It’s true. The February jobs report was good. More jobs (242,000) were created than were expected (195,000).

It’s true. The February jobs report was good. More jobs (242,000) were created than were expected (195,000).

The unemployment rate remained at 4.9%, its second straight month below the 5% level that many see as “full employment” or the point at which the Fed should start raising interest rates in order to head off an inflationary spiral.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Many are wrong.

How do we know? Precisely because the unemployment remained stable, despite the creation of more than 242,000 new positions. In other words, the supply of the labor market is rising. People are coming back to work.

It’s hard to overstate what good news this is. The Great Recession left deep scars in the US job market. The downturn—combined with baby-boom generation moving to retirement—sent US labor force participation tumbling from 66% in October 2008 to 62.4% in September 2015.

But since September 2015, more than two million people have come into the labor force as the peppiness of the US labor job market has started to pull them back. The results are an incipient sign that the years-long trend could be starting to reverse.

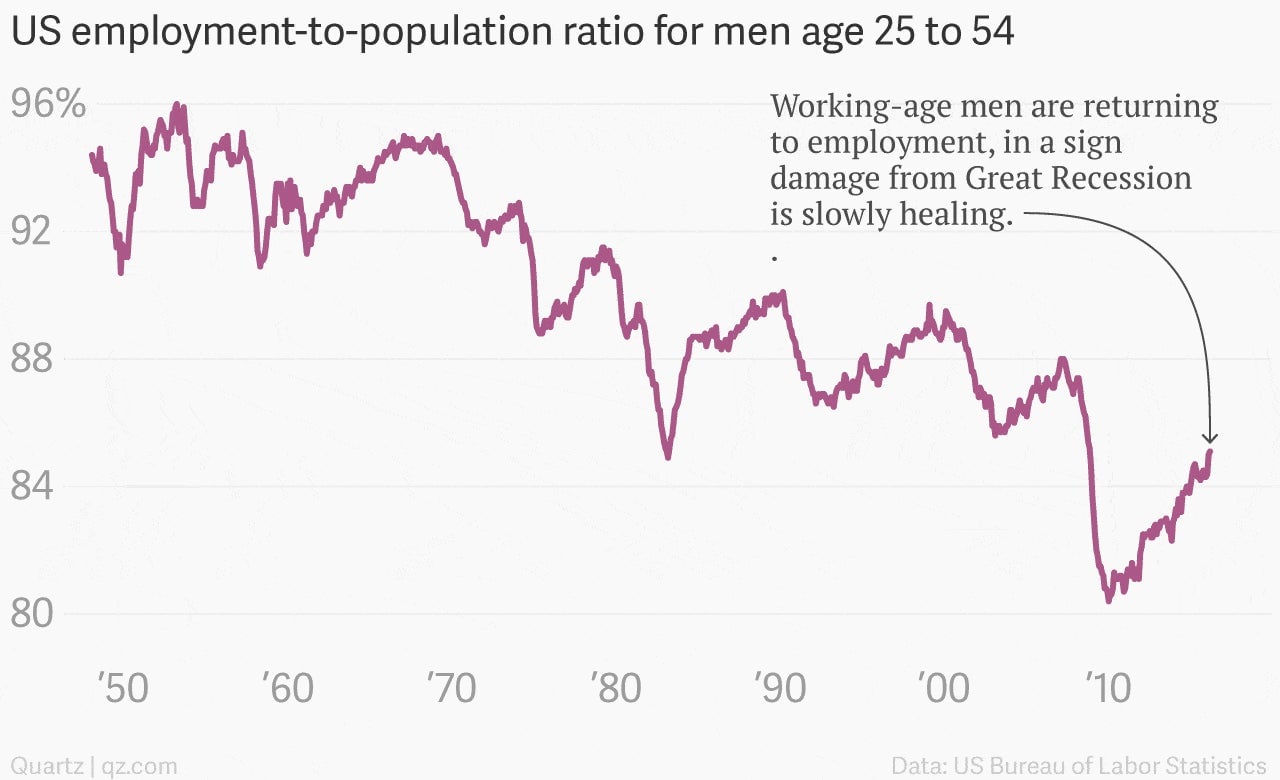

Another gauge of participation is the employment-to-population ratio, which has been showing marked improvement as well. And in a bit of especially good news, the share of men in their prime working years who are employed—which collapsed as the Great Recession hammered heavily male industries such as home construction—has been on a long, slow climb that has gathered apace in recent months. It’s probably due in part to unseasonably warm weather that’s helped support construction employment.

All the same, the improvement is real. And it’s almost exclusively due to some combination of the Federal Reserve’s efforts to support economic growth with the healing power of time. (Fiscal stimulus such as tax breaks or spending plans have been largely MIA from the recovery since President Obama signed the American Recovery and Reinvestment Act into law in early 2009.)

The improvement in labor force participation is also fragile and reversible. The Fed must nurture it by being extremely cautious in its approach to raising interest rates. There’s no need for the Fed to continue a pre-set path of interest rate hikes many had expected when it raised rates for the first time in nearly a decade in December 2015.

Core inflation, while picking up a bit, remains below the Fed’s target. And wage growth—conventionally viewed as some kind of early warning system of inflation—is still piddling by the standards of past economic recoveries. (Average hourly earnings rose 2.2% over the past 12 months.)

In other words, there is substantial slack in the labor market—people who can be drawn back to work as it gets easier to get a job. And that means the Fed can bide its time instead of rushing to raise rates further and risking undoing some of its substantial—but not sufficient—accomplishments.