Oil prices have surged since dipping to the mid-$40s last month, with internationally traded Brent at $58 a barrel in Europe today. Many see this as evidence that the price plunge is over, and that OPEC has prevailed.

Oil prices have surged since dipping to the mid-$40s last month, with internationally traded Brent at $58 a barrel in Europe today. Many see this as evidence that the price plunge is over, and that OPEC has prevailed.

Not so fast, say two major investment banks. Prices have not bottomed, they say, and OPEC remains far less relevant than it has been.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

In notes to clients, Citi and Barclays both forecast a renewed plummet. Citi’s Ed Morse says the price of Brent could fall below $40 a barrel, and even to $20. Barclays’ Kevin Norrish doesn’t go that far, but says the price will average $40 to $50 a barrel for the year as a whole.

The reason for the two forecasts is mainly supply: We have plentiful and frequent reports of drillers switching off their rigs, which are now operating at their lowest level in the US shale patch since 2011, according to Baker Hughes $BKR, which tracks this metric. But it turns out that data point is largely noise—US shale drillers are continuing to produce in their sweet spots, and may level off only late in the year and on into 2016.

Even then, shale drilling, which is as close to inventory-on-demand as oil ever comes, will come right back when the price goes up, thus locking in a lower price band. Morse calls it a “W-shaped” price trajectory, going down, then up, down, then up, and so on.

In a report released today, the International Energy Agency says, “Despite expectations of tightening [oil] balances by end-2015, downward market pressures may not have run their course just yet.”

For the year as a whole, the US may turn out a 800,000-barrel-a-day production increase, according to the consensus. That almost equals the 900,000-barrel-a-day increase in global demand for the year. Hence, we will more or less end 2015 where it began—with an enormous supply overhang.

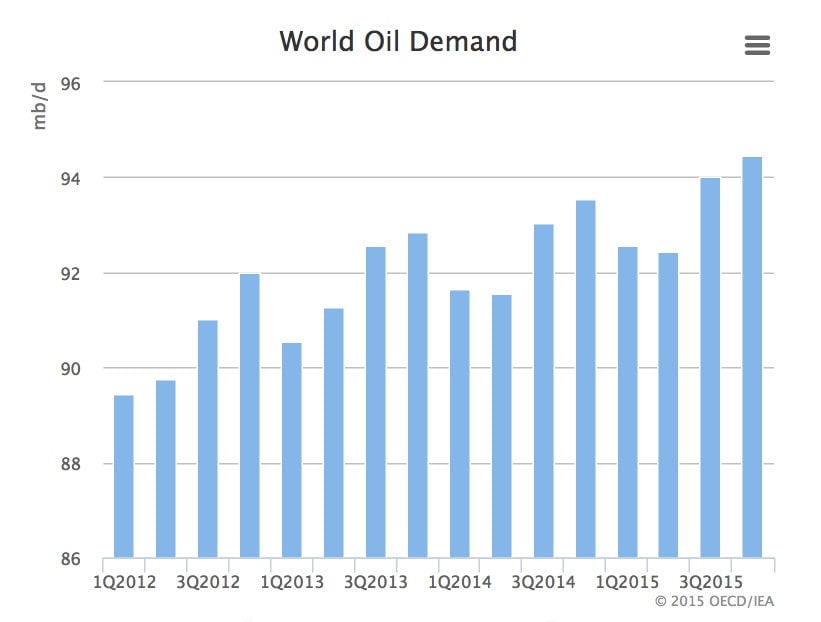

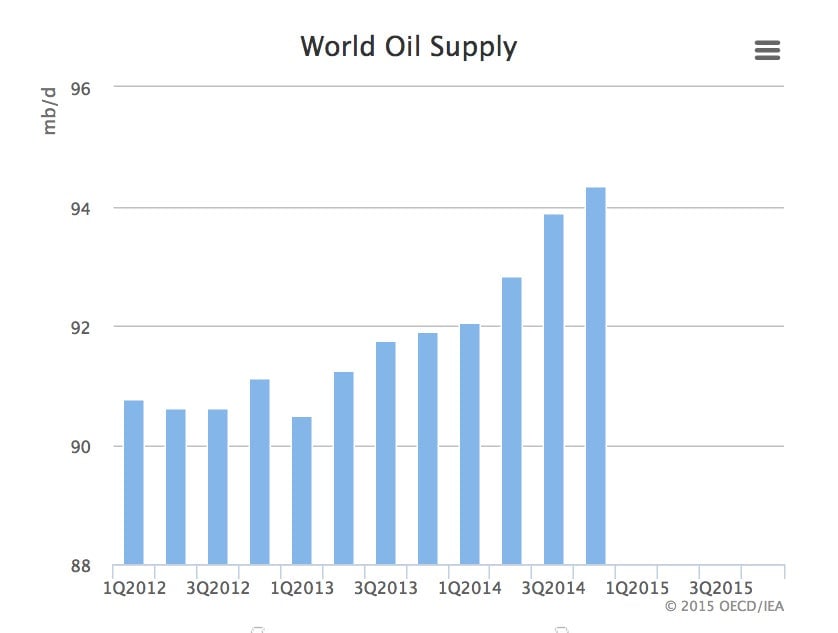

And the production surge is not only in the United States. Take a look at these two charts, from the IEA’s report today.

Drillers elsewhere in the world are expanding their production. Forecasts for China, Canada, Iraq, Russia and Brazil are all higher for the year. And other countries are paying their struggling drillers to keep producing despite lower prices—Argentina and Colombia among them, Barclays notes.

Morse says that OPEC remains in trouble. The reason is that shale production, exceeding the annual increase in demand since 2011, has reduced the cartel’s ability to control prices. The only way the Organization of the Petroleum Exporting Countries can move the needle would be a radical maneuver—shutting down up to 10% of its production over an extended period of time. But even that would risk failure and the loss of market share to its rivals, not to mention that some OPEC members would inevitably cheat and thus steal share from the group’s more honest members.

Saudi Arabia, the cartel’s leader, has been unwilling to assume these risks, and has persuaded the rest of OPEC to go along.

The presumption for OPEC is that it will win—shale will fall aside. But Morse says that is not a fait accompli:

The unconventional supply revolution has created a sort of existential threat to Saudi Arabia and OPEC, which need to find a way to reduce the market share of the new suppliers as well as perhaps some OPEC suppliers in order to maintain the productive life of their oil fields as far into the future as possible.