The euro crisis has widened the gap between rich and poor countries in Europe, and one reason is the borrowing costs for small businesses. For years, these lending rates moved in lockstep across the euro area. Since the crisis, they’ve been diverging. More worrying still, the divergence is now wider than it was last July, when European Central Bank (ECB) president Mario Draghi vowed to do “whatever it takes to save the euro.”

The euro crisis has widened the gap between rich and poor countries in Europe, and one reason is the borrowing costs for small businesses. For years, these lending rates moved in lockstep across the euro area. Since the crisis, they’ve been diverging. More worrying still, the divergence is now wider than it was last July, when European Central Bank (ECB) president Mario Draghi vowed to do “whatever it takes to save the euro.”

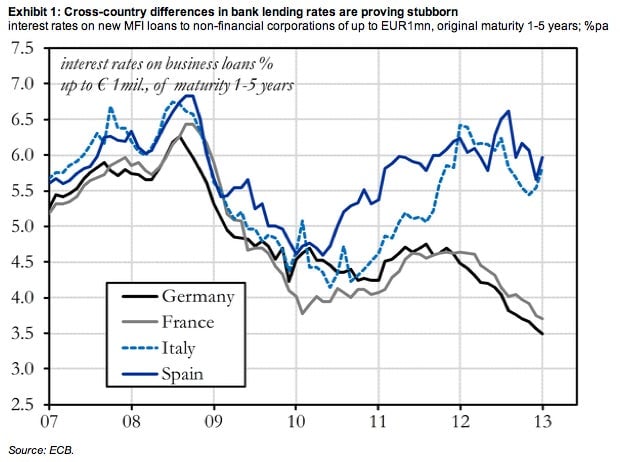

Here’s a look at the latest ECB data on business loans of less than €1 million (pdf), via Italian financial journalist Fabrizio Goria and Goldman Sachs $GS.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

As you would expect, lending rates are highest in stricken Italy and Spain. This, of course, means it’s harder for small businesses in Italy and Spain to create jobs. It would be nice to have more jobs. Italy’s unemployment has hit 11.7%, while Spain’s is now at a mind-bending 26.0%.

But you might also notice something odd in the above chart: France. Its economy is plainly lousy. So why are its rates skewing German?

The answer seems to be a larger optimism toward French sovereign debt. Evaluating the just-splendid results of a recent French bond sale, the Wall Street Journal puts this cock-eyed view down to distraction from the south. As “investors fret over risks elsewhere in the euro zone, they are willing to ignore France’s deepening economic problems,” the WSJ wrote earlier this week (paywall). France is also in a kind of Goldilocks zone: Its bonds aren’t so risky as to scare off investors afraid of the periphery countries, but not so safe as Germany’s bonds, whose next-to-nothing yields can be rather off-putting. As a result, France enjoys cheap borrowing costs—and concerns abound that President François Hollande is failing to capitalize on these to revive his economy.

However, the chart also tells us one other important thing: the private sector is reaping much more benefit from the ECB’s loose monetary policy in Germany than in its southern neighbors.

Draghi recognizes this problem. “The large companies, by and large, had no problem in funding themselves,” he said in the ECB’s interest-rate announcement earlier today. “The SMEs do,” he added. But still the ECB declined to cut rates today.

Should it have? Not necessarily. If anything, the chart above shows just how impervious Italy’s and Spain’s high lending rates can be to broader euro-zone easing. Even so, easing would have the knock-on effect of weakening the euro, which would make small exporters more competitive. And rates that ease things in Germany and France, and to big businesses, should eventually trickle down to small businesses in the south. At least in theory.

Draghi remained unmoved, though. ”The ECB is not in the business of cleaning up banks’ balance sheets,” he said, referring to the ailing Spanish and Italian banks that contributes to their country’s poor credit conditions. ”The ball is in the governments’ court [to pass economic reforms].”