Dollar stores are now getting too expensive for many Americans

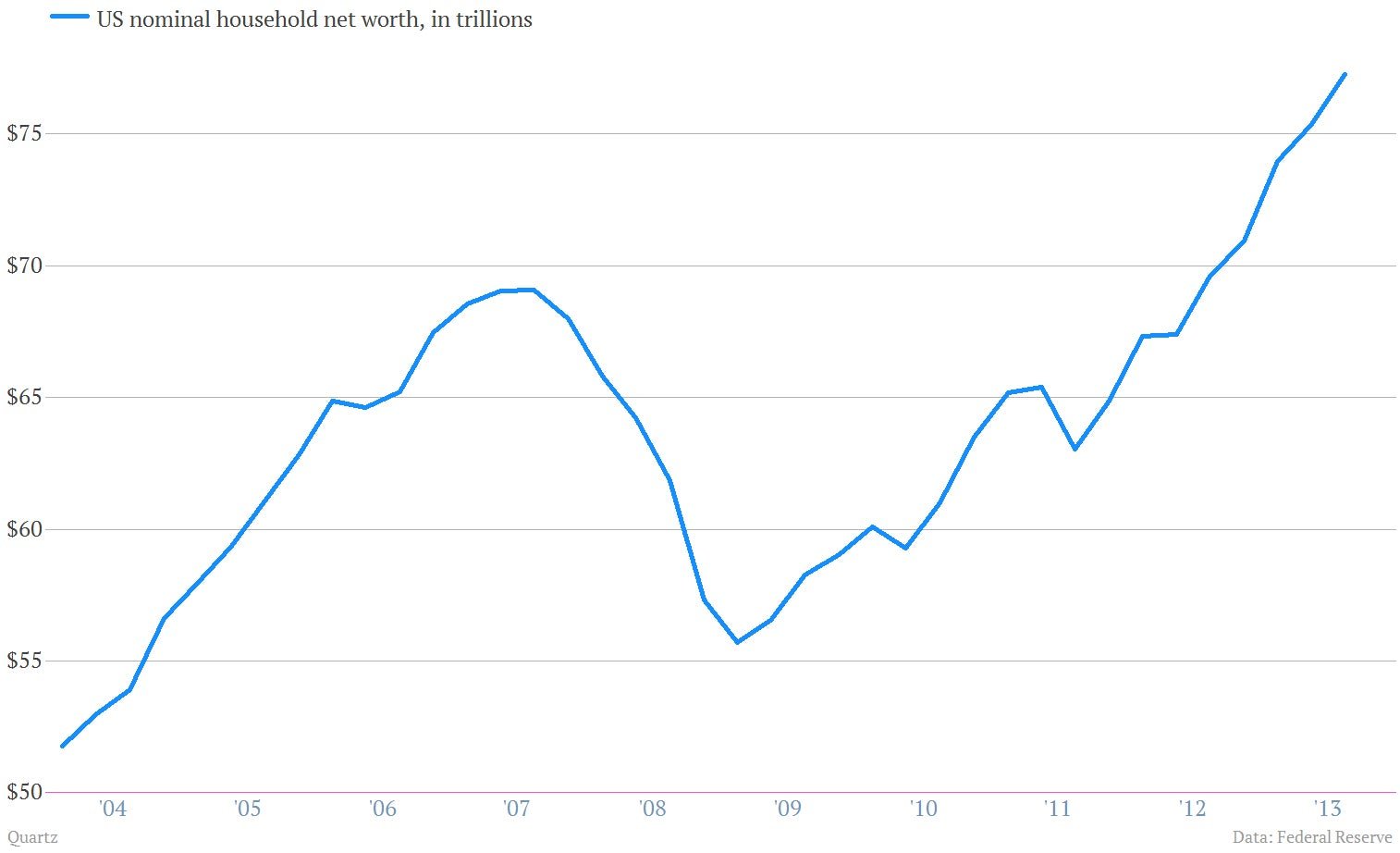

At first glance, the fortunes of American families have significantly improvement recently. Household net worth has rebounded back to roughly where it was before the financial crisis.

At first glance, the fortunes of American families have significantly improvement recently. Household net worth has rebounded back to roughly where it was before the financial crisis.

At first glance, the fortunes of American families have significantly improvement recently. Household net worth has rebounded back to roughly where it was before the financial crisis.

Why? A surge in stock and real estate prices. The stock market is up 46% since the end of 2010. And after years of pain, housing prices are rising too.

There’s a catch. While about 50% of Americans own some kind of stocks—either individual shares or mutual funds—the richest Americans own most of the market. That means most of the exceptional stock market gains accrued to what Federal Reserve research describe as “a small number of wealthy families.”

Homeownership is a bit more democratic. Houses account for a larger chunk of the assets of the US middle-class compared to the wealthy. But again, the poor are left out.

No, the poor rely not on asset prices, but on wages, Social Security, and government transfer payments for their income. That hasn’t been a good place in recent years. Wages have been stagnant. Government transfer payments have been under fire. (Extended unemployment benefits expired late last month for roughly 1.4 million Americans after a federal program lapsed. And it seems like the US Congress is set to cut transfer payments such as the US food stamps program.)

Economists argue that things like food stamps and unemployment act as crucial bits of stimulus when the economy is weak. Cutting them can act as a headwind to growth. That’s certainly the case for low-end retailers such as Family Dollar. The store chain’s shares fell sharply this week after it reported disappointing earnings. Family Dollar CEO Howard Levine had this to say on the subject:

For the last several quarters, we’ve discussed the economic challenges our customers are facing. Over the last two years, I think we’ve seen a growing bifurcation in households. Higher-income households who have benefited from market gains, better employment opportunities, or improvements in the housing markets have become more comfortable and confident in their financial situation. But our core lower-income customers have faced high unemployment levels, higher payroll taxes, and more recently reductions in government-assistance programs. All of these factors have resulted in incremental financial pressure and reduction in overall spend in the market.

Translation? As poor Americans come under more and more pressure, more and more of Family Dollar’s revenue is tied to low-margin sales of necessities like food. (Sales were strongest during the first fiscal quarter in Family Dollar’s “consumables” category, especially in areas like frozen food.)

The fact that so many Americans are being forced to curtail spending at the cheapest discount retailers should give anybody cheering the US recovery something to think about.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.