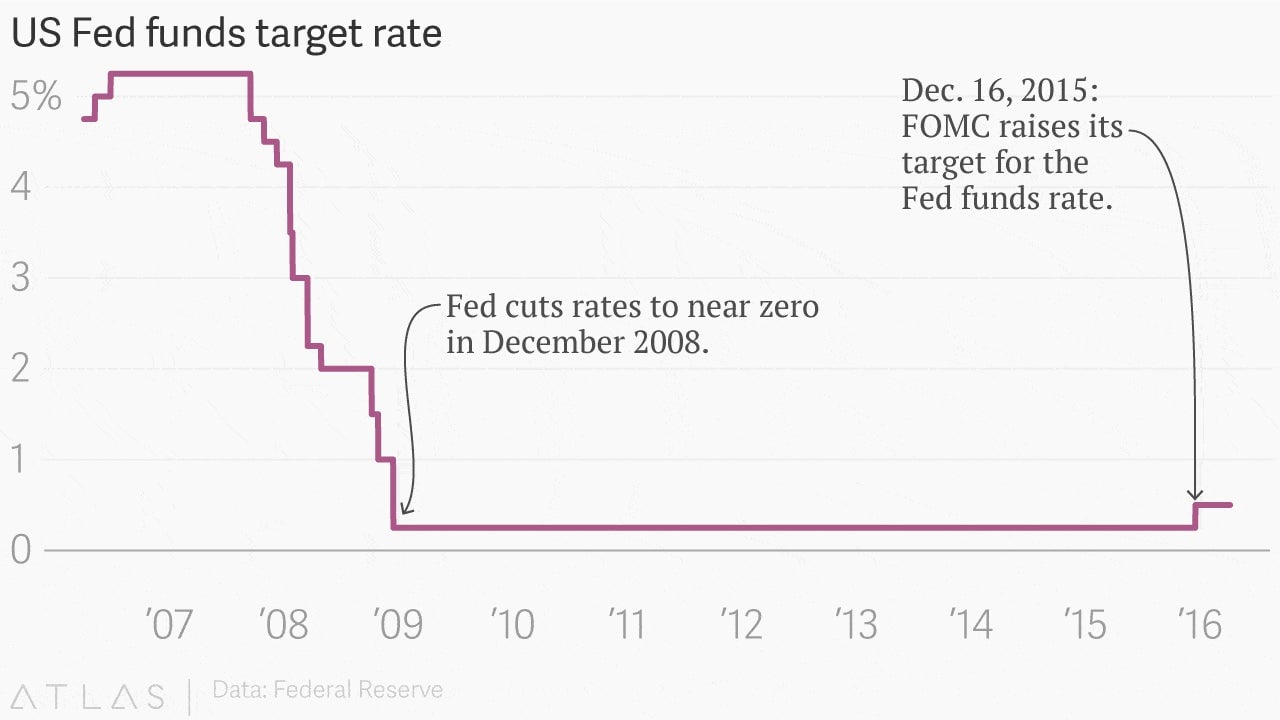

Once upon a time, the Fed expected to raise its benchmark interest rate, the Fed funds rate, to 1% by the end of 2016.

No longer. The US central bank now expects that it will only raise it by 0.50 percentage points this year.

So why did the Fed change its mind? Well, luckily, the US central bank pretty much told us why, in its just-released minutes from its most recent meeting that concluded on March 16. The minutes suggest that a rate hike also is less likely at the Fed’s meeting later this month, unless economic data picks up sharply and convincingly. Here’s why.

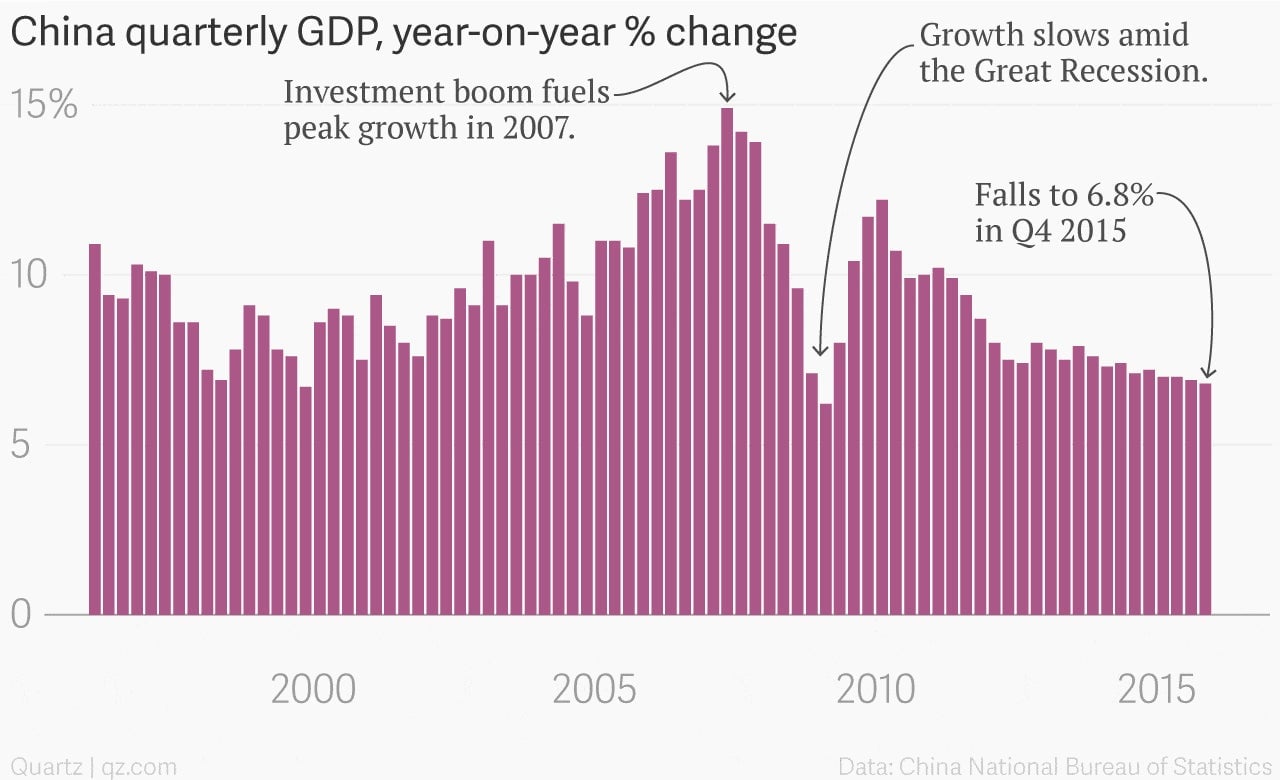

China is slowing. Brazil is a basket case. Russia is in recession. Europe is still puttering along in first gear. Japan is Japan. Weak global growth suggests that the world economy will act as a headwind on the US, if that’s the case raising rates too aggressively would be the wrong move.

Inflation continues to run below the Fed’s stated 2% annual goal, and it expects it will be below that goal even as far as 2018. True, there’s been a very slight uptick recently. Still Fed minutes state “The risks to the projection for inflation were still seen as weighted to the downside, reflecting the possibility that longer term inflation expectations may have edged down, and that the foreign exchange value of the dollar could rise substantially, which would put additional downward pressure on inflation.”

The Fed also noted the that it has more weaponry to fight inflation—should there be any sign of it—than it does to boost growth if the US economy starts to stall. That’s because interest rates are already near zero, meaning cutting them to zero or even following some central banks and pushing them into negative territory, likely won’t do a heck of a lot to provide the US economy a helping hand.

Fed officials have taken note of this asymmetry of risks. “In their view, this asymmetry made it prudent to wait for additional information regarding the underlying strength of economic activity and prospects for inflation before taking another step to reduce policy accommodation,” the minutes stated.

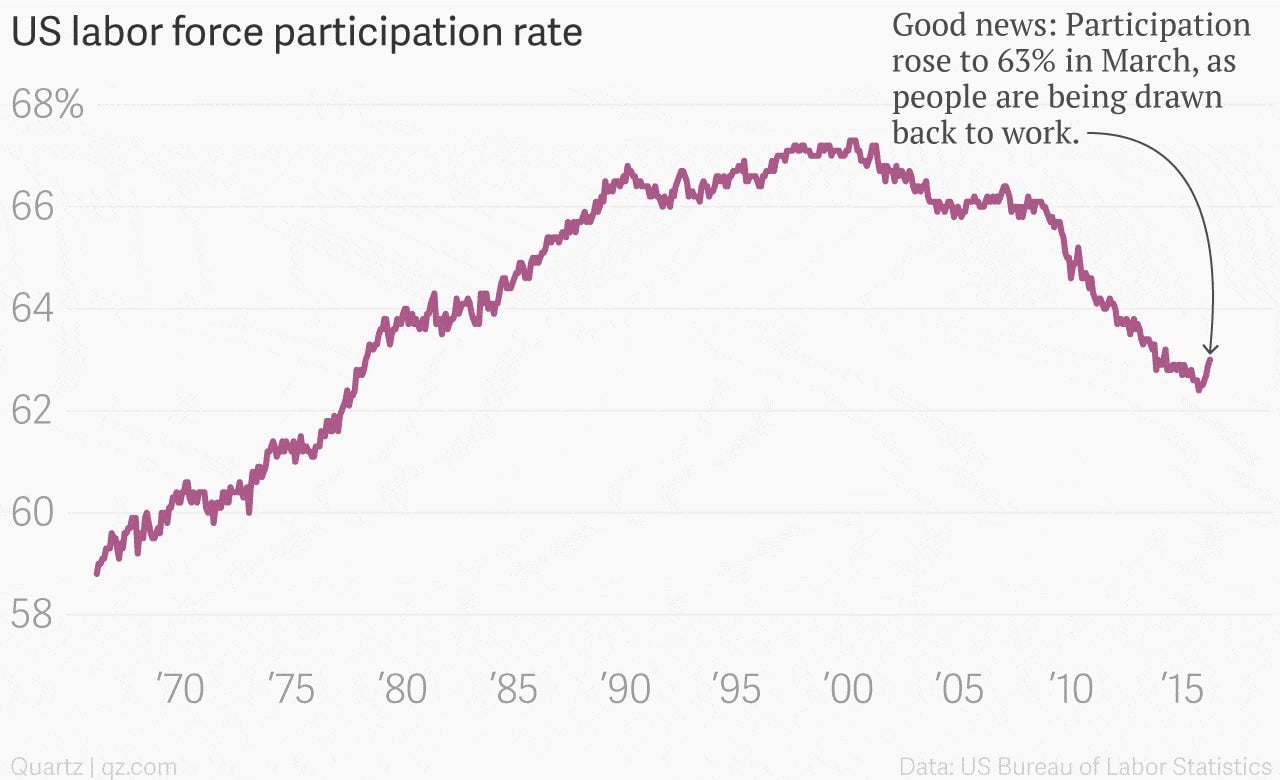

What’s more, there’s little sign that wage growth, traditionally viewed as a precursor to inflation, is picking up sharply. That’s because the US labor market is attracting people back into the workforce. That’s not only a very good thing for the economy, it suggests there’s relatively low risk of the Fed setting off an inflationary spiral by keeping money too easy, for too long.