“The economy has been stronger than we thought. That’s a good thing, obviously.”

“The economy has been stronger than we thought. That’s a good thing, obviously.”

Bank of England governor Mark Carney’s defensive tone as he fielded pointed questions at a press conference today cast some doubt on whether the dilemma he faces could be called “good.”

As Carney reassured markets that an interest rate rise is not imminent, he also announced that the British central bank has revamped its policy of “forward guidance” on interest rates, and released an of the UK’s economy. The bank now expects UK GDP to grow by a robust 3.4% this year, up from its previous forecast of 2.8%.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

But what is making life uncomfortable for Carney is that the bank’s existing forward-guidance policy, unveiled only six months ago, served to confuse as much as enlighten. Back then, the bank pledged to keep its benchmark interest rate on hold until the unemployment rate fell to 7%. Three months ago, the bank put the probability of this threshold being reached in the current quarter at 10%, but today—with the rate at 7.1%—it revised those odds to 70%. As the jobless rate tumbled faster than the bank’s projections, markets started pricing in a rate hike much sooner than the bank seems comfortable with (next year, at the earliest).

The bank’s latest “phase” of forward guidance is designed to avoid these market misunderstandings. It seems designed, in fact, to make its future intentions much harder to discern. While some applauded the new policy, analysts at Schroders likened it to a “bamboozling cluster bomb.”

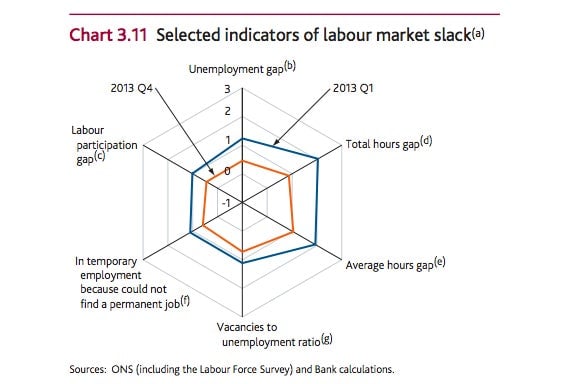

The bank suggests that it will now track more than a dozen measures of “spare capacity” to determine the course of interest rates. The bank reckons that despite the falling jobless rate, there is slack in the economy worth up to 1.5% of GDP, as shown by unemployment that remains above its “medium-term equilibrium” of 6-6.5% and surveys that suggest workers would prefer to work more hours. Stagnant wages and low productivity are also blights on the country’s otherwise encouraging recovery. And so the bank’s guidance will morph into multi-dimensional analyses of labor and output gaps, as illustrated in charts like this:

In a sense, the bank’s shift on forward guidance is an attempt to have it both ways, reinforcing the discretion that central bankers have always coveted while giving a nod to a more transparent, data-driven approach to decision-making. Although it is now harder to predict what the bank will do with interest rates, the markets should appreciate its decision to publish a broader set of indicators and forecasts. Of course, this exposes the bank to getting even more of its official projections wrong, but that is the nature of economic forecasting. If anything, the previous preoccupation with a single indicator, the unemployment rate, greatly oversimplified the complexity that bedevils monetary policy in the real world.

The bank may have botched its initial attempt at forward guidance, encouraging markets and the media to fixate on form over substance, but its new policy—however vague—sensibly acknowledges the fallibility of economic forecasting. It is not surprising that the governor has come under fire for the bank’s poor forecasting record, but slavishly setting rates according to an arbitrary, inflexible formula would be an even bigger mistake.