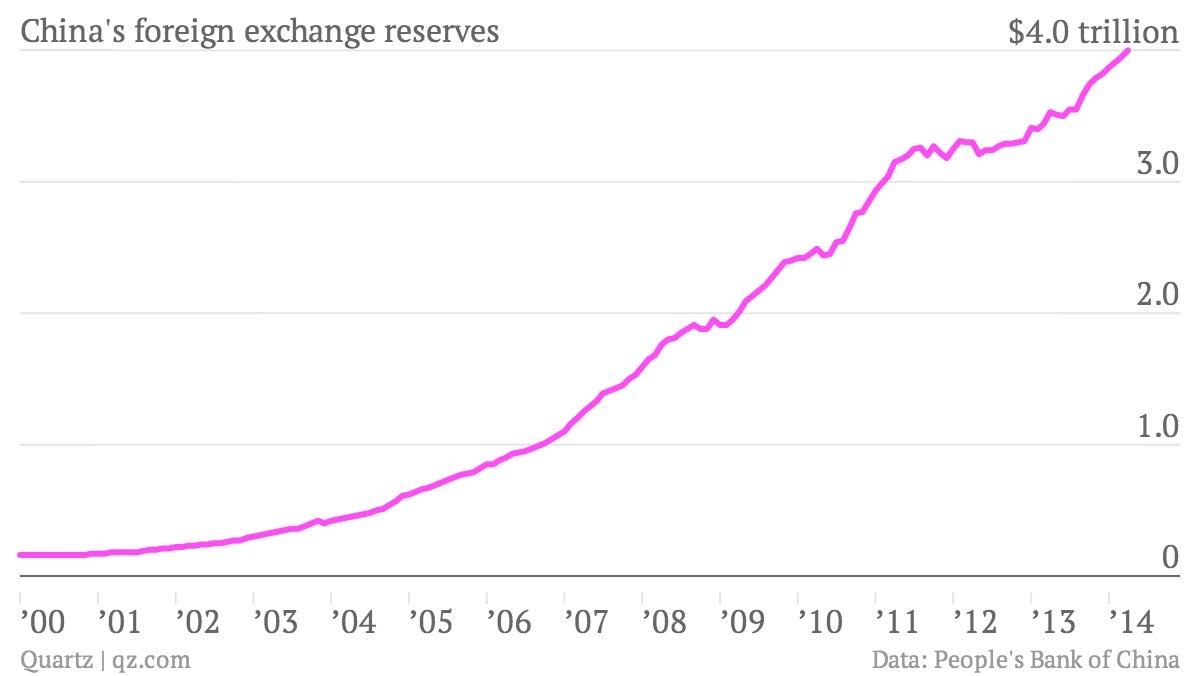

China’s foreign-exchange reserves hit $4 trillion in the second quarter of 2014, according to Chinese government officials. That’s so massive it exceeds the next six biggest national reserves combined; so huge that it equals nearly half of China’s GDP.

China’s foreign-exchange reserves hit $4 trillion in the second quarter of 2014, according to Chinese government officials. That’s so massive it exceeds the next six biggest national reserves combined; so huge that it equals nearly half of China’s GDP.

It certainly sounds impressive. But China’s foreign currency reserves are not just money lying around to be used for anything. Understanding what they can and can’t be used for highlights the fact that they’re not the bulwark of Chinese financial stability that many assume.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

“Reserves are less powerful than maybe people think they are because they’re really only good for one or two things,” says Andrew Polk, an economist at the research group The Conference Board. Here are some of the things they can be used for:

Many assume that foreign currency reserves can be used to bail out banks in the event of a financial crisis. This isn’t a totally daffy conclusion to draw; between 2003 and 2005, China injected some $60 billion of its reserves into debt-swamped Chinese banks via some fancy accounting.

But it wouldn’t be so easy this time, as Capital Economics, a research firm, flags in a recent note. Here’s what those foreign currency reserves can’t do:

If banks start needing bailouts, there’s nothing saying that the PBoC absolutely cannot use its foreign exchange reserves to give them new money. Through more deft accounting, it certainly can gradually reshuffle money around. And it can do so in ways that don’t even look like a typical banking bailout.

However, that would ultimately mean shifting corporate debt onto the Chinese government’s already expanding balance sheet. And as Japan’s eerily similar debt surge a couple of decades ago showed, no amount of foreign reserves can help once a government starts drowning itself in debt.