Ten questions for Thomas Piketty, the economist who exposed capitalism’s fatal flaw

Thomas Piketty is in high demand.

Thomas Piketty is in high demand.

Thomas Piketty is in high demand.

The 42-year old French economist’s new book Capital in the Twenty-First Century offers a nerve-wracking argument: Because the return on investment tends to exceed the rate of growth, inequality isn’t an unintended consequence but an inevitable part of capitalism, and higher taxes on wealth are required to protect democratic society. Promoting the book in Washington, DC, he was mobbed at the International Monetary Fund, hobnobbed with president Barack Obama’s advisors and spoke at a panel that included economics Nobelist Robert Solow; in New York, he spoke at the Council on Foreign Relations and the United Nations. He also found time to sit down with Quartz. (This interview has been condensed and edited.)

Quartz: When you were beginning your research into income inequality in the late nineties, did you ever think you would wind up writing a book like this?

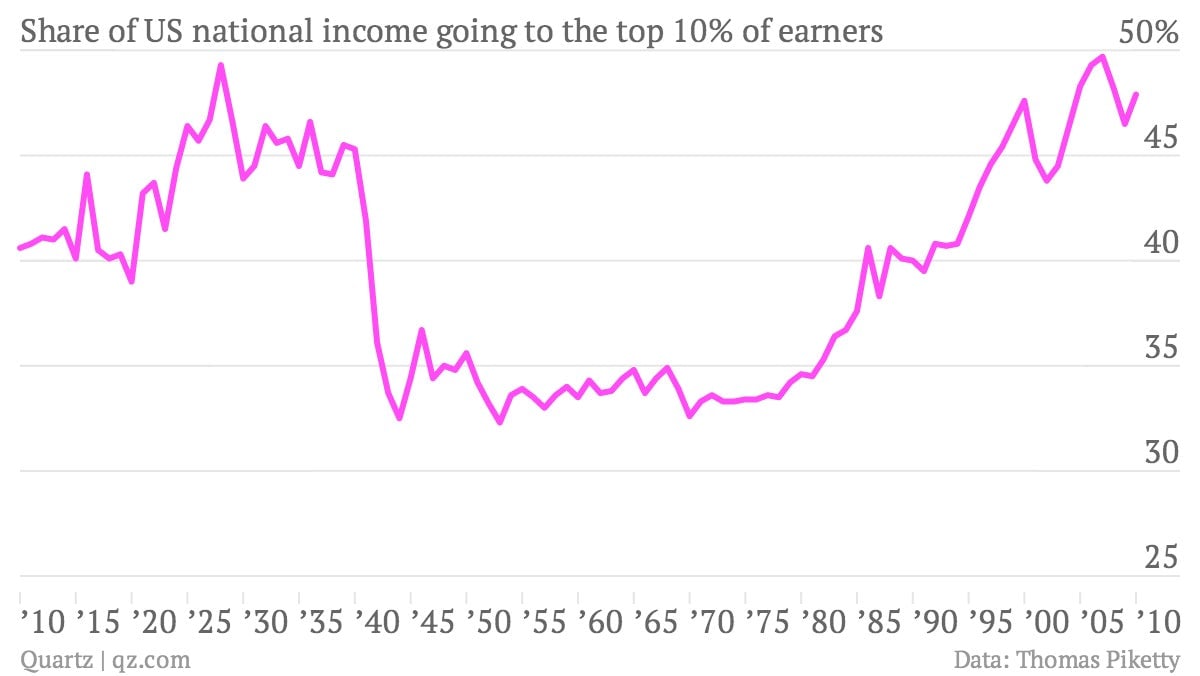

Thomas Piketty: I didn’t know what I was going to do. I started thinking, everywhere there is an income tax, there must be some data. I started asking people, economists, people at the ministry of finance. They all told me, ”no, there’s no data, it never existed, we’ve never heard of it.” I started digging into the old statistical publications of the finance ministry and I got to 1914 very quickly and I had the complete series of data. I remember this feeling of excitement the first time I realized I was going to be able to tell the complete story of how the structure of income has changed. It’s not only the number and the structure of income, you can see the different social groups changing over time. Even when we started doing it in the US a few years later with [collaborator Emmanuel Saez], we did not know at all we would end up with such a spectacular graph.

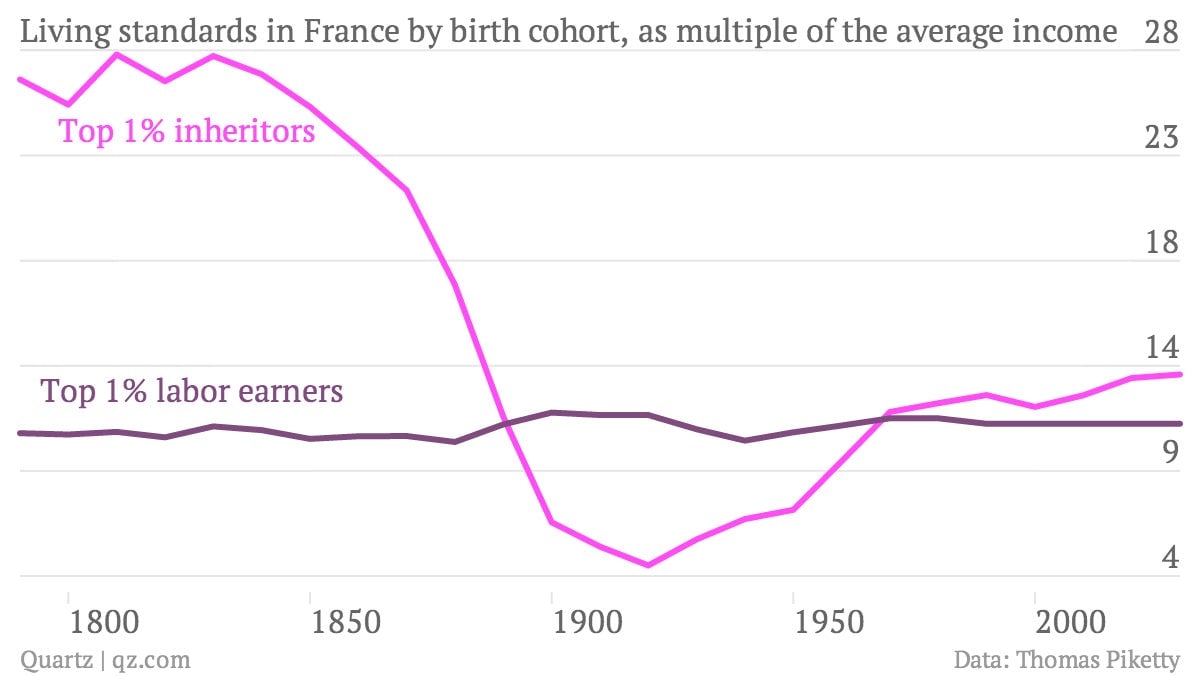

One element in your book that helps communicate that story are the literary references, particularly to Balzac’s Père Goriot—were they in your head before or did you introduce them to make it more intelligible?

This was in my head for a long time. Père Goriot, like every Frenchman, I studied it when I was in high school; I will not say that I’ve been asking these questions since I was in high school but probably for the last 10 years. The real question is, why is it that the relative importance of inheritance and labor income doesn’t seem to be as large as what it was [in the 19th century]? Is it that [the character] Vautrin was exaggerating or is it that something really deep that has changed, made inheritance lower in this society than it was in the past? Or are we in the long-run process of recovery? In the end I finally realized that it was largely a long process of recovery.

I’m not saying that we are going to return to exactly to the same extremes of wealth because the concentration of inheritance, at least in this stage, is much less extreme than it was at the time of Père Goriot. In the aggregate, the magnitude of inheritance might return to this level.

One criticism that has been raised about your findings on inequality is that they may be skewed by the growing number of elderly people living off savings than in the past, which would naturally increase capital’s share of income.

The issue is the possible rise of life-cycle wealth—has class war been replaced by the war of generations? The war of generations is much less frightening than class war, because after all, everyone is going to be young and old, and if all wealth is just about shifting your consumption to your old age, everybody’s going to be rich at some point. This is perfectly true that we have more life-cycle wealth today than we used to have, but it is much less true than we typically imagine.

In counties like the US and UK the share of pension wealth or life-cycle wealth in total wealth accumulation has increased. But even when it has increased, it is up to 20%, which is a lot, but it leaves 80% of the wealth that’s not pension wealth. There are many other reasons why people accumulate wealth beyond simply saving for their old age. If most of wealth accumulation was life-cycle, than the concentration of wealth should be in line with the concentration of labor income, it should not be so much bigger. The last thing is that in the data that we have, including the data that Emanuel Saez and Gabriel Zucman have just constructed (pdf) for the US, what we call pension funds, within this aggregate, it’s not all annuitized wealth—some of it can be transmitted to the next generation.

There have been some American reviewers who have found your book to be very deterministic in assessing the inevitability of inequality and the challenges of constructing an effective response. Is there an undiscussed assumption about political economy behind the book?

But there is a whole continuum of possible policy response! I don’t recognize myself at all in these reviews… I am not fatalistic at all, I certainly don’t believe that it’s all or nothing response. What’s probably inevitable is [investment returns being] bigger than [economic growth], that’s economics. In terms of politics, everything is possible, nothing is inevitable. [The United States] has a property tax which is a pretty big wealth tax. I would prefer it to be a progressive tax that was proportional and I would prefer it to be on net wealth rather than the gross value of real estate—if you take someone whose house is $500,000 and they have a mortgage liability of $490,000, his net wealth is $10,000, I would propose he would pay no property tax, no wealth tax. Right now he is paying as much property tax as someone with no mortgage who inherited his apartment 20 years ago. My premise is not to tax to destroy the wealth of the wealthy, it’s to increase the wealth of the bottom and the middle class.

I am not terribly impressed by people who know for sure what will happen or not. What would they have said in 1900 or 1910? I’m sure many of them would have said there will never be a federal income tax because of the constitution. For a large country like the US—the US is one quarter of world GDP—the US has ample power to put sanctions on Swiss banks. You know, five years ago, people were saying it’s not possible to break bank secrecy in Switzerland, but you know, you put the right sanctions, you break it.

To push a little on this, a lot of American commentators they see the economic reality you lay out in the book, and say to themselves, wealth is hugely influential in the political process and will block these kinds of changes.

So they are more cynical than I am. It’s not that I am so optimistic, I understand this argument, I’m just saying, I guess, the best way to try to counter this cynicism is to say what we think is right. In Europe, prior to World War I and prior to the Bolshevik Revolution, the political system was not really responding to the huge inequality of 1900 and 1910, but in the US, the democratic institution in a way did deliver more than Europe. One way to read what I am saying is, we should try to respond another time, we should have a revival of progressive income taxation, and we should have a new invention which is progressive wealth taxation. Certainly, it is much less complicated than many other challenges we are talking about, like a global tax on carbon emissions.

Another criticism of the book is that you are too quick to assume that labor and capital will be interchangeable in the future, perhaps due to growing automation—can you respond to that?

So I’m not really taking such a strong stance on this. I’m saying, this is a possibility and even a small departure from the usual Cobb-Douglass assumption [an economic model of the extent to which labor, capital and technology can replace one another while still doing the same job], we don’t have to go all the way to a robot-type economy for the long run to be a bit frightening. Minimal departure from a standard economic assumption can get you a capital share that keeps rising, not to 100% of national income, but you know it could keep rising from 20% 20 years ago, 25-30% today, 35-40% 20 years from now. That would be a huge political shock.

All I’m saying is, of course we don’t know, but let’s try to design institutions that can respond, if necessary, to this possibility. If we don’t need to respond because the capital share does not increase, because the rate of return to wealth is not much larger than the growth rate because we managed to have very fast innovation so that wealth inequality stops rising, that’s fine, I will be very happy. But we cannot just wait for this incredible coincidence to happen. There’s no pilot in the plane, there’s no natural force that will make this incredible coincidence of pushing the growth rate toward the rate of return happen, and so we need to find another plan in case this does not happen.

One reason your book has attracted so much attention is that it’s kind of magisterial—someone jokingly asked if economists are even allowed to title their books so grandly anymore.

You know, it’s more ambitious and more modest in some ways. What I’m pushing for is an economic discipline that will be closer to other social sciences, in particular, we should be more pragmatic about the methods that we are using, instead of pretending that we have our own scientific apparatus with very sophisticated mathematic models that distinguish us from sociologists and historians. I’m not the first one or the only one to push for this kind of historical approach to political economy. If you think of it, the book by Milton Friedman—the Monetary History of the United States, it’s very different from my book and I certainly do not want to compare myself to Friedman—but it’s not sophisticated in terms of techniques but it is a very careful historical account of a very specific issue. I disagree with a lot of his conclusions, but the power from his book came from the fact that he was very meticulous with the historical account.

Economists have put themselves in a position where what they are doing is supposed to be impossible to understand for outsiders so they don’t even talk, sometimes not even with their girlfriend or boyfriend or friends about what they are doing. It’s certainly worse today than it was ten years ago, you are wrong to think that the financial crisis or inequality will change this, it will take a lot.

Talk to me a little about how the book is being received in France, where it was published last fall.

There was a lot of interest in the historical perspective, but the immediate policy concerns are different. The big issue is, how do we go to closer political integration within the European Union, within the euro zone? is it possible to have a common currency without a common fiscal system?

The big message the book that is trying to get through, and in France it has started to get through but not as much as I would like it, is that we have a lot of common debt but we have a lot of wealth. The economic fundamentals of Europe are much better than what we usually see, so it’s a problem of institutions. Our federal institutions are completely dysfunctional, they don’t work at all. We need fiscal coordination. We are asking the Greeks to make their wealthy citizens pay more tax—which is a perfectly reasonable demand except that we don’t help them to do that. If it’s so easy for wealthy Greek citizens just to transfer their money to a German bank or to a French bank, its completely crazy. There’s no example in history of nations in peacetime deciding to disappear and become something bigger. It’s difficult. But still we could do better. Right now, the political parties in France I think are—in a way, I think the Germans are more ready for political integration than the French…

I think that would surprise a lot of people, to hear you say that.

The French politicians are very hypocritical, it’s very easy for them to say this is the fault of the Germans, but at the end of the day, several times in the past 15 years Germany started to make proposals of political union and it was really the French politicians that did not respond. [France’s socialist President François Hollande] is saying “I want a common public debt” but then he still wants to have a separate choice of the level of the deficit for France and Germany, which makes no sense. The Bundesbank president, who is not a nice person, who is certainly very conservative, it was very easy for him to respond, “look, if you have a common credit card you can’t do shopping separately.” If France was really making a proposal in a vote on a common deficit level for the Eurozone in exchange for the common debt, Germany would be afraid to be put in a minority by France and Italy.

The other important debate is very different from the US—we have 50% of GDP in tax, there’s a lot to do to try and simplify the tax system, make it more efficient. In France, the big issue is not we have huge rising inequality like in the US. It’s true, I was opposing Hollande for this 75% tax rate above one million euros because I thought this is not the main issue. There are many issues of reforming the welfare state, making it more efficient and sustainable for the 21st century that are very different from the US.

One difference is the “super-manager”—the executives who are paid much more, proportionally, than executives were in the past. Some of your critics point to the Forbes 400 list of US billionaires to point out that many of them are entrepreneurs. If there is mobility to let people reach that level of wealth, does the relative inequality matter?

This 400 billionaire ranking, by construction, underestimates heirs and overestimates the fraction of entrepreneurs. This is first for ideological reasons: Clearly Steve Forbes loves entrepreneurs, and he himself is an heir, his grandfather created Forbes, but he doesn’t like that. And, because heirs are more difficult to spot: They typically have more diversified portfolios. When you are an entrepreneur, you have founded your own firm, it is so easy to find that you exist, you are the main shareholder of your company, it is very easy to look at the stock market position of your company to know how rich you are. It’s not like they have a registry of wealthholders, their basic methodology is to try and make phone calls. It’s very hard to find people who have a diversified portfolio, especially if they don’t want to be on the list. Whereas entrepreneurs always want to be on the list. I don’t know exactly, but I think we should not overestimate this mobility.

The final thing: Top managers have a way to access huge wealth without being an heir. The problem, of course, is for the people who are neither top managers nor top wealth holders, they lose on both grounds.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.