Since the financial crisis hit in 2008, the Fed has often been attuned to a specific metric as it seeks to prevent the US economy from slipping into a catastrophic deflationary vortex.

Since the financial crisis hit in 2008, the Fed has often been attuned to a specific metric as it seeks to prevent the US economy from slipping into a catastrophic deflationary vortex.

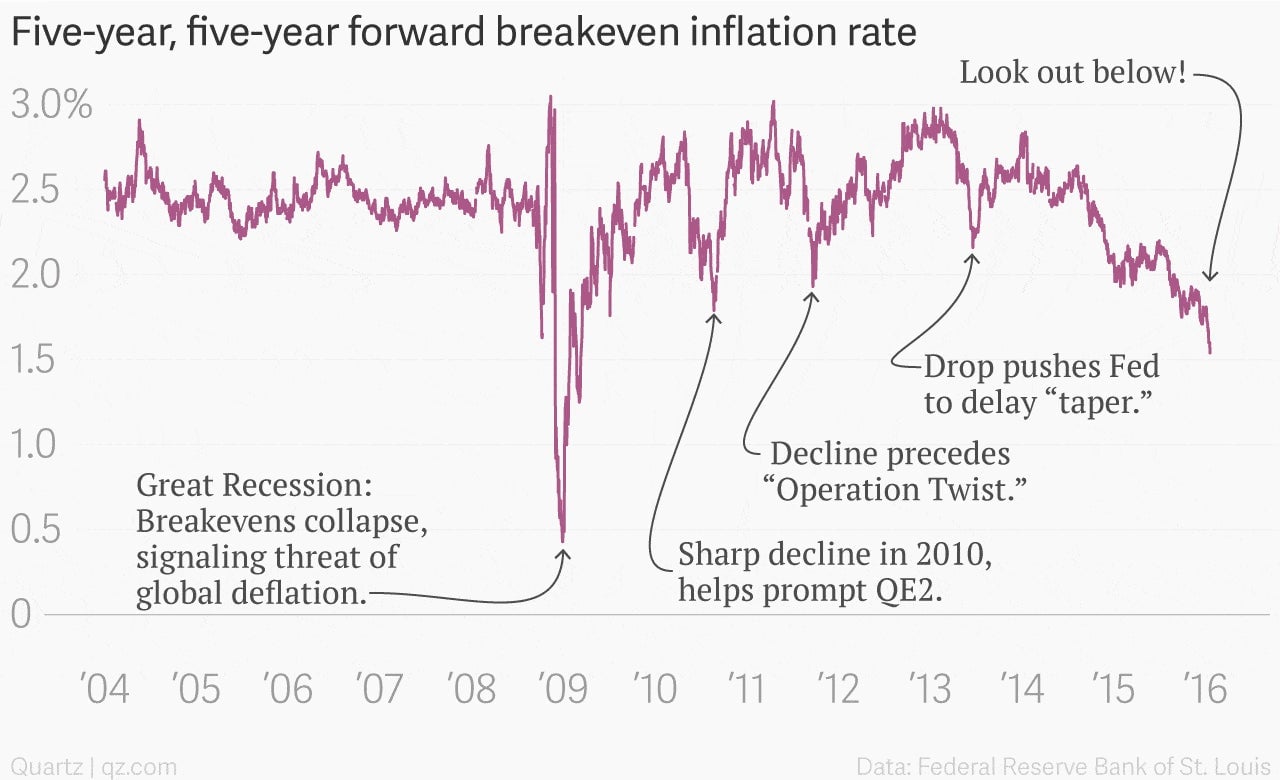

It’s called the five-year, five-year forward inflation break-even rate. Basically, this attempts to measure what cyborg investors living five years in the future (2020) think inflation will be five years even further into the future (2025). This gauge is cobbled together using existing market instruments such as Treasury Inflation-Protected Securities (TIPS) and other US Treasury bonds.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Obviously, this is a bit of financial fiction. No one knows what future investors—cybernetic or not—will think about their future outlook for inflation five years out.

But while it’s obviously only a market-based approximation, the Fed has has been very responsive to this number in the years after the Great Recession. In 2010, it announced a second round of quantitative easing—QE2—after breakevens plunged. In 2011, another decline was followed by a Fed program known as “Operation Twist.” In 2013, a precipitous drop seemed to help convince the Fed to push-off the “taper” it had hinted was imminent.

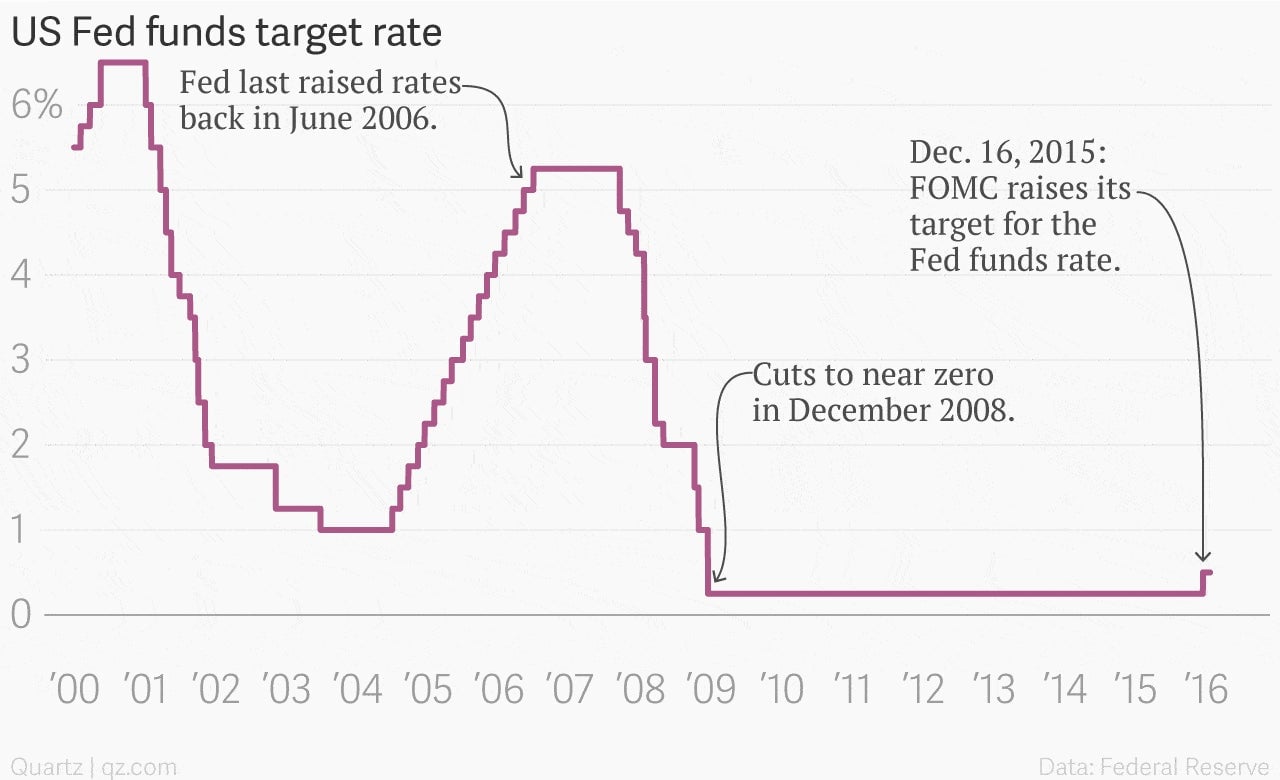

More recently, though, the Fed has seemed content to let the five-year, five-year fall, with officials—including Fed chair Janet Yellen herself—pooh-poohing the importance of market-based measures of inflation expectations, which remained spookily low even as the Fed moved toward raising interest rates for the first time in nearly a decade.

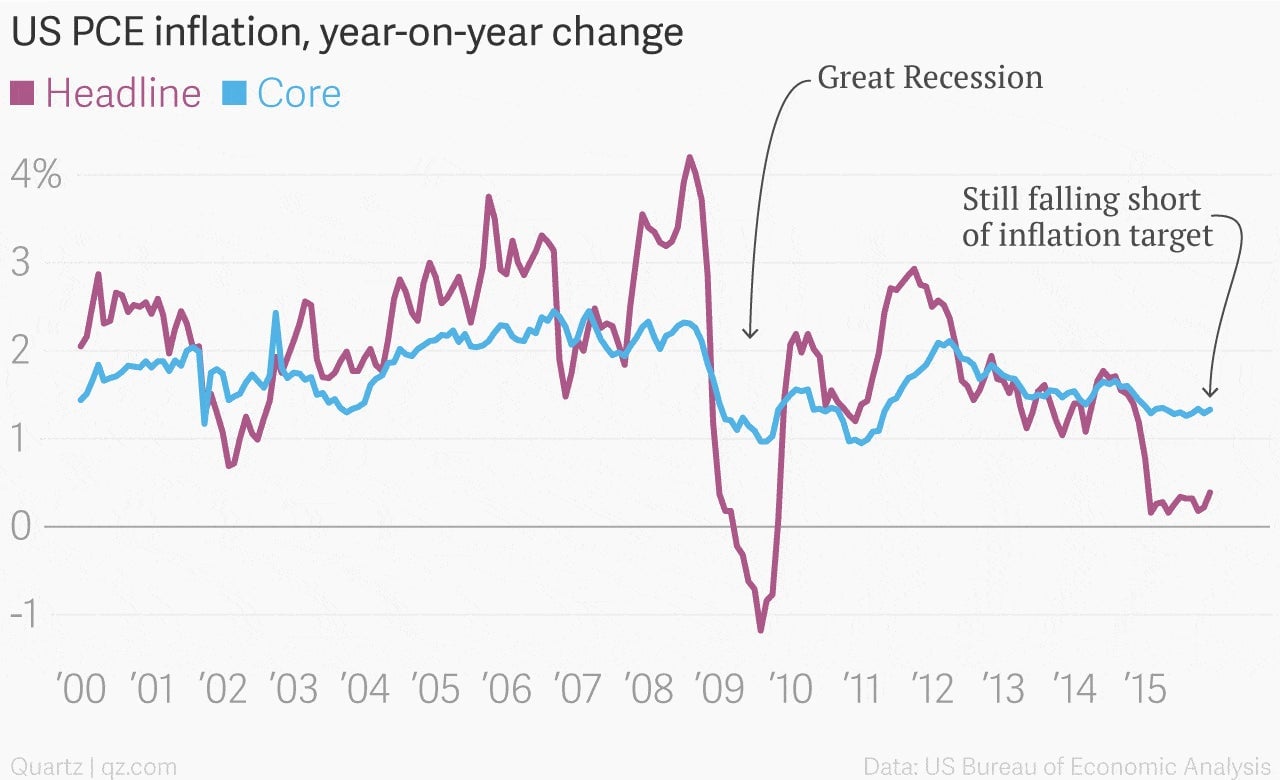

This seemed, and seems, like a really risky approach. It’d be one thing if the breakeven rate was telling a wildly different story from the rest of the inflation data. But it’s not. Oil prices have been in outright collapse. China’s economy—the world’s second largest—appears to be rapidly coming off the rails, and as a result is exporting deflation around the world. The euro zone continues to grapple with very, very low inflation. Japan remains Japan. And US inflation remains quite low, and well below the Fed’s own 2% target.

The Fed should consider whether it was wrong and may have allowed dangerous expectations for deflation to become entrenched among market participants.

Against a market backdrop like this, humility seems like the best policy option.