In a way, the message of OPEC’s inaction today—deciding not to cut supply—is analogous to the challenge that confronted GM and Microsoft in recent years: if it wants to remain relevant in a world it once dominated, and at times made tremble, it needs to change its game.

In a way, the message of OPEC’s inaction today—deciding not to cut supply—is analogous to the challenge that confronted GM and Microsoft $MSFT in recent years: if it wants to remain relevant in a world it once dominated, and at times made tremble, it needs to change its game.

For much of the rest of the world, including great power-consuming nations like the US and China, the message is very different—that of an ill-defined but temporary window in which to solve big strategic problems until very recently thought to be intractable.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

The trigger for this new state of affairs is dual—the US shale-oil boom, which has wholly muffled the geopolitical disruptions behind previously skyrocketing oil prices, and soft demand from a transforming Chinese economy.

On the sidelines are menacing new supply threats to the status quo—even more oil from the US in the coming three to five years, from Iran in the not-far-fetched scenario of a nuclear deal, and from till-now war-constrained Iraq and Libya.

Traders have observed all this supply, detected no basis for a surge of demand, and sent prices plunging. Just today, futures of internationally traded Brent crude plummeted as low as $71.25 a barrel, down 41% since peaking for the year in June at $115.71. US-traded West Texas Intermediate—the pricing basis for shale oil—fell more than $5, to as low as $67.75 a barrel, puncturing another threshold.

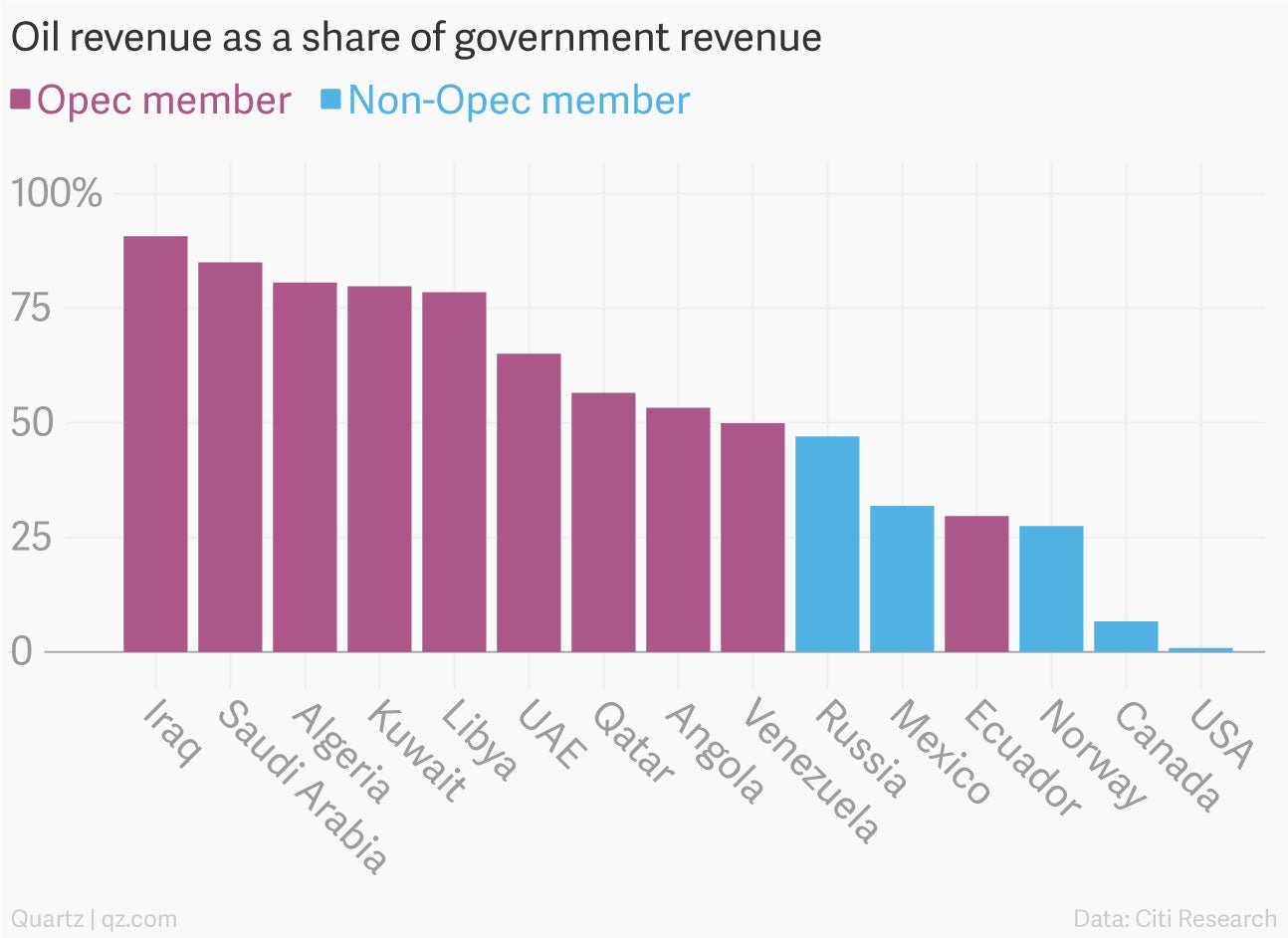

Members of the OPEC cartel have desperately flailed away, given that most of them cannot meet their state budget obligations at such prices (see chart below).

Iran, Iraq, Angola and Venezuela pushed hard for a cut, but finally they were made to understand—probably with patient explanation by Saudi Arabian oil minister Ali al-Naimi, OPEC’s effective leader—that no cut would remove the threat. If OPEC managed today to raise oil prices, that would improve the profit picture for US shale, too, and encourage American drillers to send even more supply into the market; before long, OPEC would be back at the same point of having to cut.

As a result, OPEC decided to wait for the market to balance. But this wait could be years—no one knows when, how, and even whether demand will pick up sufficiently to sop up the excess supply; similarly, everyone knows that the US shale boom won’t persist forever, but not when precisely it will tail off.

OPEC hopes—and most analysts presume—that eventually things will revert to “normal,” at least the version of normal that existed the last four decades, in which the cartel became one of the most formidable fixed objects in the global economy.

But that is not guaranteed. One scenario has the shale boom persisting through 2040; by then a big breakthrough could happen in battery technology, making electric cars more competitive, and removing a pillar of future demand growth projections. In that case, OPEC would be permanently neutered. There is simply no telling whether OPEC’s familiar world will return.

Until now, global policymakers have relied on a few presumptions in determining their strategic goals, among them that OPEC and other oil collossals like Russia would remain in commanding positions of leverage, and that scarce resources would lock in one source of friction between China and the West. Because of these fixed realities, Russia and OPEC, when they took an action, could seem to be forbidding forces; they did not seem to need to taper their ambitions in order to get along with the world. In addition, America’s decline seemed steep and inexorable.

But lower oil prices have knocked out the legs underpinning these assumptions. For starters, they mean that many of the countries with the most assertive foreign policies—Russia, Iran and Venezuela among them—are in fiscal trouble. The key fact here is that they could be in this fix for many years to come, and to the degree lower oil prices persist, the less likely they will be able to sustain policies that upset powerful other countries.

For consuming nations, the prudent posture is to view this time of lower prices as a temporary window—a period to last, say, through 2020 or 2022. And, wherever you are sitting, to pose the question—strategically speaking, what do you want?

If you are the West, would you like Iran to convincingly renounce the development of nuclear weapons? For Russian president Vladimir Putin to temper his adventurism? Then, speak quietly and unprovocatively, and keep pushing—low prices will maintain the pressure and could eventually prove decisive.

If you are an oil-producing state, this is a wake-up call to diversify your economy away from oil.

Much of the change will be chaotic, and the plunge of revenue could create more political instability in the Middle East; it will create some degree of greater oil demand, thus exacerbating climate change.

But most of the changed situation is not yet obvious—this is new terrain and will require policymakers to be alert. The main thing is simply to recognize and not be caught unawares that we are in a new age, and not to be lazy and view it as permanent.