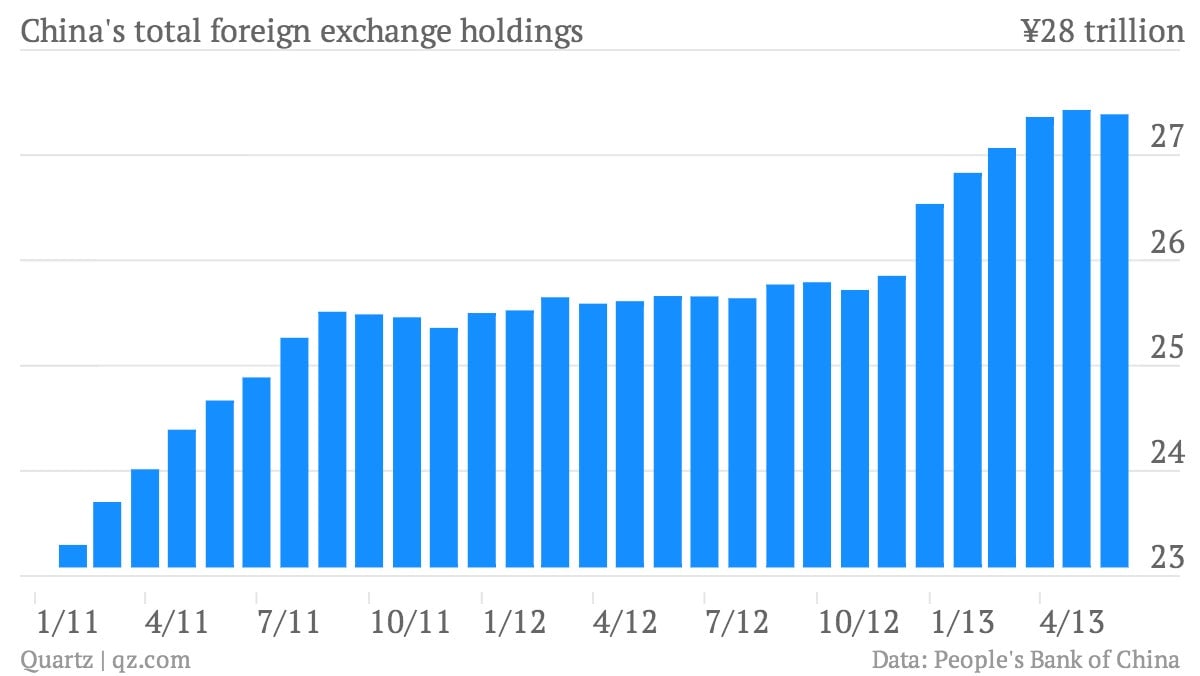

China’s foreign exchange balance fell 41 billion yuan ($6.7 billion) in June, putting the country’s overall holding of foreign exchange at 27.4 trillion yuan. That’s the latest sign that the new rules on foreign trade invoicing continue to block speculative inflows of cash. Though it’s too early to tell for certain, the data may also suggest that capital is seeping out of China, possibly due to bets that the yuan will weaken or growing concerns about economy’s state. The 41-billion-yuan decline was the first in seven months, and compares with a net increase of foreign exchange holdings of 66.9 billion yuan in May and 227.5 billion yuan in April. Here’s a look at how that position has varied over the last couple of years:

China’s foreign exchange balance fell 41 billion yuan ($6.7 billion) in June, putting the country’s overall holding of foreign exchange at 27.4 trillion yuan. That’s the latest sign that the new rules on foreign trade invoicing continue to block speculative inflows of cash. Though it’s too early to tell for certain, the data may also suggest that capital is seeping out of China, possibly due to bets that the yuan will weaken or growing concerns about economy’s state. The 41-billion-yuan decline was the first in seven months, and compares with a net increase of foreign exchange holdings of 66.9 billion yuan in May and 227.5 billion yuan in April. Here’s a look at how that position has varied over the last couple of years:

It’s unclear how much of this is held by the central bank, the People’s Bank of China (PBOC), versus commercial banks, since the PBOC stopped publishing that data in December 2012. (At last count, .) However, the PBOC is a significant chunk of that activity. And despite a dramatic fall in exports in May and June, a still-yawning trade surplus should have kept pressure on the PBOC to buy foreign currency, in order to , as would a strong bump in foreign direct investment in June.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

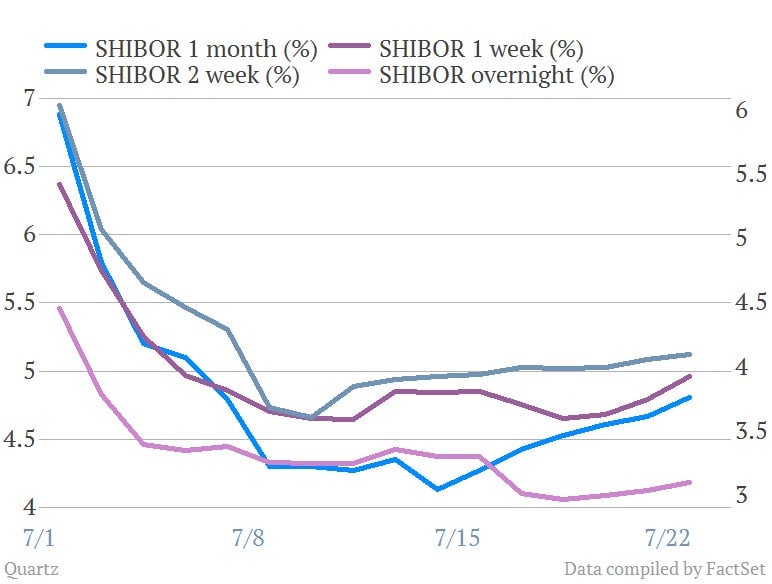

That suggests that capital is flowing out of the system, as individuals and businesses change yuan into dollars (or other foreign currencies) to invest abroad. In another sign that may be happening, domestic banks made $5 billion more in forex payments for clients (link in Chinese) than they received in forex receipts last month, despite a $27.8 billion trade surplus in June. Does the shrinking supply of money mean the central bank will resume open market operations once again, sending liquidity back into the system? Chinese analysts seem to think so. What will happen if the bank sits on its hands is that capital outflows will likely continue to shrink the amount of money in China’s economy. That will put pressure on interest rates, making it harder for commercial banks to lend. In fact, that may already be happening; as you can see, the interbank rates—particularly the one-week and one-month—have been edging up in the last week or so: Given the lack of detailed data, it’s impossible to tell for sure whether the trend in forex holdings represents capital flight. But if it does, and if the trend continues, tighter money supply could set off another rate spike like that we saw in June, which would endanger growth once again.