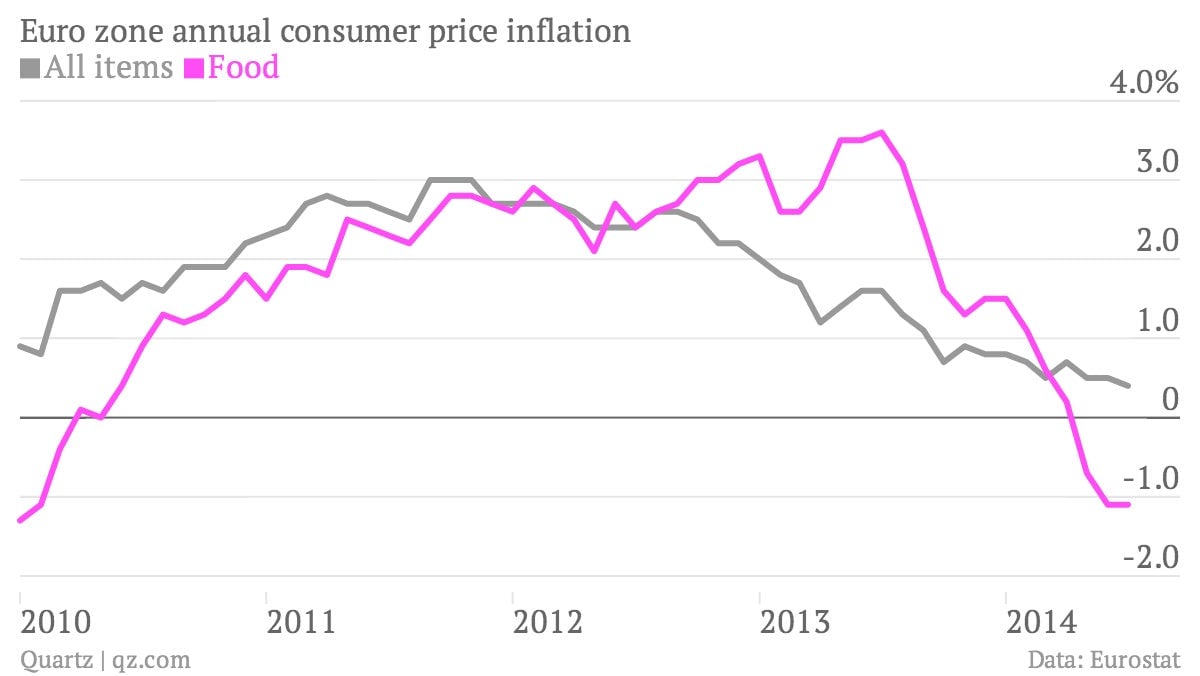

The euro zone has been flirting with deflation for months, with prices rising by a mere 0.4% last month, the weakest rate in years. As prices slip further and further from the European Central Bank’s 2% target, the risk of the “Japanification” of Europe grows.

Like Japan in the 1990s, countries such as Greece, Spain, and Portugal are already suffering from outright deflation, while consumer prices in Italy were flat in the latest monthly reading. Falling prices discourage consumers to spend and make repaying debts more difficult—problems that the euro zone’s hard-hit “periphery” could do without at the moment.

The ECB unveiled emergency stimulus measures to kickstart growth in June, which will take effect next month. The central bank says that this will head off the risk of deflation.

But the forces dragging down prices in the euro zone recently gained an unlikely ally: Vladimir Putin. Russia’s embargo on European food imports last week is already causing angst among European farmers, with the EU stepping in to support plunging peach and nectarine prices earlier this week. More emergency assistance for fruit and vegetable producers will come next week, the EU’s agricultural commissioner says.

Food prices in the euro zone fell at a 1.1% annual rate last month, with 14 of the bloc’s 18 members recording falling prices. And that was before the Russian embargo:

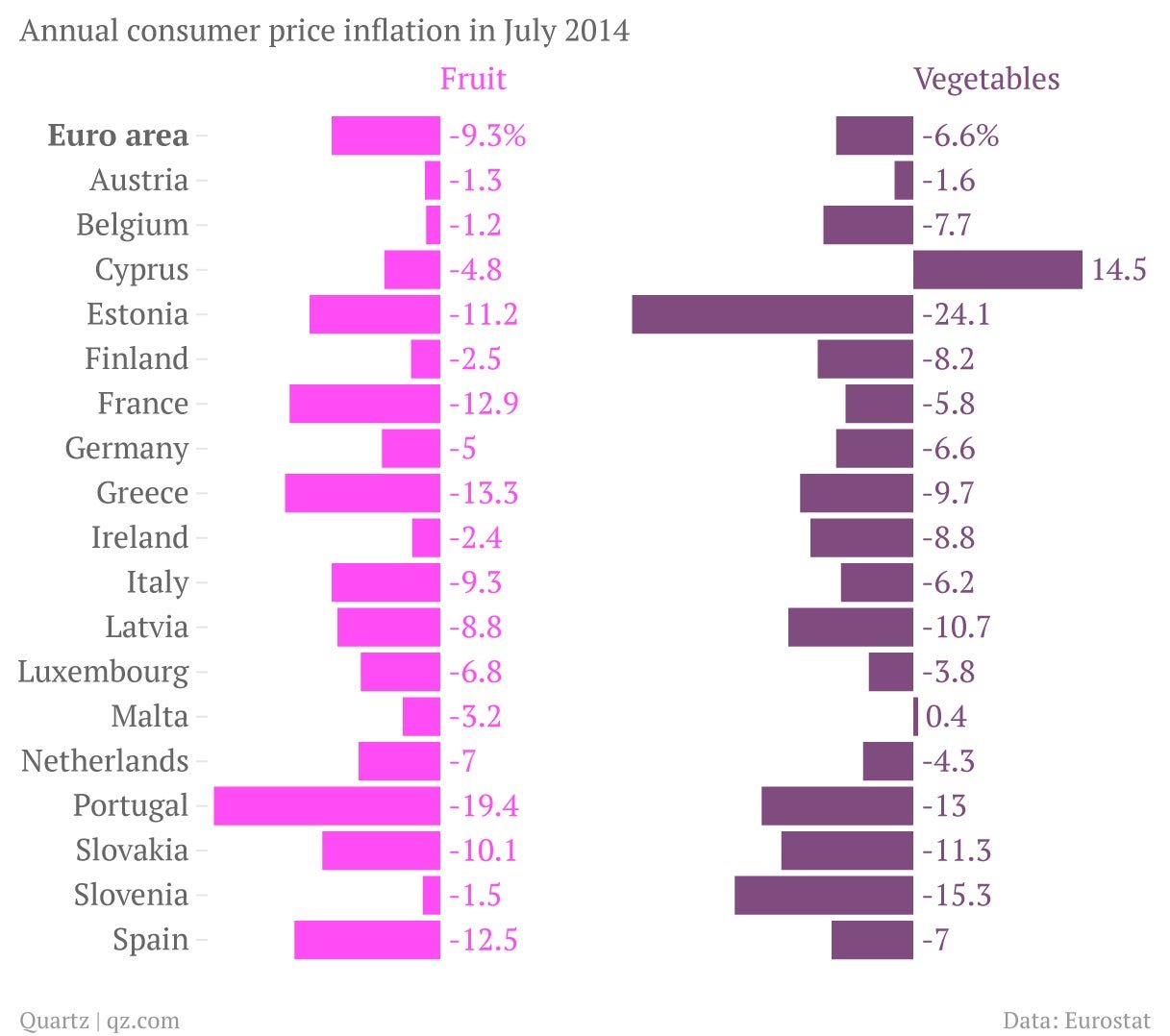

Now that one of its largest export markets is off-limits, the combination of healthy harvests and tepid demand that has pushed down prices of European produce in recent months will probably get worse before it gets better. And it’s already pretty bad:

Last month, falling fruit and vegetable prices alone were responsible for shaving 0.24 percentage points from the euro zone’s headline inflation rate (which, remember, was only 0.4% to begin with).

Of course, policymakers routinely exclude volatile categories like food and energy from their preferred measures of “core” inflation. But officials cannot ignore the costs of supporting food producers hit the hardest by the Russian embargo, and it’s not as if core inflation (0.8% in July) is that much higher than the index that includes food. Ordinary people do not think in such abstract terms—a prolonged period of falling prices at the supermarket might make them think that prices of other things should be lower as well, sparking a broader-based deflationary spiral that’s a much bigger problem than a glut of unsold peaches.

Japan’s experience with deflation showed that once it sets in, it is extremely hard to shake. European officials stress that escalating sanctions are more damaging to Russia, and they may be right, but that doesn’t mean that the cost of Russia’s retaliation can be so easily dismissed.