Ben Bernanke just delivered what looks to be one of his final official speeches before the end of his term as Federal Reserve chair on Jan. 31. The speech is a nice, long history lesson of his thoughts on the extraordinary measures the Fed undertook during the financial crisis.

Ben Bernanke just delivered what looks to be one of his final official speeches before the end of his term as Federal Reserve chair on Jan. 31. The speech is a nice, long history lesson of his thoughts on the extraordinary measures the Fed undertook during the financial crisis.

As for what happens now, the question is when the Fed will raise its marquee policy rate—the Federal Funds target rate—which has been parked near zero for for just shy of five years. The answer? Probably not anytime soon, even though the Fed recently made moves to cut back on its bond-buying programs via the long-awaited taper.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Here’s Bernanke’s sharpest quote on the topic: “The FOMC’s decision to modestly reduce the pace of asset purchases at its December meeting did not indicate any diminution of its commitment to maintain a highly accommodative monetary policy for as long as needed.”

Translation: Even though the Fed is getting out of the bond-buying business, the Fed Funds rate is going to stay low for quite some time. And we think that will be enough to keep interest rates from spiraling wildly higher and hurting the economy.

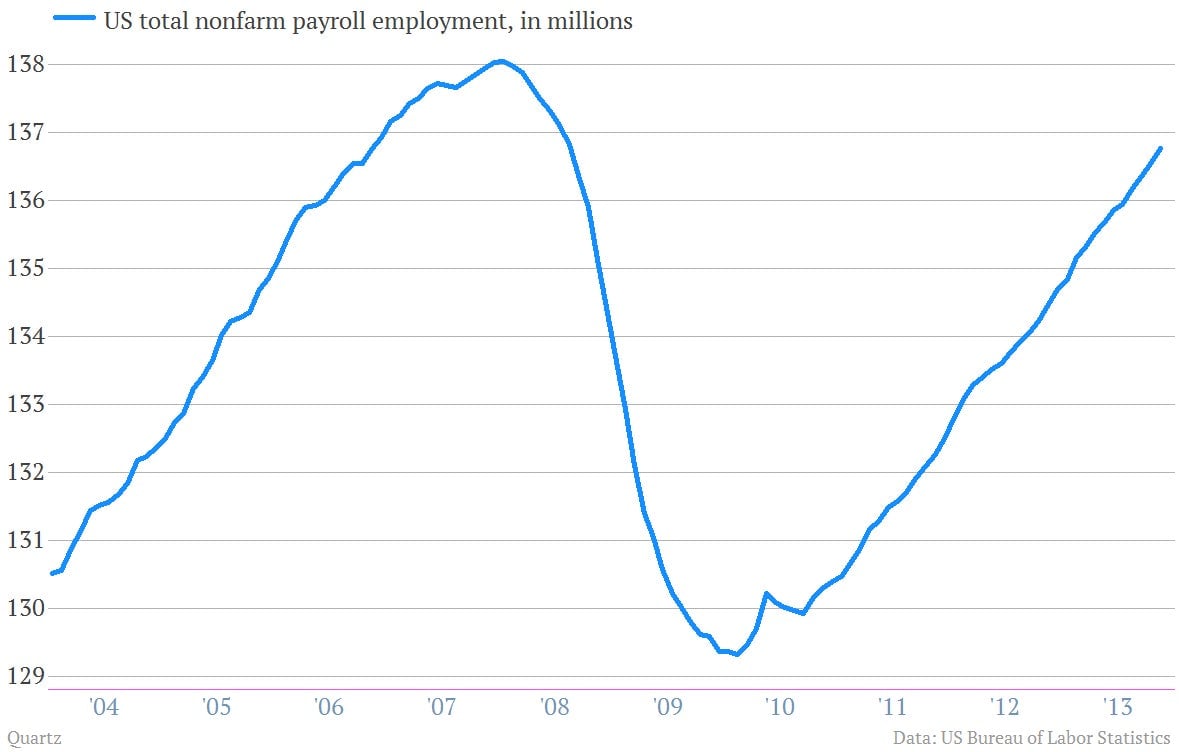

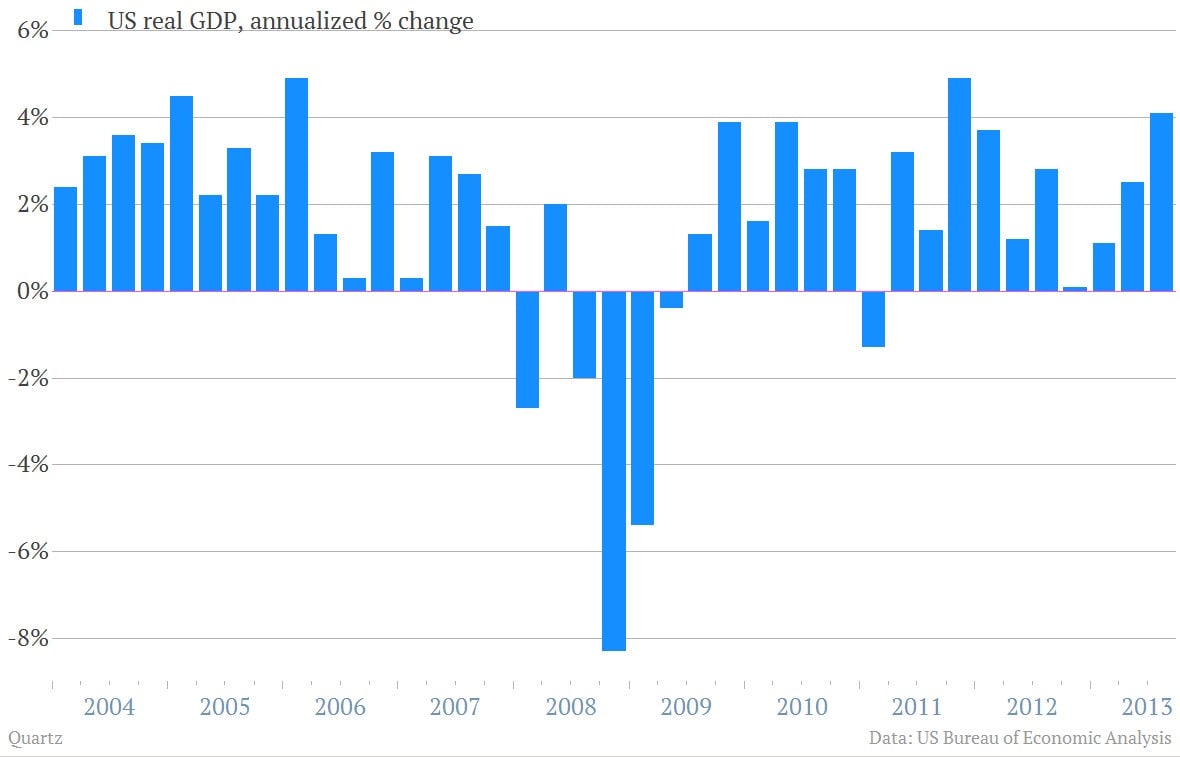

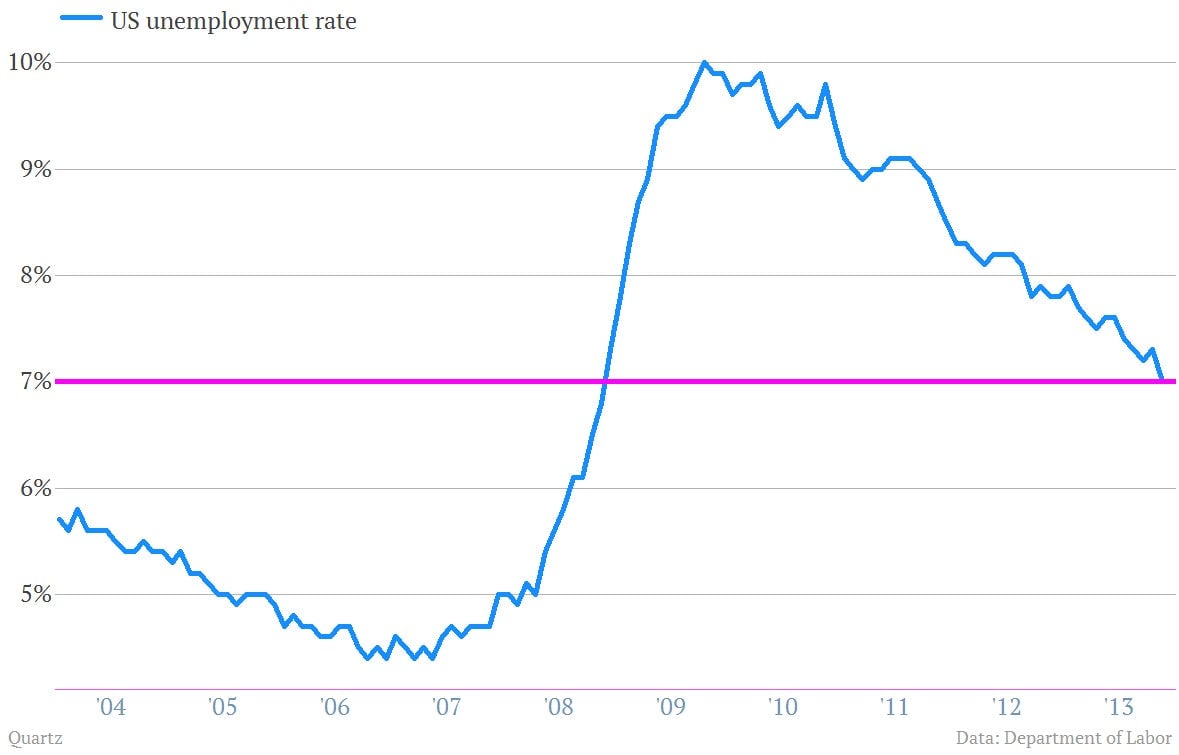

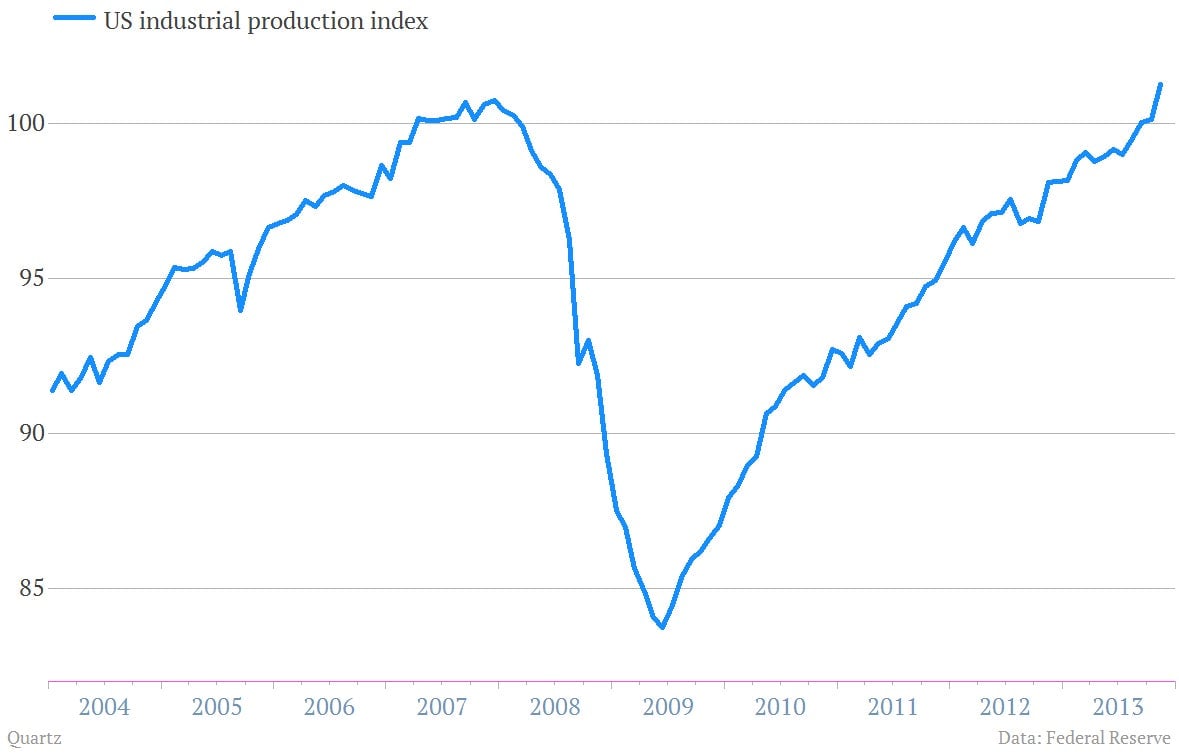

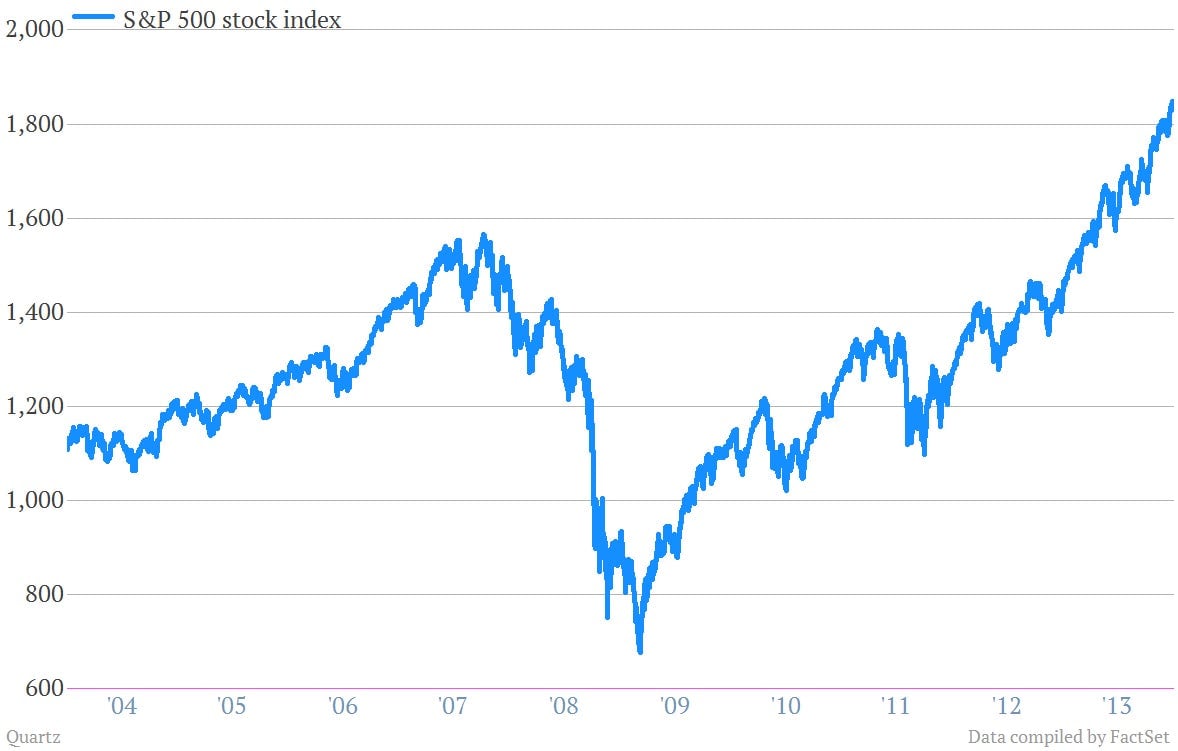

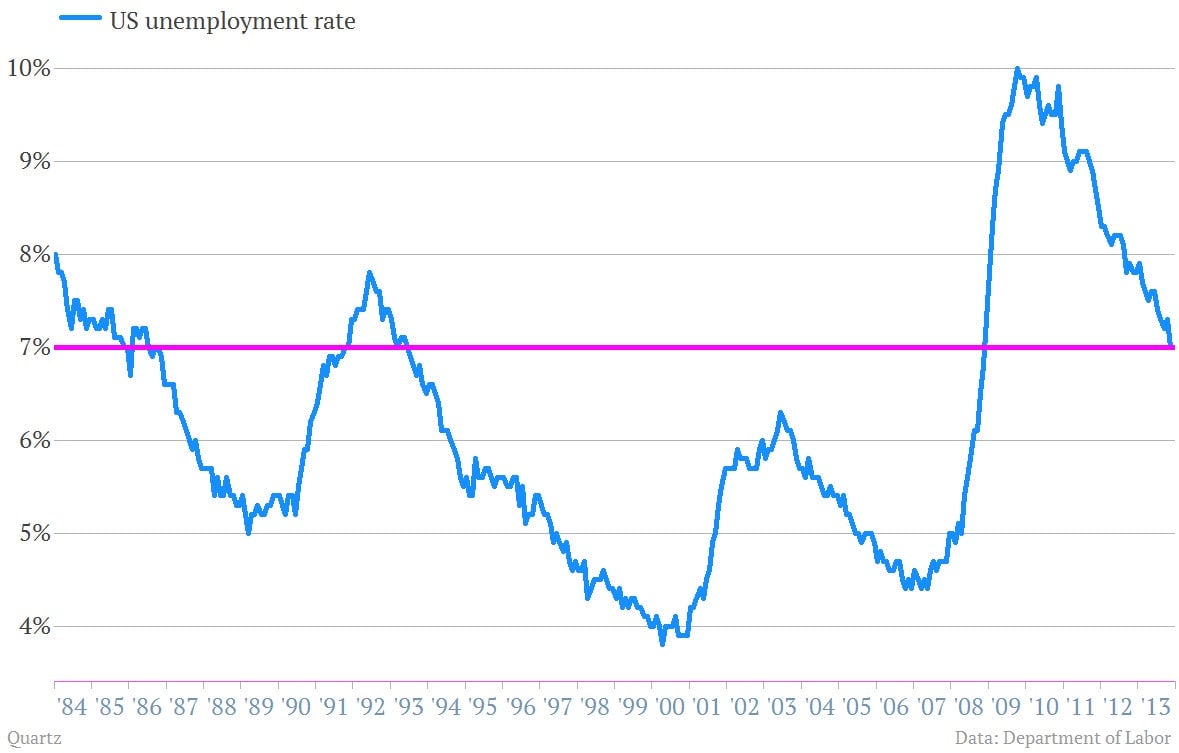

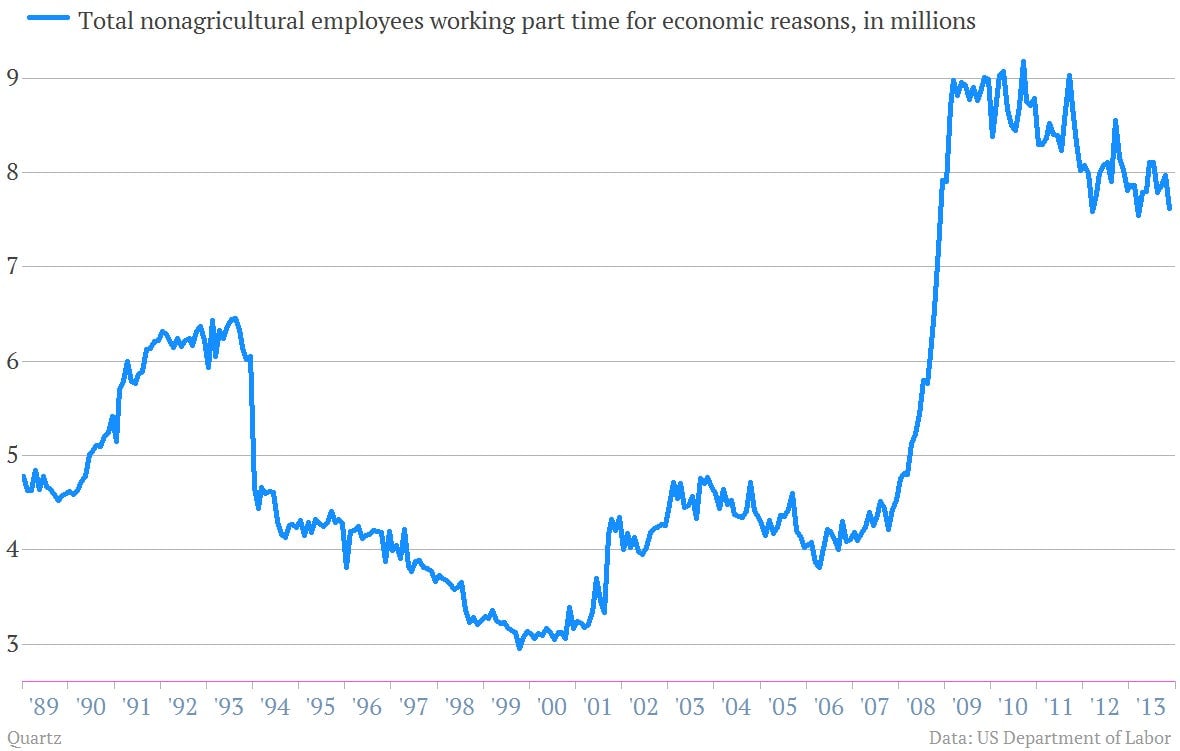

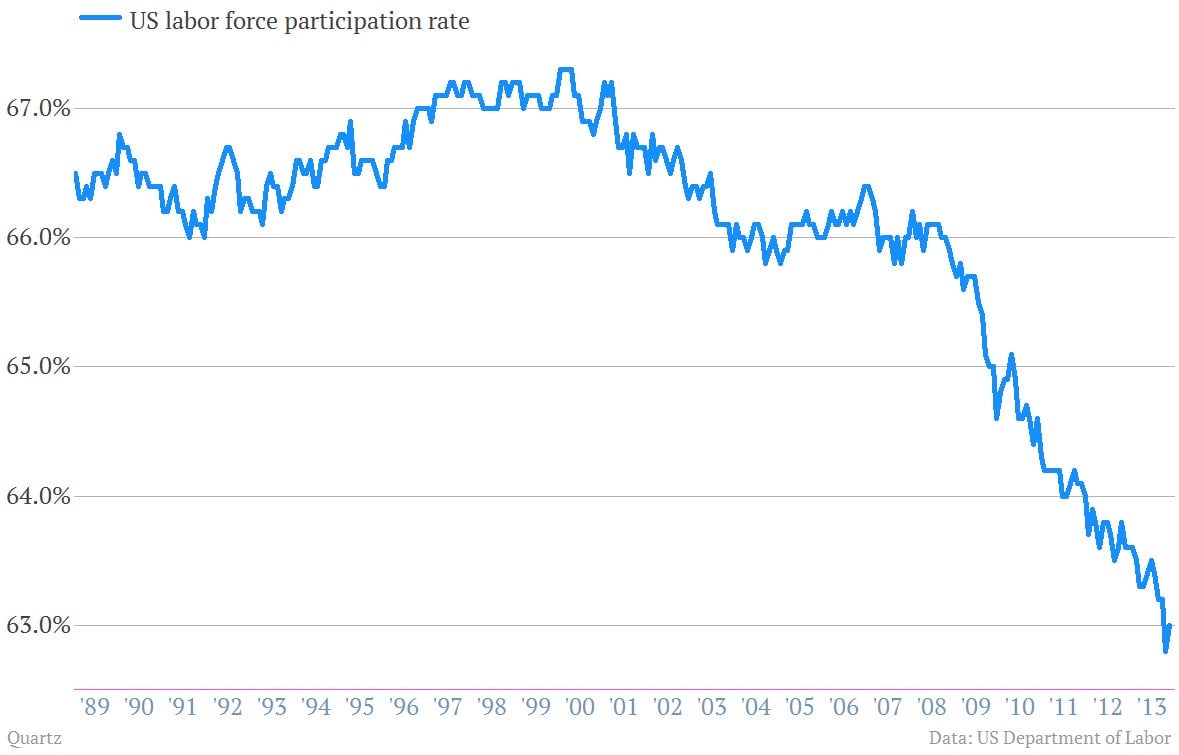

In short, Bernanke still thinks the economy is pretty weak. Here’s the key two-paragraph excerpt of his speech—in whole—that lays out his views on the economy, accompanied by relevant charts: