In both the run-up to and the aftermath of the Federal Reserve’s announcement of a third round of money creation and bond-buying—quantitative easing—known as QE3, the fashionable position on Wall Street and among the financial commentariat was that it wouldn’t work. Sure, the thinking went, the Fed might be able to set off a rally in financial markets such as stocks and commodities, but it won’t be able to do anything for the real economy.

Such thoughts were often delivered with a world-weary sigh and frequently while wearing a bow-tie.

And like plenty of positions that become popular in and around Wall Street, these views turned out to be two things: Dead. And wrong.

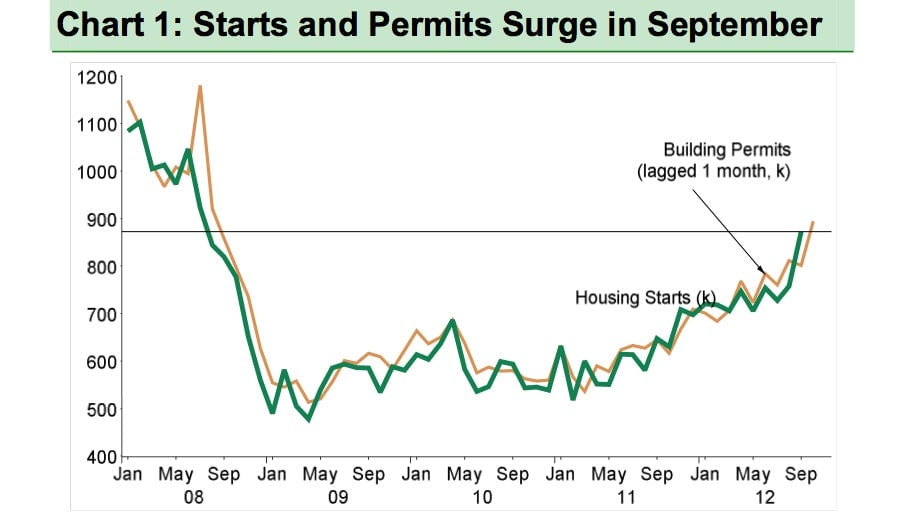

There’s really no other way to explain the massive—and apparently strengthening—turnaround that we’ve seen in housing lately (see chart above) except for the Fed. This morning’s jump in US housing starts is just the latest tidbit of data to support what’s becoming a widely held view.

Of course, all the requisite caveats apply. The US economy still looks weak. The labor market, while showing signs of improvement, is fragile. And whether the benefits of any boost to housing spreads to the broader economy remains very much an open question. And by the way, it’s also true that housing was showing signs of “green shoots” even before the Fed announced QE3.

But policymakers at the central bank recognized that trend early and pushed hard to keep it going. And that largely explains how and why they unveiled their plan for unlimited purchases of federally guaranteed mortgage bonds. (Here’s a chart-laden explainer on why this might be Ben Bernanke’s masterstroke.)

So, for the historical record, here are a few purveyors of the conventional wisdom who now look anywhere from slightly misguided to quite wrong. Of course, being wrong isn’t a crime. It is, however, a fact.