The lingering low-yield environment has been challenging for sure. Many bond investors, fearful of rising interest rates, have shortened duration¹ to protect principal. Others, with a desire to boost income or maximize return, have lengthened duration in an attempt to capture the higher yields and returns offered further out on the yield curve.

Below we highlight the trade-offs of moving short or long in bond portfolios. While all bond-investing strategies have pros and cons, we believe an approach that diversifies across durations is best for most investors. Most important, despite their lower return expectations, bonds deserve an important role in a portfolio because they are one of the best diversifiers of equity risk.

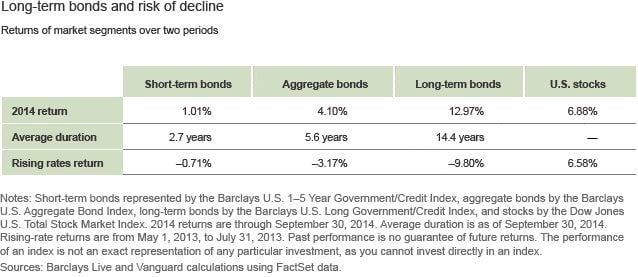

Over the past five years, many investors moved into short-term bonds to reduce interest rate risk. However, short-term bonds underperformed aggregate bonds by almost 200 basis points during the five years ended September 30 (2.23% for the Barclays U.S. 1–5 Year Government/Credit Index versus 4.12% for the Barclays U.S. Aggregate Bond Index), as the feared rising rates didn’t materialize.

Any overweight to short-term bonds has come at a significant opportunity cost to investors, highlighting the difficulty of market-timing.

If rates do spike, bond funds with longer durations may take longer to recover their principal, but historically they have recovered and often do not take much longer than funds with shorter durations to do so.

In the event of a “bear flattening” of the yield curve—i.e., when short-term interest rates rise more than long-term rates—having a shorter duration may also mean greater losses.

With interest rates actually falling in 2014, long-term bonds have been one of the strongest-performing fixed income segments. The Barclays U.S. Long Government/Credit Index returned 12.97% through September 30, far outpacing the 4.10% return of the Barclays U.S. Aggregate Bond Index and the 1.01% gain in the Barclays U.S. 1–5 Year Government/Credit Index.

However, unless long-term bonds are used for a liability-driven approach, they carry significant risks. During the surge in rates in the summer of 2013, long-term bonds fell a steep 9.80%, compared with a 3.17% decline in the Barclays U.S. Aggregate Bond Index and the 0.71% loss for the Barclays U.S. 1–5 Year Government/Credit Index.

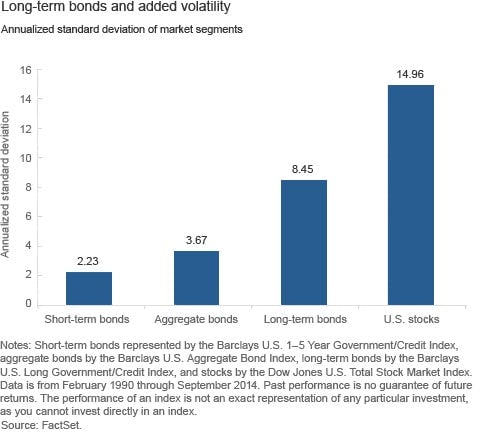

The historical volatility of long-term bonds has been more than twice the volatility of aggregate bonds, and any overweight to long-term bonds may lead to suboptimal outcomes.

Introducing the added volatility that comes with long-term bonds may result in significant losses to a fixed income portfolio when there is an upward shift in yields.

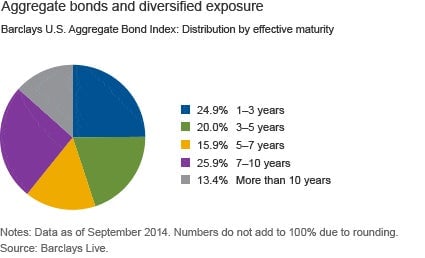

Using the Barclays U.S. Aggregate Bond Index as a strategic benchmark provides exposure to the entire domestic taxable bond market. The broad exposure by effective maturity helps investors to balance the risks of rates rising or falling.

“Rather than shifting drastically one way or abandoning bonds altogether, investors should employ a broadly diversified strategy across duration buckets, which will allow them to potentially benefit if rates rise or fall,” said Ryan Rich, an investment analyst with Vanguard Investment Strategy Group. “No one knows which direction rates will head, or how fast they’ll go, but we do know that bonds can provide diversification in times of equity stress. While not all bonds are alike, a broadly diversified bond fund with intermediate duration can offer that ballast.”

This article was produced by Vanguard and not by the Quartz editorial staff.

_______________________________________________

¹Duration is a rough measure of how much a bond or bond fund’s price is likely to fluctuate against a change in interest rates. The higher the duration number, the more sensitive a bond investment will be to changes in interest rates.

Notes: