The financial media were buzzing yesterday after a BofA/Merrill Lynch report called the Jan. 27 bailout of a 3 billion yuan ($495 million) investment product in danger of going bust a “Bear Stearns moment.” The report’s author, rates strategist Bin Gao, was referring to the US Federal Reserve’s Mar. 2008 rescue of the investment bank Bear Stearns, which had saddled itself with mortgage-backed securities.

If you accept that analogy, the implication is that China’s “Lehman moment” —the equivalent collapse of a much larger bank or investment product—is nigh.

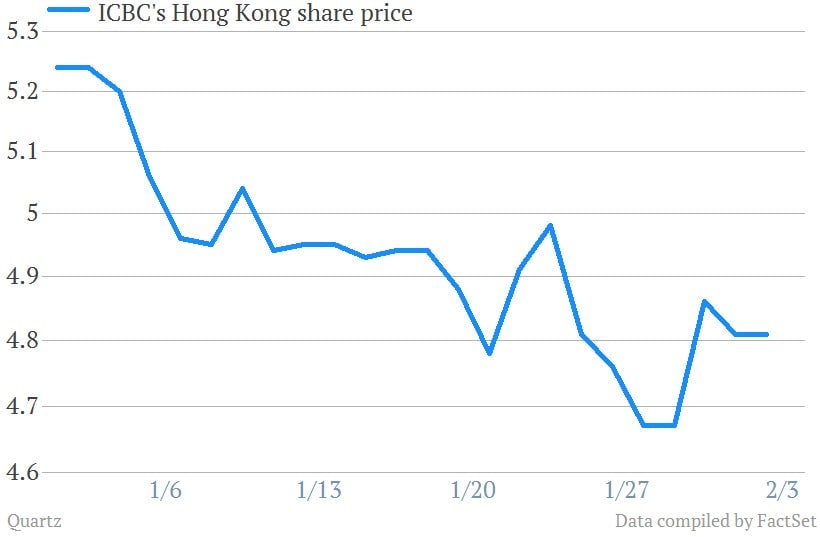

That hints at more turmoil ahead for Chinese banks. Judging by the share price of Industrial and Commercial Bank of China (ICBC)—which marketed Credit Equals Gold #1, the failed 3 billion yuan wealth management product (WMP), to its wealthier customers (a more detailed explanation here)—the market doesn’t seem bothered.

What’s more, shares of China Construction Bank, which has been embroiled in a similar WMP scandal, and of Minsheng Bank and China Merchant’s Bank, two non-state banks heavily involved in WMPs, jumped at least 2.4% the previous day.

What gives? Investors may think the worst is over for Chinese banks, but that’s a short-sighted view. Taken at face value, ICBC’s refusal to bail out the product’s investors may have set a precedent for other banks to so the same, said Mike Werner, analyst at Bernstein Research, in a note. (That said, since it’s unclear who the “mystery investor” buying rights to the WMP from customers actually is, it’s possible ICBC contributed money.)

Credit Equals Gold #1 customers made off like bandits, getting not only their principal back, but a guarantee of 2.8% on the product’s third and final year. That averages out to a 6.6% annual return. By backstopping the trust-product-gone-bad—and generously—the government has wrongfully instilled confidence in its banks and encouraged retail investors to keep piling into WMPs.

As of Q3 2013, the average trust company in the $1.67 trillion industry was deeply overleveraged, managing 43 yuan worth of trust assets for every one yuan in equity, says Gao. By comparison, the 20:1 leverage ratio of China Credit Trust, which originated CEG1, seems relatively constrained. But as Gao argues, CCT still would have found it extremely difficult to pay the CEG1 principle to customers had the “mystery investor” not stepped in.

At least one bigger trust default looms: Shanxi Liansheng, a mining company, owes WMP investors $5 billion. Gao says there’s been an uptick in the last few months of trust products warning customers about payment problems.

It’s not surprising that Chinese markets haven’t priced in this risk. As Bin Gao notes, the S&P 500 index didn’t peak until two months after the Fed bailed out Bear Stearns. Even so, China has plenty of near-Lehmans brewing.