Asia seems bound for a natural gas shakeup pitting the US against Russia—which could benefit consumers, but also deal a potential hard blow to current and future producers, such as Australia and east Africa.

Asia seems bound for a natural gas shakeup pitting the US against Russia—which could benefit consumers, but also deal a potential hard blow to current and future producers, such as Australia and east Africa.

The trigger for the shakeup is a critical mass of US and Russian gas exports destined for Asia over the coming decade and beyond, much of it likely to be priced at a substantial discount to the liquefied natural gas (LNG) currently on sale in the region.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

LNG sold in Japan last month for about $15 per 1,000 cubic feet, and in February, it went for more than $20. But in May, Russia committed to sell 38 billion cubic meters (bcm) of gas per year to China at half that February price—an estimated $10 per 1,000 cubic feet. When US LNG produced from the shale gas boom begins to reach Asia next year, Citi estimates that it will sell for about the same price–$10 to $12 per 1,000 cubic feet.

The US and Russian gas will compete with existing and planned LNG projects around the world toward the end of the decade. According to numbers compiled by Citi, Russia could supply 30 bcm of gas to China by 2020 and as much as 95 bcm to Asia as a whole by 2025. The US is in approximately the same posture—seven export projects in various stages of approval could export 93 bcm of LNG in a similar time frame. The combined potential US and Russian volume is equivalent to more than 3 million barrels of oil a day.

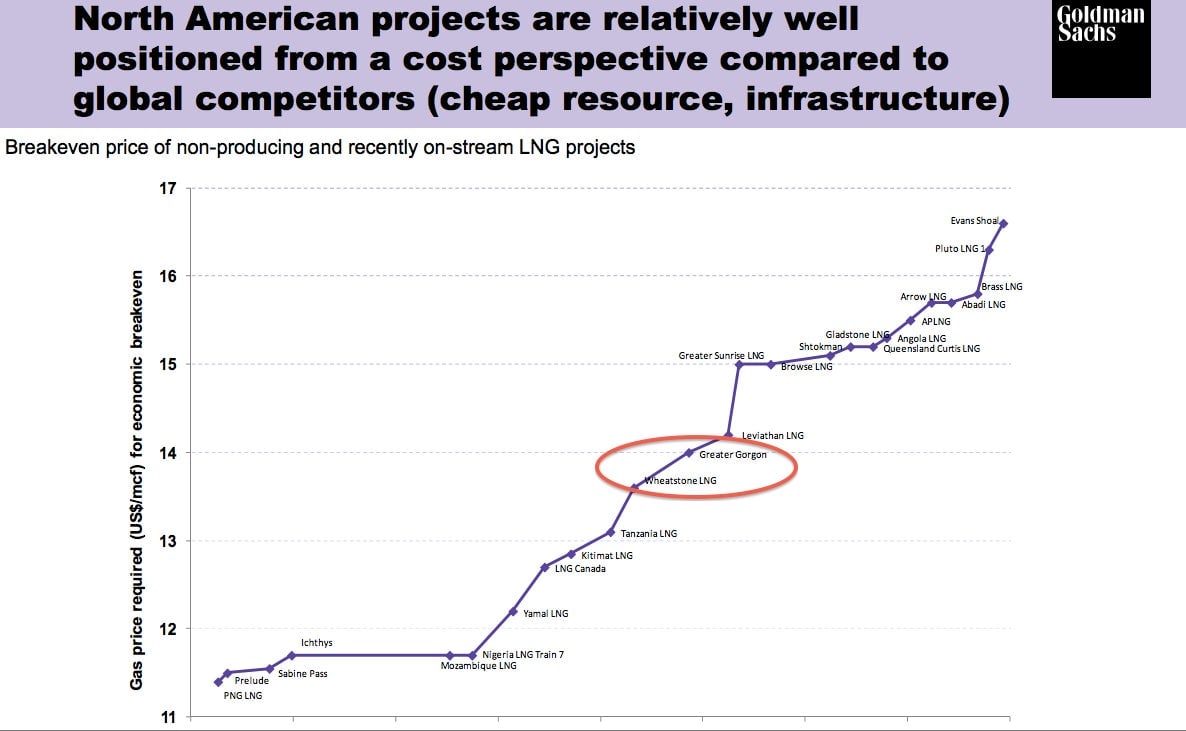

Among the projects whose economics could be challenged are Chevron $CVX’s Gorgon and Wheatstone LNG projects offshore from Australia. In a report last year (pdf, slide 32), Goldman Sachs $GS said the two projects require a gas price of $13.50 to $14 per 1,000 cubic feet to break even. Others in possible trouble are east African LNG projects in Mozambique (which need about $11.50 to break even) and Tanzania ($13). Proposed Canadian LNG projects are also at risk of becoming uneconomical. Here is the Goldman chart:

In a note to clients today, Eurasia Group’s Leslie Palti-Guzman said that, as a result of the price impact of the Russia-China deal in particular, new Australian LNG projects are unlikely, and the development of projects in Mozambique and Canada could be delayed.

Chevron has sold much of its Australian LNG production in advance, and some analysts suggest that high-priced LNG may survive more or less intact despite the encroachment of the cut-rate competition. IHS’s Kelli Maleckar says that prices across Asia will vary. “You might see North American LNG projects getting slightly lower average prices from China, but the impact when mixed with prices received for deliveries to the rest of Asia will be fairly muted,” she told Quartz.

But if Europe is a lesson, Asian LNG buyers are likely to initiate a price renegotiation once the competing US and Russian volumes show up at such a substantial discount—and to secure lower prices. Such pressure will continue for a number of years if analysts are right that a surplus LNG market will emerge in Asia toward the end of the decade.

But to the degree that demand soars unexpectedly—a possibility given China’s politically driven shift from coal-fired to gas-fired electricity—prices could stabilize in the middle, moving toward $14 per 1,000 cubic feet. Even at that price, the Australian projects could be only marginally profitable.

Chevron declined to comment. Anadarko, one of the major LNG developers in Mozambique, did not respond to an email.

Commerce usually operates on a different plane from politics, and as the low-price sellers, the US and Russia may end up amiably sharing the Asian spot market. But, depending on demand and the size of their own supply, they could just as well end up in savage competition for market share.

Russia does not fear US shale gas in Europe because it can supply the continent at a much lower price. But neither will it have a distinct price advantage in Asia, the fastest-growing region for energy demand. There, with the high-priced gas producers struggling for survival, the US and Russia would slug it out. The only certain winners will be consumers.