How an obscure middleman system plays a key role in keeping US drug prices sky-high

Pharmaceutical giant AbbVie was able to delay competition to its blockbuster arthritis drug, Humira, into the US market for many years. But Americans can finally choose from one of several arthritis biosimilars, as generics for complex molecule drugs are known.

Although biosimilars will sell at a list price lower than Humira, there is no guarantee that patients will actually be offered as much access to cheaper biosimilars as they are to the name-brand product.

The first biosimilar to enter the market is Amgen $AMGN’s Amjevita, which was launched in the US on Jan. 31, 2023. The drug will be available in the US at two different list prices, $3,288 and $1,557 for a two-week supply, respectively 5% and 55% less than the Humira list price.

It’s not different quantities, not different means of administration, not even different packaging. It’s the same product, sold at two prices, one more than double the other. Understanding why that is sheds some light into the workings of a secretive actor that profits from the complexity of American drug pricing: Pharmaceutical Benefit Managers (PBMs).

It’s not easy to explain how PBMs work, because their role is not designed to be understood. They are a unique feature of the healthcare industry in the US. They are arguably as responsible as the pharmaceutical industry for the sky-high prices that Americans pay for drugs compared to the rest of the world. They are also uniquely obscure. A 2017 survey by the National Pharmaceutical Council found that just under a third of companies employing the services of a PBM actually understood how they work. Because of this, they get away with their role in price hiking without big pharma’s infamous reputation.

Although the name may suggest otherwise, PBMs are not one person, or even a department within a company. They are whole companies—huge ones, in fact. The biggest, CVS Caremark (34% market share), reported nearly $170 billion in revenue for 2022, or about 60% of the overall revenue of CVS, which includes health plans, pharmacies, and other services. Express Scripts (24% PBM market share) and OptumRx (which is part of United Health Group, and accounts for 21% of the market) both have revenue of around $100 billion a year. Karen Lynch, CVS CEO, made more than $20 million in 2021; Andrew Witty, UnitedHealth $UNH Group CEO, got $16.8 million in compensation in 2021 (Heather Cianfrocco is OptumRx’s CEO, but her salary information aren’t public); Express Scripts’ CEO George Paz was paid $13.8 million in 2021.

By way of comparison, in 2020, before covid vaccines added billions to big pharma’s bottom lines, the pharmaceutical company with the most revenue—Johnson & Johnson $JNJ—grossed $82 billion.

The need for PBMs stems from the structure of America’s health system. Submitting and processing insurance claims, negotiating drug prices, establishing reimbursement rates with pharmacies: These are all administrative layers that add onto the cost, and the bureaucracy, of privatized healthcare. In most other countries, government bodies negotiate the price of drugs and their reimbursement rates, so there is limited need for this type of intermediary.

On paper PBMs make perfect sense. Insurance companies use them to outsource the burden of negotiating with drug companies, and processing drug claims, trusting that their expertise will get the best deal and in so doing, pass down the savings to both the companies and subscribers. Except, these savings don’t really trickle down—at least not all, and not always.

PBMs list the drugs they have negotiated in what is known as a formulary, or a tiered list of medications. The least expensive drugs are on lower tiers, typically generics. These have low or no copays. As tiers go up, so do copays. However, that isn’t necessarily proportional to the actual price of a drug. For instance, a medication might be on the top tier simply because there is a generic available for it, and a much more expensive drug without a generic (or biosimilar) substitute could be on the second tier. Typically, a formulary will be structured in three or four tiers, with the top one reserved for drugs that patients have to pay for out-of-pocket.

PBMs are paid by health insurance companies through administrative fees, but often a portion of those fees is proportional to the savings they bring to an insurance plan through negotiation. The higher the discounts, the more valuable PBMs are, and the more they are paid. It seems logical enough, yet this is where the first issue lies: Though a PBM’s goal should be to lower the cost to their client, this isn’t necessarily the best way to get a high discount from a drug company.

In fact, the higher a drug’s price is before the negotiation, the more the negotiation will appear effective—even if the price was already determined by keeping into account a future discount. “It’s a little like raising the price of a jacket before you put the jacket on sale,” says Robin Feldman, a professor of law at University of California Hastings and the author of Drugs, Money, & Secret Handshakes, a book on the role of PBMs in drug pricing. “Looks like a great deal, but it’s not.”

What adds complexity, and warped incentives, is the way the discounts given to PBMs work. For the most part the discounts happen in the form of rebates. “The [insurance] company never knows the actual price paid for that particular medicine purchase. The rebates come in well after that the patient has purchased the drug,” says Feldman. Rebates are given after patients of the insurance plan buy large volumes of a certain medicine, and PBMs are allowed to pocket a portion of those rebates. They are then supposed to pass on the rest of the savings to the insurance companies and their subscribers, but there is no way to know for sure what the share is.

PBMs and pharmaceutical companies claim that their agreements are trade secrets, although price and price terms should not be, as Feldman and her colleague Charles Tait Graves argue in the Yale Journal of Law and Technology. “The deals for calculating the rebates are deeply hidden secrets. The health plan, their auditors, and even the government don’t get full access to the contracts,” says Feldman. Only pharmaceutical companies and PBMs know the full details pricing agreements, and even the insurance companies that pay the PBMs only have marginal access to them.

“Imagine saying to the defense industry, ‘Want to order a tank? Great. But we won’t tell you the price—not now, or ever. Just trust your broker that you are getting a really good deal,’” says Feldman. Yet, that is exactly what happens.

PBMs, particularly very large ones, also have a gatekeeping function. If medications are not included in formularies, or are too high up in the tiers, drugmakers might not see sales. So drug companies offer higher and higher rebates, and since the PBMs profit from rebates that are given after purchase, it is in their interest to put the drugs for which they get higher rebates in lower tiers. An efficient market would put generics, biosimilars, and less expensive drugs in the lowest tiers, but that isn’t always the case in the US.

As rebate incentives grow, so does the misplacement of drugs in formularies. Generic makers typically give no rebates—they just make much cheaper drugs—while big pharma companies give very high discounts for name-brand drugs, based on volume. An analysis of Medicare prescription prices estimated that an average 26% rebate was offered across its formulary, which includes many generic drugs that don’t offer any. So the average rebate for brand-name drugs is surely more than 26% for Medicare, and potentially even higher for private insurers.

According to an analysis published in 2021 in the Journal of Law and Bioscience, in 2010, 73% of generic drugs were on the least expensive tiers across formularies; in 2017, only 28% were. Similarly, in 2010 47% of drugs were placed in inappropriate tiers, while in 2017 74% were. These misplacements, added up to $13.25 billion in surplus expenditures on drugs between 2010 and 2017.

Further, just as insurance plans don’t know the full amount of the rebates negotiated with the manufacturers, they don’t know the reimbursement rates given to pharmacies. So the plan pays a certain price, and if the negotiated rate with the pharmacy is lower, the PBM can pocket the difference.

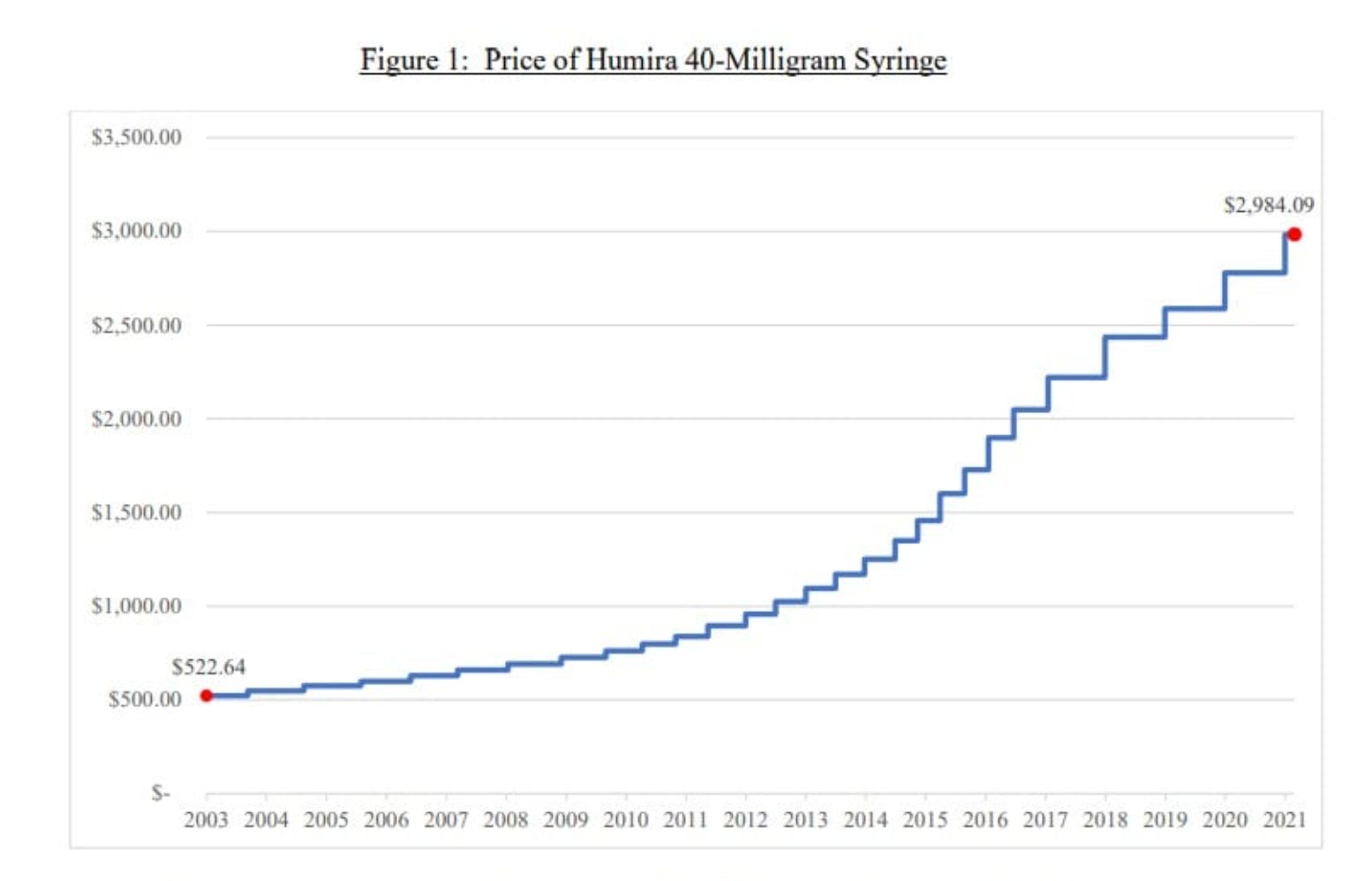

Humira’s price has gone up year after year since it was introduced in 2003, far outpacing inflation. In 2003, according to the US House Oversight Committee, a 40 mg syringe retailed for about $523. In 2021, it was nearly $3,000—if following inflation that price would be $767. The recommended dose for treating arthritis is usually 40 mg every other week.

One reason is rebates. Formularies are updated yearly, rebates renegotiated, and list prices continue to rise to make up for even higher discounts. But as Humira had managed to keep competition out, its rebates and discounts were likely just a way for AbbVie to maintain a good relationship with PBMs.

Now, however, things are different, and biosimilars are entering the market. But they could fail in the US if PBMs don’t include them in low enough tiers in their formularies. It could very well happen—for instance, the agreements PBMs make with AbbVie could include some conditions for keeping the biosimilar competition at bay in the formularies.

If so, PBMs would be better off by agreeing to the big brand’s demand than trying to broker a deal with the smaller competitor. “The problem is how volume works. The brand already has much of the market. The [biosimilar] is trying to get into the market but has to start with a much lower volume,” says Feldman.

Enter Amjevita’s double price strategy: A high price that could carry a high rebate, and a lower price with low or no rebate. “With respect to the two list-price approach that we’ve employed here at this launch, this is really to address the complexity of the US market,” said Murdo Gordon, who leads Amgen’s commercial operations, in a call with Amgen’s investors. “Pharmacy benefit managers have a business model that requires that they negotiate rebates with manufacturers, and so they would prefer a high list price,” he explained.

So Amgen’s pricing still plays into the PBM rebate game, while also illustrating just how much PBM rebates contribute to high drug prices. In this case, intermediaries between the manufacturer and insurance providers cost $1,731 per every Amjevita 40 mg pen. “Amjevita is available at both list prices for patients without insurance for purchase,” Michael Strapazon, a spokesperson for Amgen, told Quartz, adding that the company offers financial support to uninsured patients.

Many insured patients are unlikely to see the difference in the short term—copays for Humira and Amjevita will remain similar. Those purchasing the drugs without insurance, or paying coinsurance, will though. And eventually, the cost of inflated prices will trickle down to policy holders, too.

Things might be changing, however. Scrutiny over PBM activity is increasing at a bipartisan level, and policy proposals to provide more accountability to their work have been introduced in many states. As of April 2022, for instance, New York State has forced PBMs to disclose the full details of their deals with pharmaceutical companies, and several bills with similar scopes have been introduced in Congress since 2019. On Mar. 1, the House Oversight and Accountability Committee chairman, Kentucky’s Republican congressman James Comer, launched an investigation into the role of PBMs in the rise of drug prices.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.