First, there’s the need for the central banks of developing countries to diversify their holdings. When a country runs a trade surplus, meaning that it sells more goods and services abroad than it buys from other countries, demand for its currency rises to pay for its goods. As part of this, central banks wind up with foreign currencies—mostly dollars or euros—in their accounts. Many developing countries are net exporters, which has helped steadily increase their central banks’ foreign reserves.

But as quantitative easing and economic uncertainty have effectively caused many reserve currencies such as the dollar and pound to depreciate, central banks with large stashes of such foreign currencies have felt increasing pressure to invest instead in other assets as a way of preserving the value of their reserves. Gold is in the category of things they can buy that are considered safe havens amid economic turbulence.

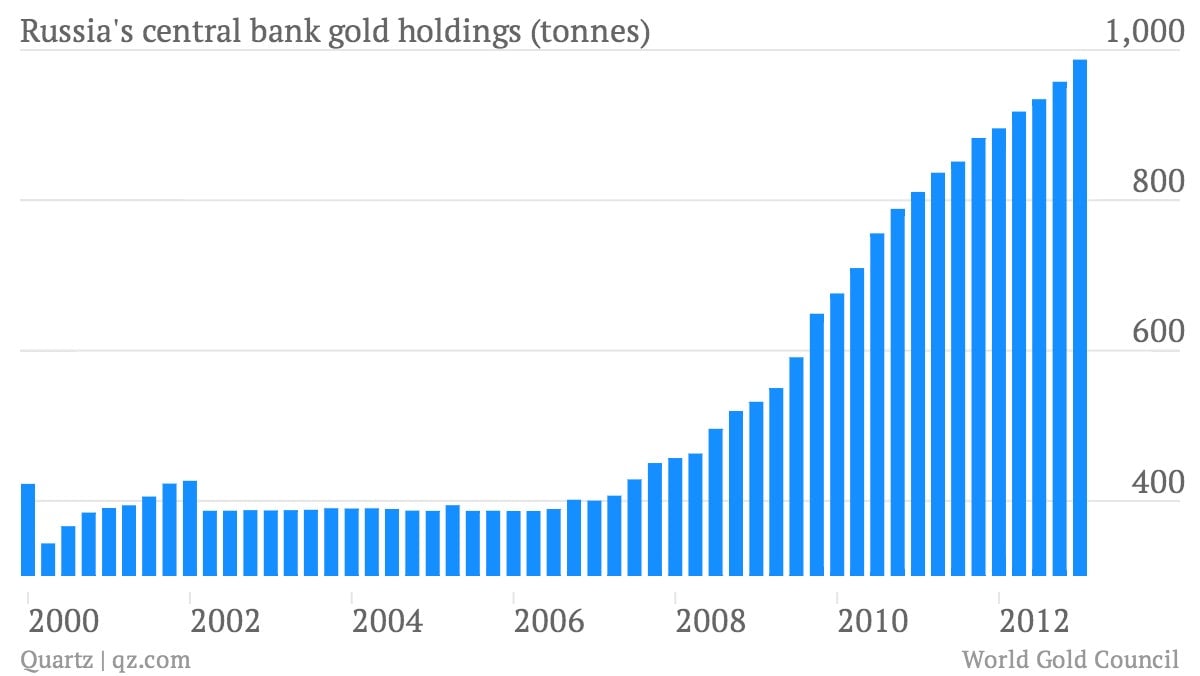

For example, Russia has bought up 570 tonnes of gold in the last decade as a bet against any “cataclysm” in the dollar, euro or pound. In 2012 alone it amassed around 75 tonnes, makings its reserves the eighth-largest in the world; so far in 2013, it has added nearly 20 tonnes.

Other examples include export-centric countries like South Korea and Thailand, which have both been snapping up gold in the last few years. (Tellingly, China’s gold purchases have plateaued with its foreign exchange holdings.) Meanwhile, a big jump in the holdings of Mexico’s central bank likely came its 2010 currency interventions to keep the peso weak, which resulted in ballooning reserves. Here’s a look at the net central bank holdings in tonnes for those countries:

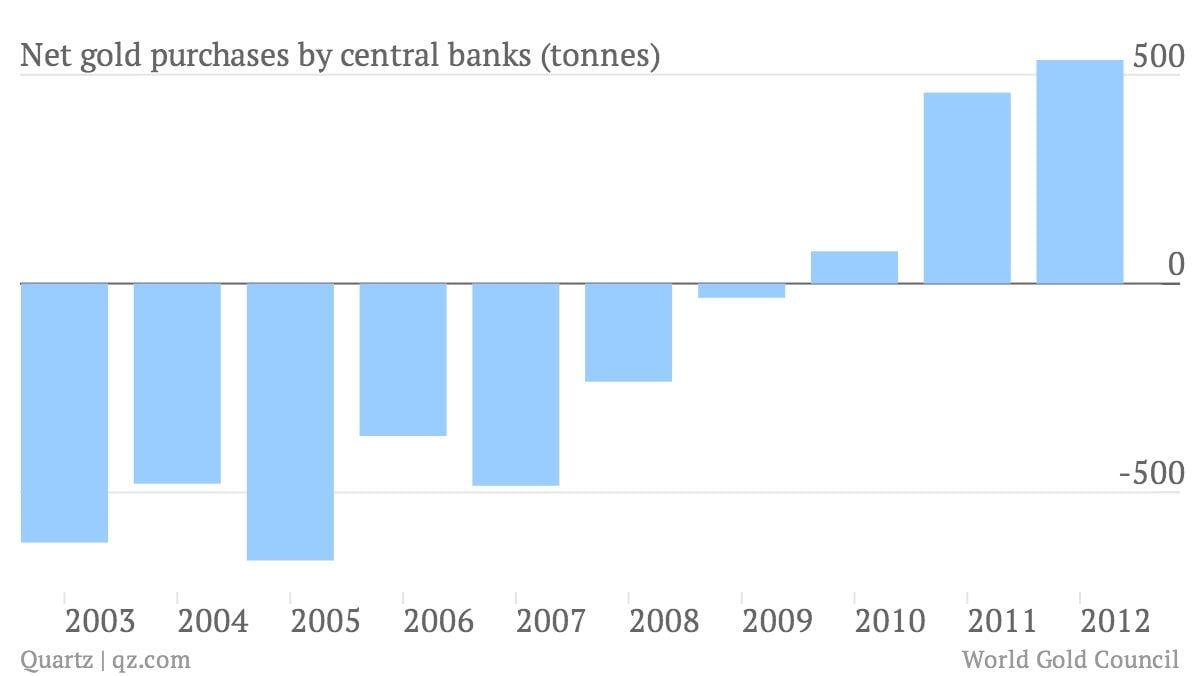

But remember the WGC data reflect net purchases. Developing countries are mostly playing catch-up with the central banks of more advanced economies, which used to be net sellers of gold. Here’s a list of the top central bank holders of gold:

Joseph Gagnon, economist at the Peterson Institute for International Economics, explains that the large holdings—in terms of both volume and share of reserves—among the developed economies are largely due to historical legacy. ”Most of these gold stocks are just holdovers from many decades ago when gold mattered,” Gagnon tells Quartz, noting that “there is no need to hold gold.”

Many had been trying to get rid of these holdovers—in fact, the selloff among central banks in Europe was consistent enough that it eventually necessitated a 1999 agreement on the limit to what they could unload each year. And even that didn’t stop some European central banks. For instance, Spain has sold off a whopping 46% of what it held in gold in 2000. Portugal and the Netherlands also parted with 37% and 33%, respectively.

But all that stopped abruptly in 2009, around the time when diversifying foreign reserves became more important. And with the gold market now crashing, that may seem like an extremely unfortunate call. However, as Gagnon points out, the values of central bank reserves aren’t all that important for advanced economies that still have a high proportion of their assets in gold. “Falling gold prices will have no effect on almost all of these countries,” says Gagnon.