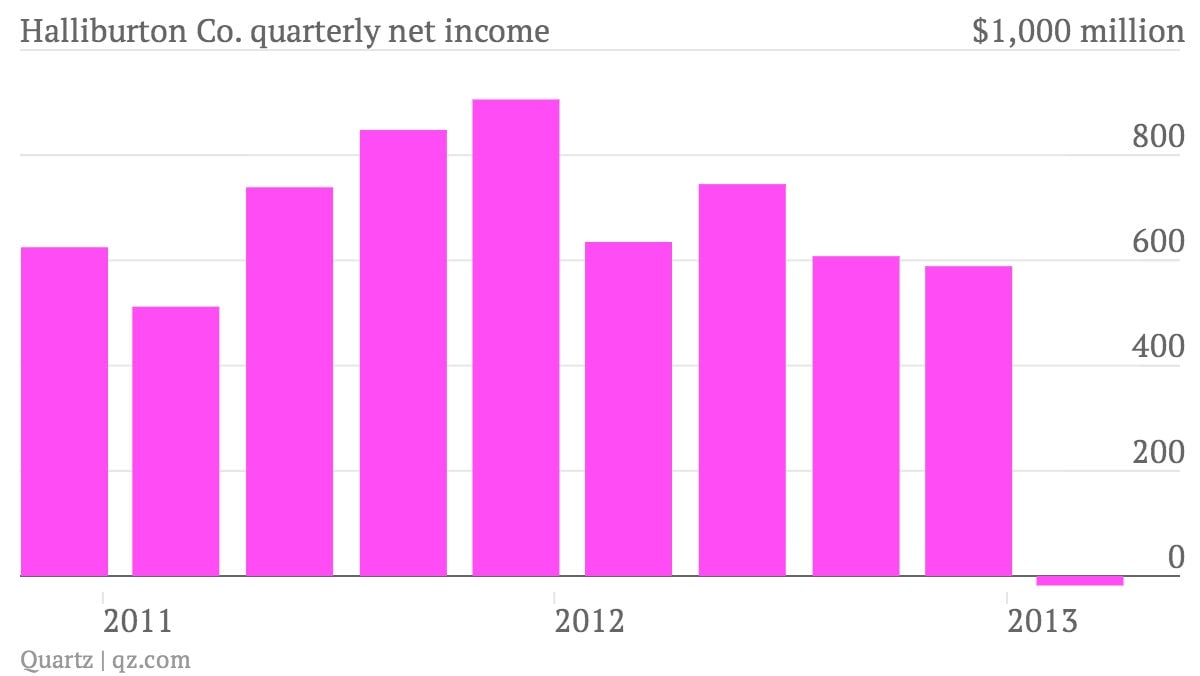

Halliburton takes a punch from Gulf settlement, and then pumps out impressive numbers

The numbers: The world’s second largest oil field services firm reported a net loss of $18 million (pdf) on the heels of $637 million in litigation charges from the 2010 Gulf of Mexico oil spill. But discounting money set aside for the oil spill and losses incurred from closed operations, Halliburton’s quarterly profit ballooned to $0.67 per share, significantly higher than analyst expectations of $0.57 per share. Strong sales, which climbed 1.5% from last quarter to $6.97 billion, coupled with successful cost-cutting helped the company’s operating profit margin reach 16%.