by Maria Bruno

A recurring theme jumping out at me from news headlines is that millennials are shying away from the stock market, setting them up for long-term failure as they invest for retirement. For example, just recently, I read about a survey that reported less than 20% of millennials found the stock market to be the best way to save for the future. Frankly, I don’t get it. The numbers don’t support the sentiment!

Looking at both Vanguard and industry data, we see that younger investors are actually embracing stocks. They’re doing so through the use of balanced funds such as target-date funds. So, why the disconnect? Perhaps millennials don’t realize it, but their average equity exposure is very much in line with what it should be for their age and investing stage.

Case in point: Our research shows the average stock allocation of young Vanguard IRA® investors is about 85%.

This trend isn’t exclusive to Vanguard IRA investors. According to the Investment Company Institute, equity holdings in Roth IRAs for younger investors industry-wide is about 82%.¹

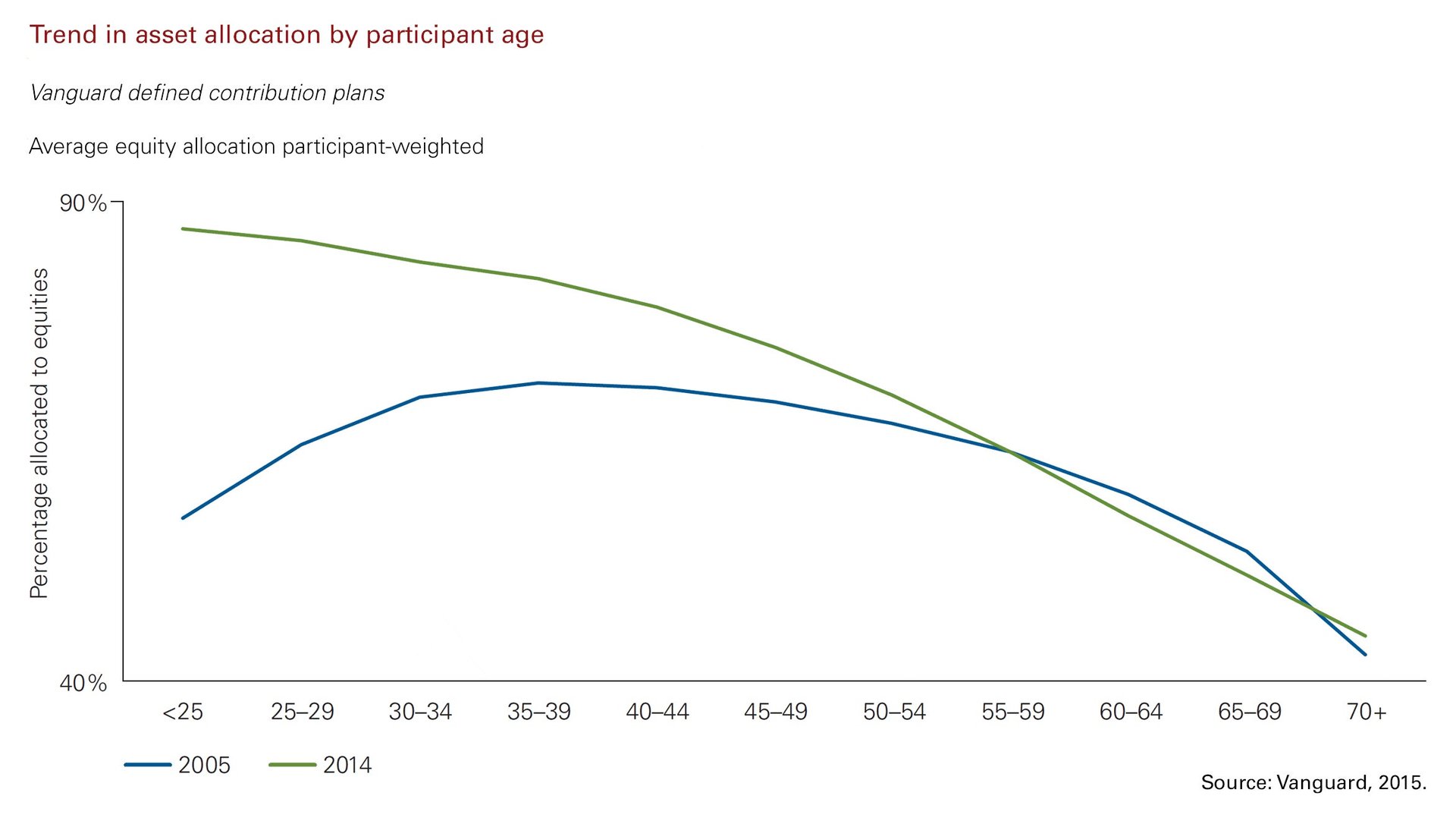

According to our research, millennials also have (appropriately) high equity allocations in their 401(k) plan portfolios. Similar to IRA equity allocations, equity holdings for young investors in their employer-sponsored plans average around 85%.² While in the past we saw younger investors with more conservative 401(k) portfolios, we see more equity exposure today. Improved plan design, such as the use of auto-enrollment and the use of target-date funds as a default investment, are opting investors into balanced portfolios and thus helping them avoid asset allocation mistakes (such as extreme portfolio allocations).

Investing in the stock market can be risky. But, when investing for the long term, avoiding the stock market can be even riskier. There are two opportunity costs as a result of staying on the sidelines. The first is shortfall risk; if the portfolio lacks investments that offer higher return potential, younger investors may not achieve growth sufficient to fund long-term goals. The second is inflation risk; the portfolio may not grow as fast as prices grow, and younger investors will lose purchasing power over the long term.

So while millennials face financial challenges, I don’t see their lack of equity exposure as one of them. In evaluating the asset allocation decisions in their tax-advantaged retirement accounts, the numbers support that younger investors are actually on the right track!

(If you think your investments may not be on the right track, this questionnaire can help you determine what asset allocation may be most appropriate for your situation.)

This article was produced by Vanguard and not by the Quartz editorial staff.

* Roth IRA contributions outpace traditional IRA contributions 2 to 1 for younger investors. Traditional IRA equity holdings among younger investors are lower, ranging from an average of 64% for those 25–29, and 72% for those in their 30s.³

¹Holden, Sarah, and Daniel Schrass. 2015. “The IRA Investor Profile: Roth IRA Investors’ Activity, 2007–2013.” ICI Research Report (July). Available at http://www.ici.org/pdf/rpt_15_ira_roth_investors.pdf

² Young, Jean A. and Stephen P. Utkus, 2015. “How America Saves 2015.” Valley Forge, Pa., Vanguard.

³ Holden, Sarah, and Steven Bass. 2015. “The IRA Investor Profile: Traditional IRA Investors’ Activity 2007–2013.” ICI Research Report (July). Available at http://www.ici.org/pdf/rpt_15_ira_traditional.pdf

Maria Bruno

Maria is a senior retirement strategist in Vanguard Investment Strategy Group. She leads a global team that’s responsible for conducting research and providing thought leadership on the topics of retirement, wealth, portfolio construction, and financial planning for individual investors. Maria specializes in retirement planning, retirement income solutions, and wealth management strategies. Prior to her current role, Maria worked in our financial planning and advice departments. Maria earned a bachelor of science in business administration (B.S.B.A.) from Villanova University and is a Certified Financial Planner™ professional.