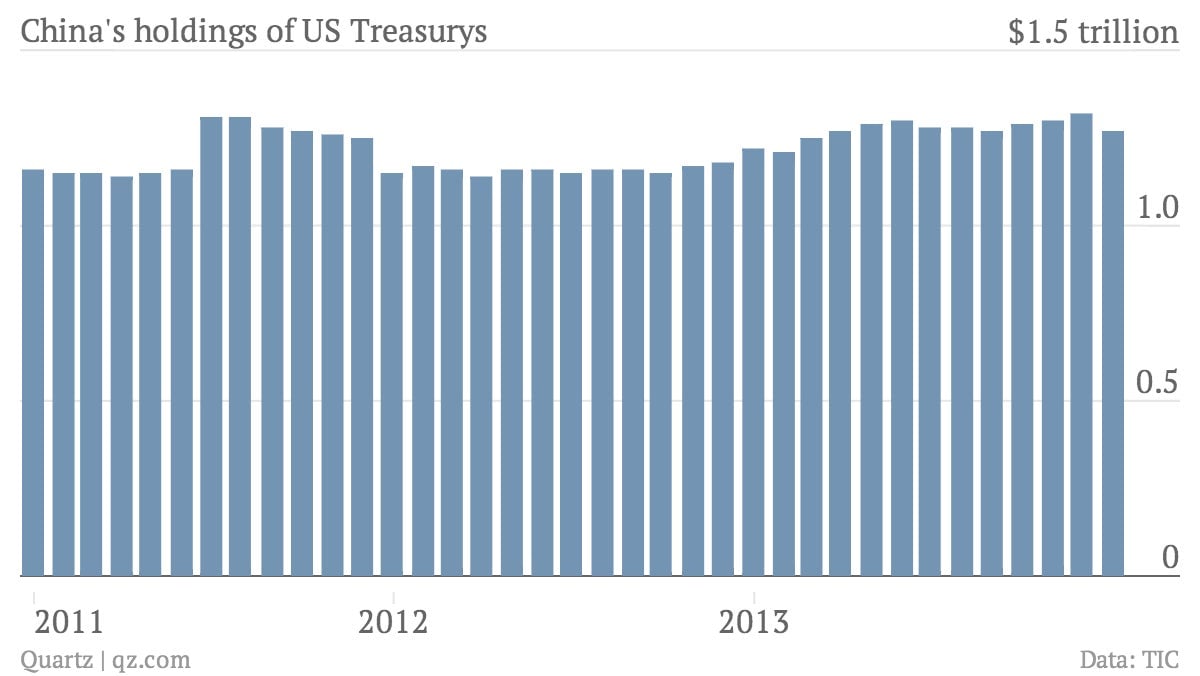

China’s holdings of US Treasurys dropped to the lowest levels in two years after China dumped $47.8 billion in paper—equal to about 3.6% of its Treasury holdings as of November—bringing its total holdings to $1.27 trillion. Not that this should come as a shock. Yi Gang, a deputy governor of China’s central bank, hinted at the move when he announced in late November that the country no longer benefits from increasing its foreign reserves.

China’s holdings of US Treasurys dropped to the lowest levels in two years after China dumped $47.8 billion in paper—equal to about 3.6% of its Treasury holdings as of November—bringing its total holdings to $1.27 trillion. Not that this should come as a shock. Yi Gang, a deputy governor of China’s central bank, hinted at the move when he announced in late November that the country no longer benefits from increasing its foreign reserves.

Though this news is likely to stoke fears of a US bond market sell-off, it’s way too early to judge whether this is a fluke or a new PBoC strategy. If China continues to slash its Treasury holdings, that could be grim tidings indeed for the US Treasury market, especially with the Federal Reserve also winding down its bond-buying, as BNP Paribas’s Aaron Kohli told Caijing. (Note also that even as China and Japan offloaded US Treasury securities, overall foreign holdings of US Treasurys increased ever so slightly, thanks largely to a .)

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

But there are some reasons to doubt that this is the new normal. For one, Yi’s remarks—implying that China will scale back its currency interventions, curbing its demand for US government debt—have the paradoxical effect of inviting more speculation on yuan appreciation. The way this works is that the PBoC buys dollars at its desired exchange rate in order to keep the value of the yuan, which is pegged to the dollar, from rising too much. If it stops buying dollars, there’s nothing preventing the yuan’s value from rising.

The promise of a strengthening yuan adds another layer of appeal to the already inviting returns available in wealth management products and money-market funds. If those twin attractions pull in more “hot money,” as speculative capital is called, and if foreign direct investment and net exports continue to boom, the PBoC will have to keep buying dollars—or allow a stronger yuan to hurt exports.

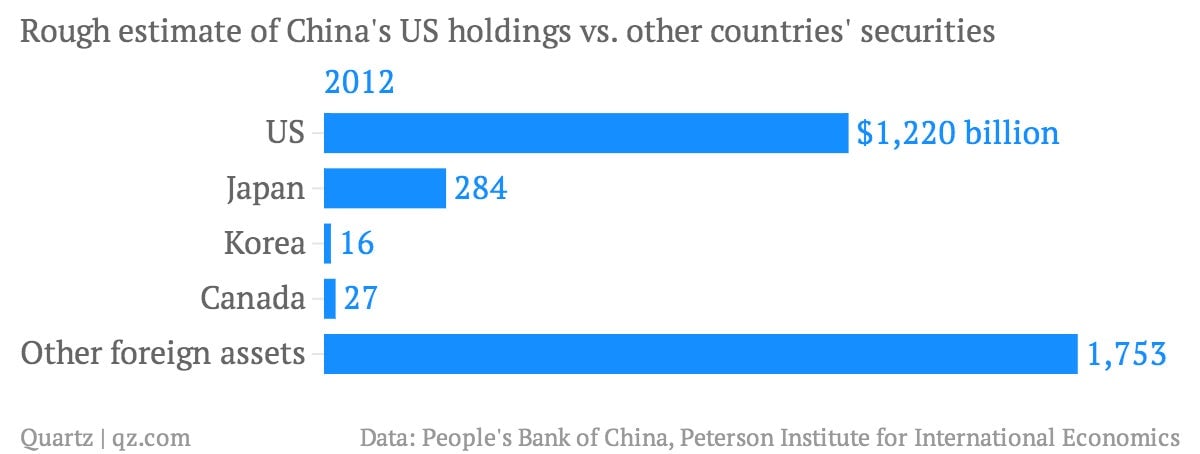

And as long as it keeps piling dollars into its reserves, the central bank has few other options than US securities. Though it has been diversifying into Korean, Canadian and Japanese securities of late, as the Peterson Institute of International Economics’ Kent Troutman recently pointed out, the PBoC will still be hard-pressed to find a market big and liquid enough to be a suitable alternative to US Treasurys. To give you a sense of proportion, check out this rough approximation of Chinese foreign reserve holdings:

If and when the Chinese government does finally loosen its hold on the yuan, however, the impact on US government bonds will very likely be a big one.

“When China finally begins to allow the [yuan] to float more freely and thus does not have to accumulate further foreign reserves, a large, price-insensitive source of demand (and thus force for lower rates) will exit the market,” wrote PIIE’s Troutman in a recent blog post. “Who steps in (and at what price) to provide the demand, as well as the speed and manner in which China unwinds its own unconventional monetary policy, will determine the ultimate repercussions on the global financial markets.”