this rally is getting a bit long in the tooth.

Still, the tooth can get longer. And if it does, sitting on the sidelines of an ongoing rally would be represent something of a career risk for Wall Street market analysts. If they’re wrong on stocks in 2014, at least most of them will be wrong together, which is far safer for them—even if not for investors.