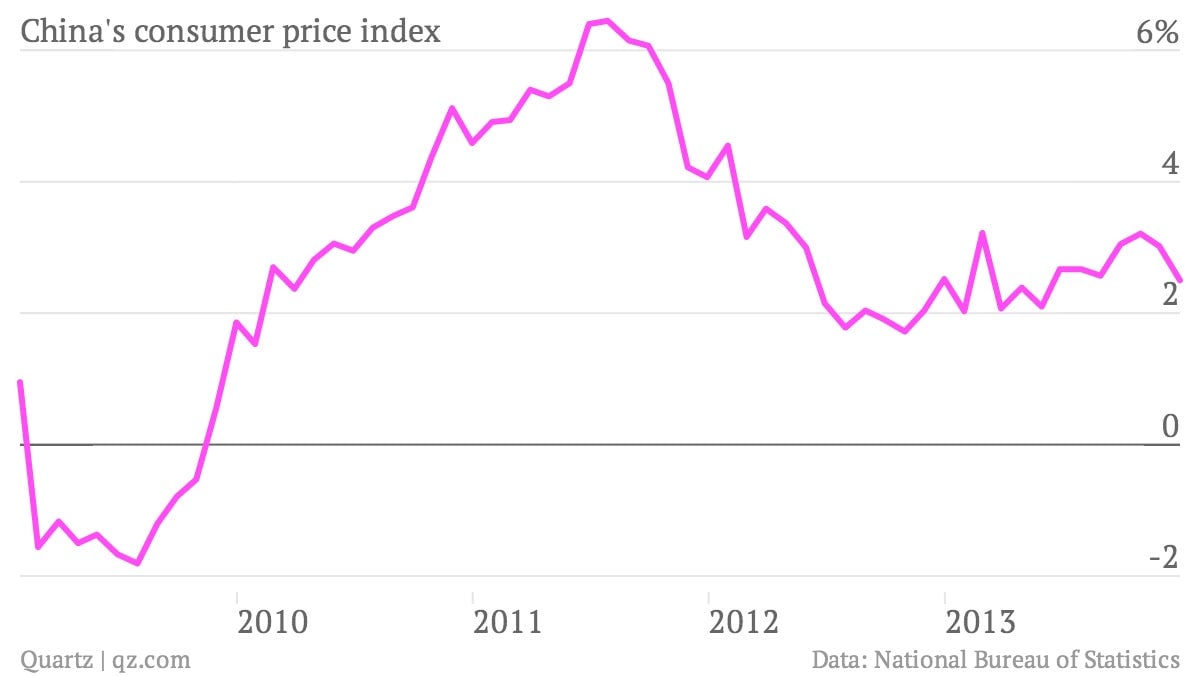

Despite massive gushes of credit pumped into the system each month, Chinese consumer price inflation (CPI) hit a seven-month low in Dec. 2013.

Despite massive gushes of credit pumped into the system each month, Chinese consumer price inflation (CPI) hit a seven-month low in Dec. 2013.

In a typical economy, this would make no sense. Ebbing inflation, alongside slowing GDP growth, are not what you see when monetary policy is loose. But China isn’t a typical economy.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Where economists disagree is on what a slowing inflation rate does say about China’s money supply. Slate’s Matthew Yglesias argued that something “people are missing about the China slowdown is that monetary policy keeps getting tighter.” Patrick Chovanec, an economist at Silvercrest Asset Management, takes the opposite position. ”Every time the CPI rate looks moderate, people say [China has] more room for monetary easing to boost the economy,” he tells Quartz. “[But] monetary policy is already horrendously loose in China.” Michael Pettis, a finance professor at Peking University, concurs: CPI “is not the appropriate measure by which to gauge domestic monetary conditions.”

Why does this matter? Because just how tight or loose monetary policy is—and, as it turns out, for whom—makes all the difference to China’s chances of “rebalancing” its economy without crashing it.

What makes China unlike Western economies is that the government, not the market, determines the interest rates—in other words, the cost of money—on both deposits and loans. By setting them both artificially low, the government shifts wealth from savers to borrowers.

The more money pumping into the system, the more borrowers benefit. And pump it does: controlling the value of China’s currency versus the dollar forces China’s central bank to spew enormous sums of money into its financial system.

As for China’s hapless savers, the closed capital account leaves them unable to invest in much else, so despite lousy rates, they keep stashing their cash in banks.

This unfair distribution is why the money supply can surge without juicing consumer inflation. To achieve a similar effect, a market-based system would have to do something like this, argues Pettis:

Imagine if somehow the US were to enact a law whose result was that every time the Fed expanded the money supply, a one-off tax was imposed on households, the proceeds of which were transferred to corporate borrowers. In that case monetary expansion would be much less likely to cause an increase in demand for consumer products, and so would create much less consumer price inflation, and much more likely to cause a surge in production.

So what about monetary policy—has it, as Yglesias argues, been getting tighter?

The answer is that it has for some but not at all for others. Thanks to China’s two-tiered system, monetary policy that’s looser for producers is simultaneously tighter for consumers.

This two-track system amplifies changes in money supply. When money creation eases, growth tends to tank, as it did in 2012. That’s a big reason why maintaining 6-8% GDP growth while “rebalancing” China’s economy—shifting away from investment and toward consumption-led growth—is so tricky.

It’s also why China’s debt makes interest-rate liberalization so fraught. Chinese businesses are already spending an eye-popping 39% of China’s GDP paying interest. Shifting money back toward consumers leaves less to go toward those payments. And that means lots of companies would go belly-up.