The once-fringe fantasy of a return to the gold standard is creeping back into the mainstream.

The once-fringe fantasy of a return to the gold standard is creeping back into the mainstream.

It has long been dismissed as a fool’s errand, on par with abandoning the Federal Reserve and other trappings of the modern economy. Mainstream economists deride it almost without exception. Reintroducing the gold standard would “be a disaster for any large advanced economy,” says the University of Chicago’s Anil Kashyap, who connects enthusiasm for it with “macroeconomic illiteracy.” His colleague, Nobel laureate Richard Thaler, struggles with its very underlying principle: “Why tie to gold? Why not 1982 Bordeaux?”

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Yet the idea that every US dollar should be backed by a small amount of actual gold is more popular than economists’ opinions might suggest. Advocates include members of Congress and president Donald Trump. Enthusiasm for a return to the gold standard has become more prominent since Trump’s most recent nominees to fill the vacant Federal Reserve governorship have endorsed a return. The first two—Herman Cain and Stephen Moore—both dropped out of consideration, but the third, economist Judy Shelton, announced today in a Trump tweet, may be the most ardent in her support.

Last year, Shelton called for a “new Bretton Woods conference,” akin to the 1944 meeting that established the post-war economic order, perhaps to be held at Mar-a-Lago, where a return to the gold standard could be considered. “We make America great again by making America’s money great again,” she wrote in the journal of the Cato Institute, a libertarian think tank.

Since 2011, at least six states have passed laws recognizing gold and silver as currency; another three are presently contemplating bills of their own. The surprising success of Ron Paul, a Texas Republican Congressman and ardent gold bug, in the 2008 and 2012 elections showed the potency of these ideas among the electorate. In its 2012 and 2016 campaign platforms, the Republican Party called for a commission to investigate the viability of a return to a gold standard system. The Republican-controlled House of Representatives passed a bill including such a commission in both 2015 and 2017, but both times the proposals died in the Senate. Last year, Alexander Mooney, a Republican representative from West Virginia, took that a step further when he introduced a bill proposing a full-on return to the gold standard. (The bill has no cosponsors and, unsurprisingly, has gone nowhere.)

Today, with inflation unusually low and stable, the gold standard is a tougher sell than it once was. But as trust in American institutions wanes, there is renewed support for money backed by something tangible, not the say-so of the government. If inflation picks up once again, a solid base of gold standard evangelists is ready to take it mainstream. That a supporter of the gold standard may yet wind up on the Fed’s board of governors is yet more evidence that the idea’s prospects are shining brighter than they have in many years .

Money depends on trust—the faith that it will hold its value so that, when the time comes to spend it, it will be accepted without question in exchange for what the holder expects it to be worth. Inflation eats away at that value.

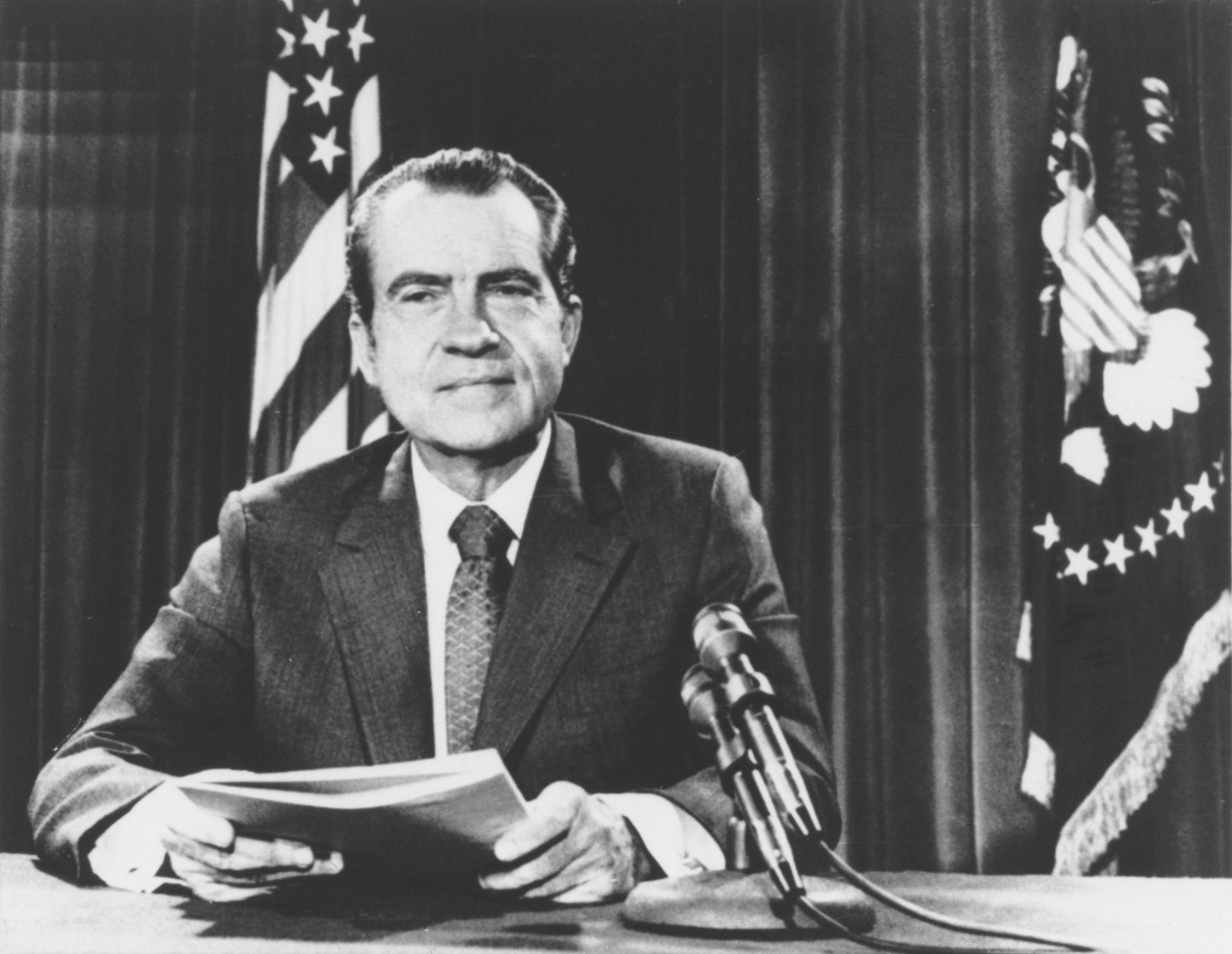

In modern times, governments are often a culprit behind inflation. Since they enjoy a monopoly on printing money, they can issue new currency at virtually no cost. But governments are run by vote-seeking politicians, who might print more money to juice short-term growth needed to win re-election, inadvertently causing inflation to flare up later. This quandary isn’t theoretical, and has happened with surprising frequency throughout history. To cite a recent, prominent example, US president Richard Nixon bent to this temptation (pdf) during his 1972 re-election campaign—contributing to the breakout of inflation that ravaged the American economy throughout the 1970s and early 1980s.

There’s a seemingly easy fix: Take the power of money creation out of the hands of politicians. According to the monetarist theory popularized by economist Milton Friedman in the 1970s, preventing inflation requires fixing the supply of money. The gold standard, by limiting the dollars the government can print to the weight of gold it holds in reserves, is one way of doing so.

The US adopted the gold standard in 1879, when Congress finally followed Britain, Germany, France, and other advanced nations. By holding national currencies stable against gold, the international embrace of the gold standard encouraged foreign investment and facilitated trade, giving rise to the first era of intense globalization.

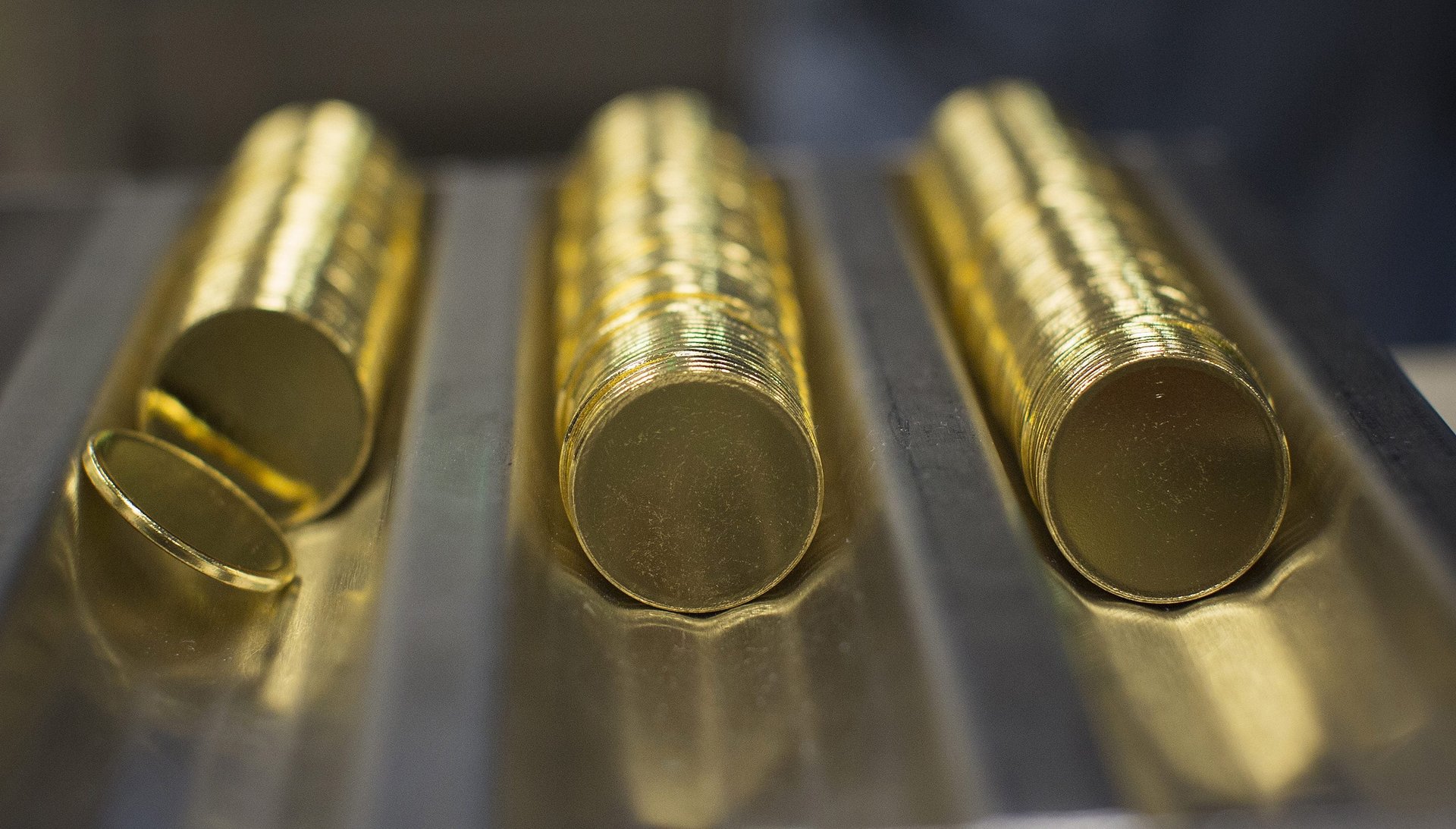

Here’s a very cartoonish version of how it worked: The US Treasury agreed to redeem a set weight of gold in exchange for a fixed number of dollars, and vice versa. During the classical gold standard era—from 1879 to 1914 in the US—one troy ounce of gold fetched $21.

The gold standard’s discipline came from the fact that the government had to be sure it held the necessary volume of gold in reserve, in case anyone wanted to exchange dollars for a set amount of the shiny metal. If it printed more money than it held in gold reserves, the state risked hyperinflation or causing a financial crisis by shattering faith in the solidity of its currency.

In theory, the gold standard, therefore, limits government spending to only what it can raise in taxes or borrow against its gold reserve, and prevents it from simply printing money to pay its debts. It also takes power over the money supply away from central bankers. Indeed, it might render central banks mostly unnecessary. Bear in mind that for most of the classical gold standard era, the US didn’t have a central bank, which was introduced in 1913.

Had history worked out differently, the dollar might have been pegged to cowrie shells, peppercorns, or giant stone disks, all of which, like gold, have served as money at one time or another. But for reasons both aesthetic and practical, the glimmering metal became the asset of choice. “The simple answer to that is that for the last 5,000 years, so far as we are aware, man has used gold and silver as money, and particularly gold,” says Alasdair Macleod, the head of research at Goldmoney, a Toronto-based investment manager for precious metals. “It’s durable, people respect that it’s got value—it’s actually as simple as that. It is something which markets should be free to choose, and they have chosen gold.”

Gold is integral to the story of US growth and prosperity. In the 19th century, discoveries of subterranean veins in at least 24 states were “rungs in a ladder that culminated in America’s economic domination of the globe,” prompting westward migration and economic expansion, writes James Ledbetter in One Nation Under Gold: How One Precious Metal Has Dominated the American Imagination for Four Centuries. It is a national emblem of wealth, and “streets paved with gold” served as a myth that helped lure many migrants to the US. “From the very beginnings of our national life, it has seemed impossible for Americans to look at gold dispassionately,” Ledbetter explains. “The metal, and its seductive hint of boundless wealth, tap into a psychological wellspring that reaches beyond any purely physical qualities.”

Legislation in the past century which codified and restricted how Americans could attain or trade gold seems to have intensified the longing for it. In 1933, Americans were temporarily barred from buying and selling gold within the country; by the 1950s, the law was still in place, and a black market for gold flourished. John F. Kennedy was anxious that the dollar should be “as good as gold”; Operation Goldfinger, which launched a few years later, was a top-secret government campaign to dig up gold within US territories as quickly as possible, with the hope of propping up a post-war economy expanding at a pace that threatened to outstrip the world’s supply of the metal.

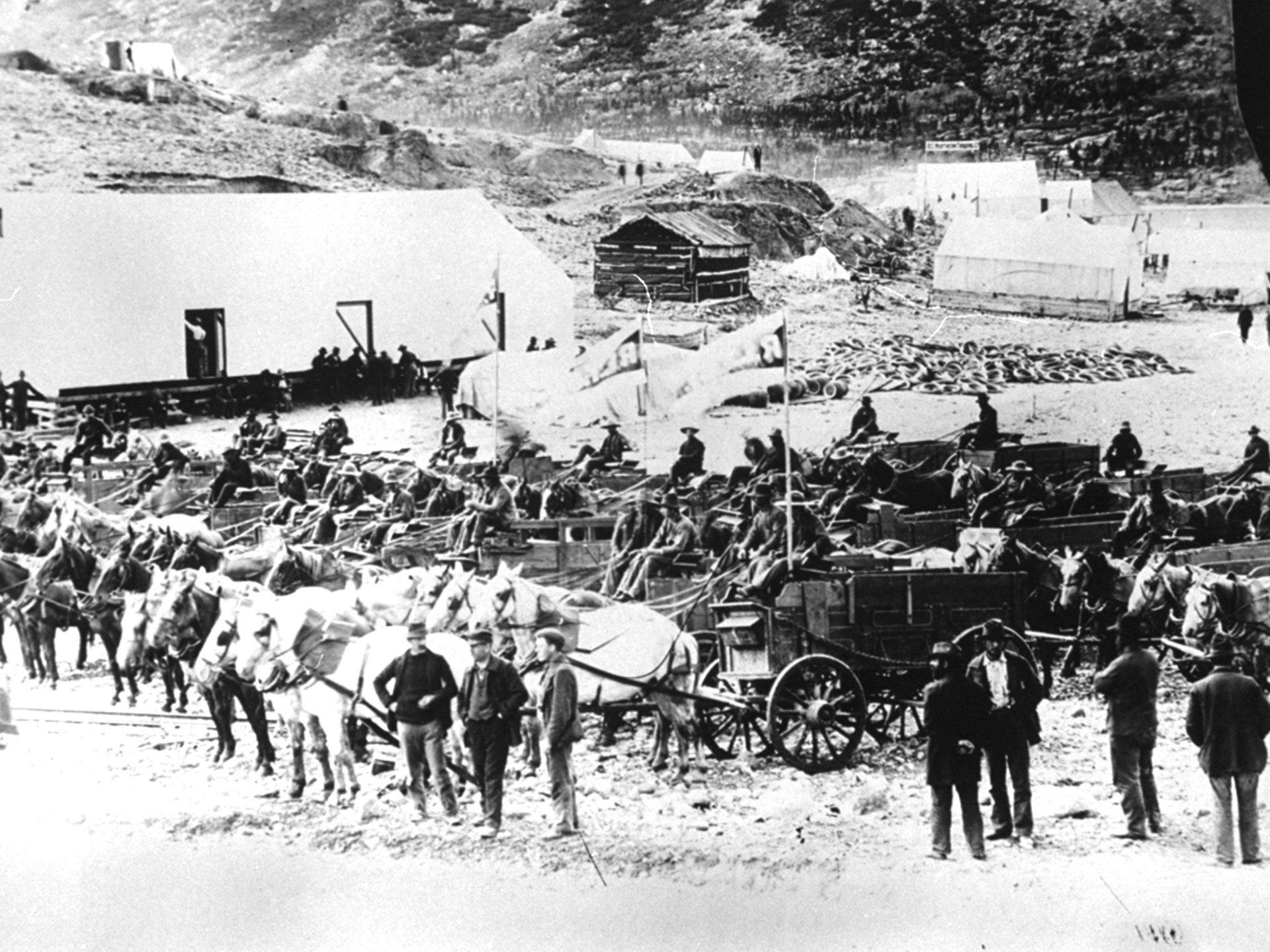

The gold standard is inextricably tied to mining. The supply of the metal depends on how much is extracted from the earth, after all. But since mining only adds a tiny fraction to the overall stock of gold each year, prices don’t fluctuate as wildly as they used to. In the height of mining activity, in the mid-1800s, big gold discoveries in California and Australia spurred a pickup in inflation. Then, as economic growth outpaced the rate of new gold discoveries, a 20-year period of deflation set in; it ended with new discoveries in South Africa and the Yukon, as well as technological advances in gold processing. That’s how things are supposed to work: When a gold shortage causes purchasing power to rise steadily, mining companies are encouraged to find more gold.

And indeed, overall, prices and real economic activity during the classical gold standard era was remarkably stable (pdf). “If you look at the US during its classical gold standard period, the average rate of inflation is pretty close to zero—and likewise in Great Britain over its experience with the gold standard,” says Lawrence White, an economics professor at George Mason University and one of the few respected economists who’s pro-gold standard.

Gold-standard adherents often extol the strength of currencies such as the pound and the dollar in the early 20th century. Modern central banking, they say, has knocked the stuffing out of these once mighty currencies. (The fact that average hourly wages have mostly been adjusted to match the rise in inflation doesn’t seem to factor into the equation.) Where mainstream economists see constraint, goldbugs see discipline—a government that cannot spend beyond its means—and a hedge against corruption. For those who believe in small, limited government, there is obvious appeal. Believers credit it with a kind of Midas touch: the gold standard necessarily begets “balanced budgets, low taxes, small government and a healthy economy,” to borrow the words of economist Barry Eichengreen, a prominent historian of currencies at the University of California, Berkeley.

The thing is, economic success during the classical gold standard era depends somewhat on the eye of the beholder. David Laidler, a monetary historian at Western University in Ontario and Friedman’s research assistant in the 1960s, says the gold standard wasn’t as effortlessly successful as the data might suggest.

“I’m not going to tell you that the gold standard didn’t function in the 19th century—it did. But it didn’t quite deliver the kind of nirvana that people now talk about,” he says.

For some Americans, its effects were downright devastating. After the US adopted the gold standard in the 1870s, price levels of agricultural commodities fell continuously for nearly 20 years, crushing American farmers under the weight of their debts and punishing interest rates. The resulting political upheaval culminated in William Jennings Bryan’s famous “cross of gold” speech: his tirade against how deflation caused by the gold standard was ravaging rural America.

Questions of money are always political, and often a zero-sum choice between which economic class will prosper and which will suffer. Inflation erodes the value of financial assets, hurting savers but helping borrowers. Deflation benefits those with wealth and punishes debtors. Eventually, the latter group—the masses whose standard of living relies on mortgages and other forms of debt—tends to win out.

The classical gold standard era ended with World War I, because to fund wars governments have to print a lot of money. In these conditions, maintaining gold convertibility goes out the window. After the war ended, the US and most other advanced economies scrambled to re-peg their currencies to gold. But for a host of reasons—for example, the overvaluation of the pound and several other key currencies, and the decline of Britain as an imperial power—the gold standard failed to deliver the stability of the earlier era.

Many economists argue it amplified the shocks of the Great Depression, particularly in the US and France, which waited longer than their trading partners to abandon convertibility. It was for this reason that John Maynard Keynes, the great British economist, called the gold standard a “barbarous relic.” Unsurprisingly, the post-World War II monetary system—of which Keynes was a key architect—made the US dollar the basis of world reserves. The dollar itself was still convertible into gold. However, other global currencies fixed their exchange rates not to gold, but to the dollar.

When Richard Nixon took office in the late 1960s, the US government was again spending heavily, due to the Vietnam War and the social welfare programs launched by his predecessor, Lyndon Johnson. That effectively pushed down the value of the dollar. In 1971, to stave off a run on US gold reserves, Nixon halted convertibility (meaning that other countries could no longer redeem dollars for gold). Under intensifying pressure, in 1973 the president scrapped the gold standard altogether.

Prices started climbing, exacerbated by Nixon’s strong-arming of the Fed to keep rates low. As the 1970s wore on and inflation surged, gold found support among the likes of Ronald Reagan, who talked it up on the campaign trail during the 1980 presidential election. By June 1980, prices for consumer goods were rising 14% annually, galvanizing public support for “sound money.” After trouncing Jimmy Carter, Reagan set up a commission to determine whether to revive the gold standard.

Nixon had promised, and perhaps believed, that the US would eventually return to the gold standard. Reagan’s victory made that look possible—likely, even. But many of the president’s appointees to the commission were longtime opponents of the system (among the exceptions was a certain young Texas congressman named Ron Paul). Then came the “Volcker shock,” when Fed chairman Paul Volcker hiked rates to their highest levels in history to curb runaway inflation, which thrust the economy into a deep recession. Crucially, though, inflation dropped sharply and the commission put the official kibosh (pdf) on a return to a fixed metallic standard.

With inflation finally tamed, gold’s moment was over. Fiat currency managed by central bankers had officially won out.

This abandonment represents a betrayal to a few distinct, but often overlapping, groups: people who believe in limited government; people who interpret the American constitution literally; and people who fear the power of central banks, Wall Street, and other financial institutions.

Advocates of the gold standard point to the fact that because there is no way to redeem paper dollars for gold or silver, “there is no way to finally pay a debt.” One common fear is that investors will stop buying US Treasury bonds, ultimately resulting in financial ruin for the country.

Their concerns can run to the hyperbolic. “It is impossible to overstate the calamity that will occur when the Treasury bond collapses,” stresses the homepage of the Arizona-based Gold Standard Institute, a peripheral non-profit “dedicated to spreading awareness and knowledge of gold.” On our current course, “we will wake up one morning and find that our bank accounts are wiped out,” it warns. “Even if we have dollar bills in our pockets, food will not last in stores for very long, because food production and distribution depends on the banking system.”

Some argue returning to the gold standard is a legal imperative.

There is a basis in the US Constitution for this, at once specific and quite vague: Sections 8 and 10 of Article I state that Congress has the “Power…to coin Money, regulate the Value thereof, and of foreign Coin,” while “no state…shall make any Thing but gold and silver Coin a Tender in Payment of Debts.”

It’s entirely possible that this was supposed to guarantee convertibility between state currencies, rather than asserting anything intrinsic to gold. But these two mentions in the country’s founding document have served as ammunition for constitutionalists, including groups such as the far-right John Birch Society, established in 1958. The society, whose views align closely with Trump’s, supports the disestablishment of the Fed and a return to the gold standard, on the grounds that the constitution does not give Congress the right to delegate its money-related powers elsewhere, nor to use any currency that is not gold- or silver-backed.

But if there are various arguments for a return to the gold standard, there are many more reasons to reject it. Nearly 50 years into using fiat currency at a floating exchange rate, a total overhaul of America’s entrenched monetary policy framework is much less feasible.

For one thing, says Laidler of Western University, the rise over the past four decades of politically independent central banks has made it unnecessary. That’s because, as long-time Fed chair Alan Greenspan told Congress, “a central bank properly functioning will endeavor to, in many cases, replicate what a gold standard would itself generate.”

Plus, constraining a central bank limits how easily it can adjust monetary policy to respond to economic conditions. Between 1879 and 1914, when the US adhered to the gold standard but had no central bank, private clearinghouse associations played the “lender of last resort” role for member banks, says White, the George Mason economist. The world’s financial system is now vastly bigger, more complex, more deeply integrated, and more global than it was during the gold standard’s heyday. It’s hard to imagine how anything less than a strong, central authority could stave off, for example, the scale of market collapse that threatened the world in 2008.

The US would derive minimal benefit from re-adopting the gold standard unless other major economies did too. However, even then, the system of fixed-exchange rates created by gold convertibility has some big downsides. While encouraging cross-border investment and trade, it also makes it extremely hard for governments to adjust to localized economic disruptions (the struggles of the euro zone currency union offers a present-day example of this drawback). The gold standard could also push financial contagion to viral levels, with the flow of gold and the fixed exchange rate forcing the suffering of one nation on everyone in the system.

Despite the myriad reasons that a return to the gold standard seems impossible, the dream remains alive, in part because of the efforts of Ron Paul. Paul was first moved to run for office in 1976, in reaction to Nixon scrapping gold standard a few years prior. “I remember the day very clearly,” he told Texas Monthly in 2001. “Nixon closed the gold window, which meant admitting that we could no longer meet our commitments and that there would be no more backing of the dollar. After that day, all money would be political money rather than money of real value. I was astounded.”

Paul’s views were shaped in part by economist Friedrich Hayek’s accounts of how the Nazis’ effective abandonment of the gold standard allowed them to beef up fiscal spending in preparation for their war of conquest, Eichengreen wrote in National Interest in 2011. Paul subsequently spent most of his career as a vocal but lonely goldbug in Congress. He retired in 2013.

These days, Mooney, the West Virginia Congressman, has taken up the mantle as one of gold’s biggest cheerleaders (Ron Paul’s son Rand, a senator from Kentucky, is also a part of this club). For Mooney, American Eagle coins are the key to reviving the gold standard. These collectibles are issued by the US mint and sold to numismatists for about $1,600 apiece, despite having a face value of just $50—roughly the cost of an ounce of gold in the early 1970s. Some goldbugs see them as a symbol of what American money should be; the disparity between the face value of these coins and the value of the gold used to make them captures how far the dollar has fallen in their minds.

Though they are not US legal tender, state law in Utah allows them to be used as currency—though it’s an expensive way to get $50 of gas or groceries. Other state laws have mostly moved to lift taxes on them, broadly recognizing them as money rather than collectibles, on the order of baseball cards and Beanie Babies. (This taxation of money is a big beef for Mooney and his allies.)

If American Eagle coins are a symbol of how degraded US currency has become, for gold adherents, a return to the gold standard seems like the best way to protect the dollar’s value and and ensure it remains a bulwark against inflation.

It’s probably no coincidence that the most recent resurgence of gold interest has come at a time of acute public anxiety about the stability of money. The global financial system nearly blew up 10 years ago, and was saved by unprecedented monetary activism by the Federal Reserve. Nobody knew what to expect from the Fed’s epic asset purchase program. Fears of Weimar-style hyperinflation in some corners proved fertile ground for the pro-gold messages of Paul and others who see salvation in gold. Paul’s surprisingly successful grassroots presidential campaigns were further evidence that his message was gaining traction.

Hyperinflation never happened. But nor did other monetary fears recede—notably government over-reliance on debt. While on occasion president Trump has said that deficits don’t matter, the commander-in-chief credits the “very, very solid country” of yesteryear with it being based on the gold standard. In 2016, before his election, Trump suggested it might be time to stage a return: “Bringing back the gold standard would be very hard to do—but boy, would it be wonderful. We’d have a standard on which to base our money.” This might be dismissed as a throwaway comment, if not for Trump’s desire to put the likes of Cain, Moore, and now Shelton on the Fed board, giving a goldbug a seat at the table to steer the most powerful country’s monetary policy.