With one day left to pay its creditors, Argentina appears to be heading for a voluntary default.

With one day left to pay its creditors, Argentina appears to be heading for a voluntary default.

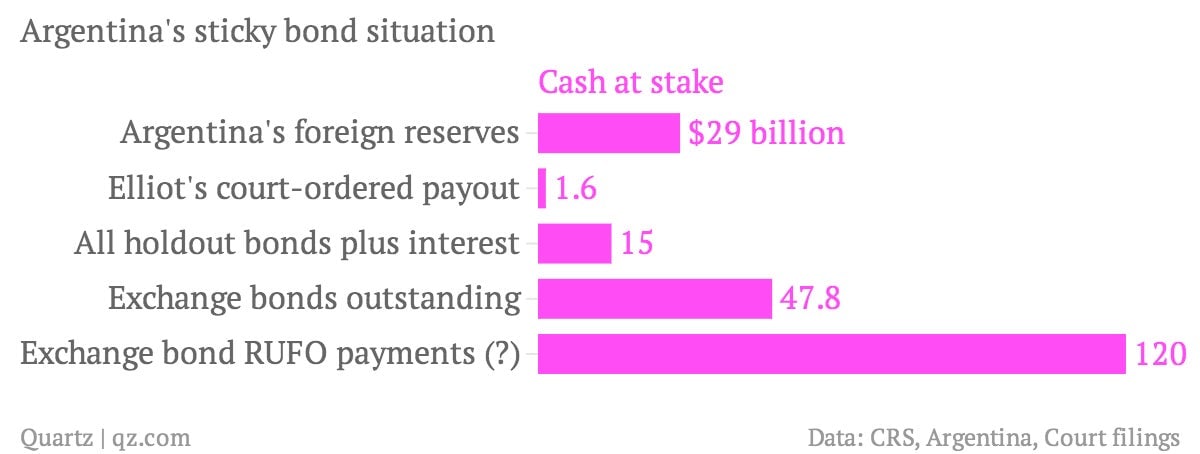

If you’ve been following the debt saga of Latin America’s third-largest economy, you know things are a mess: A decade of restructuring following Argentina’s record default in 2001 helped the country reduce its borrowings through two debt exchanges, but a small minority of creditors held out and demanded full repayment. The sovereign bonds in question were issued under New York law. After years of litigation, subsidiaries of Elliott Management won not just a $1.6 billion settlement, but a judge’s injunction that would block Argentina from paying anyone unless it paid the holdouts, too.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Now, Argentina is out of appeals. The deadline to pay creditors was July 1, and while the country put a $539 million interest payment for the exchange bondholders in escrow, it didn’t actually pay them or the holdouts. On July 30, a 30-day grace period ends. If Argentina can’t reach a deal that satisfies the holdouts and persuades them to ask for the injunction to be lifted, it’s default city.

So far, Argentina’s delegation in New York has yet to even meet with the holdouts, instead working through a mediator. Even as they negotiate, Argentina’s president, Cristina Kirchner, has continued to talk tough, for example calling on the holdouts to accept the 50% to 70% haircuts imposed on the holders of the exchange bonds.

There’s still time for a last-minute compromise, and Argentina in theory should be motivated to reach one. Policies that the government has adopted in the absence of foreign lending and investment have left the country vulnerable to inflation and recession; settling the default threat could promote the return of foreign capital.

But it’s not that simple. Kirchner has made not paying the holdouts a key part of her political pitch, and battling foreign vulture funds is easier than fighting corruption charges (paywall). And then there’s the math: paying the holdouts means adding $15 billion in obligations, about half the country’s current foreign reserves. If the government goes this route, it will want to string things out for maximum leverage.

Argentina’s latest delay gambit involves clauses in the exchange bonds regarding RUFO (Rights Upon Future Offers) payments. Argentina says that if it reaches a compromise with the holdouts, it may have to provide the same deal to the exchange bondholders, which could cost the country anywhere from $120 to $500 billion in extra payments, depending on how hysterical your source is. So the government would prefer to delay payment until the end of the year, when the RUFO terms expire, but even that might not be necessary—at the last minute, European exchange bondholders offered to waive their RUFO rights in an effort to convince the US court to stop blocking the interest payment, avoid a default and give the parties more time to reach a deal.

But a default could, weirdly, benefit the exchange bondholders: They would start accruing interest of 8% on their absent coupon payment—a decent take in a low-rate environment. But it wouldn’t be so great for Argentina’s bottom-line. Nor would the country want bondholders calling in clauses demanding immediate repayment, which also would put pressure on Argentina’s limited foreign reserves.

Speculation persists that Argentina will still try an end-run around the situation by offering yet another exchange, this time for bonds under Argentine or European laws instead of those in US jurisdiction, but this would give creditors the upper hand, and with it a chance to extract more cash from Argentina.

And none of that includes the likely economic costs of a default, such as a recessions and further complications to government finance in Argentina.While holdout bondholders who spoke with Quartz anonymously say they are hoping for an 11th-hour deal, the clock is ticking without much movement.