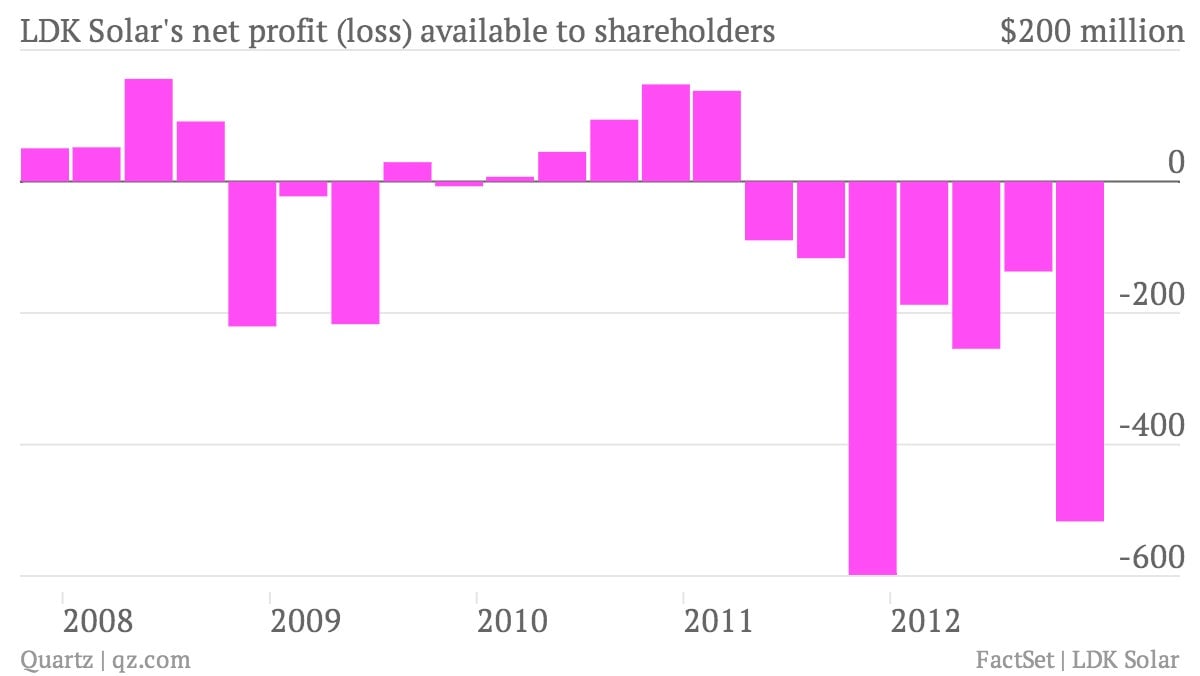

Chinese renewable energy giant LDK Solar reported its fourth-quarter earnings today, and by any measure the news was grim. Falling revenues, a $409 million operating loss, a negative 301% operating margin, and more than $2 billion in debt. As of this morning, LDK has a market cap of $137 million.

Chinese renewable energy giant LDK Solar reported its fourth-quarter earnings today, and by any measure the news was grim. Falling revenues, a $409 million operating loss, a negative 301% operating margin, and more than $2 billion in debt. As of this morning, LDK has a market cap of $137 million.

But wait, it gets worse. LDK, which on April 16 partially defaulted on $24 million in bonds, faces a $295 million payment to China Development Bank on June 3 unless it spins off a subsidiary that makes polysilicon, the chief ingredient of solar cells. Given that polysilicon prices fell 50% in 2012 and the Chinese solar panel industry is burdened by overcapacity, such a sale appears unlikely. (The company makes just about everything in the photovoltaic panel supply chain—from polysilicon to silicon wafers to solar cells. It also develops solar power plants.)

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

LDK, it seems, could be the next Chinese solar company to fail. After all, China’s banks last month forced the Chinese operations of Suntech into bankruptcy after the company defaulted on $541 million in convertible notes. Until 2012 Suntech ranked as the world’s biggest solar panel maker. (More here on the Suntech saga.)

But on a conference call with analysts this morning, LDK executives sounded confident that LDK is too big to fail. “We are working very closely with the government, the banks and our vendors,” LDK chief financial officer Jack Lai said. “We’ve reached some agreement with China’s banks that loans will stay in place and lines of credit will be renewed and we’ll continue to have support from China-based banks.”

Lai said LDK has also secured a 2 billion yuan ($321 million) line of credit. “We’re confident we’ll be able raise sufficient funds to meet our obligations,” said Lai.

LDK will need all the help it can get. The company’s liabilities total $4.5 billion and fourth-quarter net revenues were a paltry $136 million. But even that looks good compared to Lai’s projections for the first quarter of this year, when it expects revenues of $80 million to $100 million.

Absent a government bailout it’s unclear how LDK extracts itself from this mess. Lai said some of its creditors may be amenable to converting accounts payable to equity. But given that LDK’s American depository shares were trading at $1.08 today, creditors may not find that very enticing.

The company has already fired nearly half its workforce and is unlikely to bring in much cash from asset sales. Case in point: Today LDK disclosed in a financial filing that the sale of a subsidiary to the Hefei City government resulted in a net loss of $80 to $90 million.