The British pound hasn’t been linked to gold since 1931. The US snipped the cord in 1971. But the Swiss only fully severed ties to gold in 1999, when voters approved a revamped constitution.

Now, a good chunk of them seems to want to go back.

On Nov. 30, Swiss voters will cast ballots on a number of issues including the “Save our Swiss Gold” initiative launched by the right-leaning Swiss People’s Party. The ballot measure would instantly ban the Swiss National Bank from selling gold. It also would require that the national bank keep 20% of its assets in gold within five years. (It currently has about 8% in gold.) Oh, and it would demand that all the gold be stored in Switzerland itself. (About 30% is parked abroad right now.)

“It’s really an attempt to return to some kind of gold standard, for those who don’t trust paper money and who want gold backing it up,” UBS strategist Beat Siegenthaler told Reuters.

While it’s not strictly the same thing as a gold standard—for instance a classical gold standard stipulated that national banknotes be freely converted to gold at a fixed price—the Swiss gold initiative is a step in that direction.

What’s the motivation, exactly?

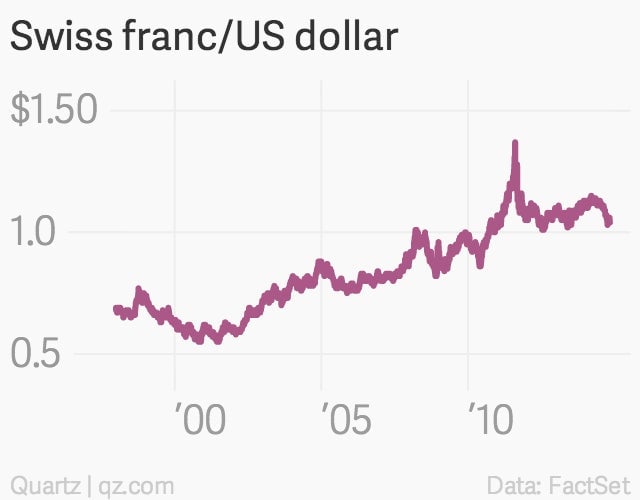

It would be one thing if we were dealing with a basket-case currency and rampant Swiss inflation. But Switzerland’s currency problem, ever since it cut ties with gold, is that the franc has been far too strong, not too weak. That’s acted as a drag on the Swiss economy’s high-value export sector. In fact, it’s been such a problem that the Swiss National Bank has taken big—some might say risky—steps to smack down the currency, the effects of which would likely be reversed if the bank were forced to buy more gold.

As for the repatriation stipulation, if Switzerland’s vast holdings of gold were parked with the Central Bank of Argentina, well, ok then. But the Swiss National Bank says 70% of its gold already is in Switzerland, while the rest is slumbering quietly at the Bank of England (which holds 20%) and the Bank of Canada (with 10%), not exactly the most heterodox institutions in the world.

And the worst part of the proposed law, according to a Swiss National Bank official by the name of Jean-Pierre Danthine, is the provision that Switzerland must never, ever sell gold again. He explained in a recent speech:

In combination with the obligation to hold at least 20% of total assets in gold, this could gradually lead the SNB into a situation where its assets would mainly consist of gold: each extension of the balance sheet for monetary policy reasons would necessitate gold purchases, but whenever the balance sheet needed to be reduced again for the same reasons, we would not be able to resell our gold holdings. This would severely restrict our room for manoeuvre.

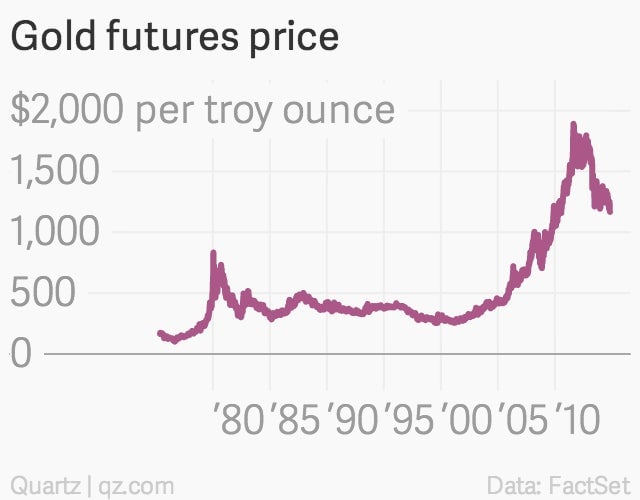

From a purely tactical point of view, it would be deeply silly to double down right now on gold, which gained in value during the financial crisis but has since slid from its peak in 2011 at nearly $1,900 an ounce. Committing to buy now would essentially be a giant bailout for speculators in the gold markets. Bloomberg reports that, given the Swiss National Bank has some $544 billion in assets on its balance sheet, the gold initiative would force it to buy more than $56 billion worth of physical gold over the next five years. And if current price trends continue, the value of that gold would be falling.

In short, the Save Our Swiss Gold initiative doesn’t make sense economically. (Luckily its chances of becoming law are slim—it would need to win outright in a popular vote, and also in the majority of cantons that make up the Swiss Federation.) But referenda like this and the one Swiss voters recently passed to clamp down on immigration really aren’t about economics. They’re about the increasingly influential rightward drift of European politics, which threatens to result—especially in the case of the Save our Swiss Gold initiative—in some really terrible policies.