Lowflation.

All of a sudden this not-so-clever portmanteau is everywhere.

But what it lacks in wit, it makes up for in usefulness.

Large chunks of the emerging global economy—including Brazil, Russia and China—are slowing. Established economies such as Germany and Japan aren’t growing like gangbusters. And oil prices are collapsing. All of that adds up to a global decline in prices that is scrambling financial markets and economic expectations. The latest evidence? The euro zone slipped into outright deflation in December, with prices falling 0.2% year-on-year.

The flurry of economic and market outlooks recently published have been liberally peppered with references to lowflation. (Here are a smattering, bolding is ours.)

Goldman Sachs $GS: A mechanical reduction in core inflation could have an important impact on monetary policy, especially if other indicators such as wages remain consistent with continued lowflation.

Nomura: With a global disinflationary shock, we think market participants will be more confident about the Federal Reserve and the Bank of England’s ability to address the lowflation issue.

Morgan Stanley $MS: In our view, the dominant macro theme in 2015 will be central banks’ battle against lowflation–excessively low inflation that has become pervasive, persistent and pernicious.

Proliferation of the term lowflation suggests a shifting mindset in financial markets, as investors come to expect perseverant low or falling prices. The difference between that and ”deflation,” is just a matter of degree. When widespread, enduring price declines are seen to be the norm, it can spark a vicious cycle of falling profits, investments, jobs and income, which in turn further depress economic activity.

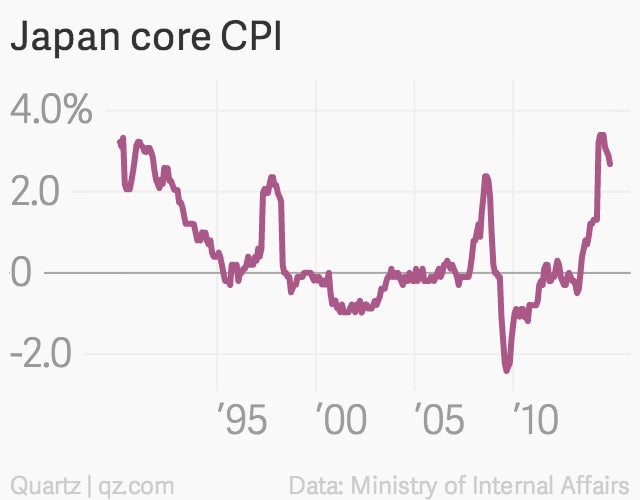

That negative feedback loop has proven very difficult to break (see Japan’s decades-long wrestling match with deflation).

Economic policymakers are anxious to prevent this mindset from spreading across Europe, one of the world’s largest economic entities. The European Central Bank has a chance to do so at its upcoming meeting on Jan. 22, by moving toward a Federal Reserve-style bond buying program, known as Quantitative Easing, or QE.

But policymakers are divided about whether such measures, which aim to lower borrowing costs to boost spending and investment, would be effective. After all, yields on long-term Spanish debt, for example, are already below 2%. So it isn’t borrowing costs that are keeping businesses from investing. It’s the tight credit from Europe’s crippled banking system and the horrific state of many of its largest economies. (Italy’s unemployment rate is a record 13.2%. That’s the third largest economy in the euro zone).

The real value of an ECB bond-buying program would probably be more psychological than what can be measured in terms of bond yields. Draghi said he was willing to do “whatever it takes” back in July 2012. Now it’s time for him to act.