It’s tough to figure out where China’s next debt panic will come from these days. Just as trust products had surpassed local government-financing vehicles as the frontrunner, a series of events—including a default and a trading suspension—in the last two weeks have pushed corporate bonds to the fore.

Though they’re not as risky as trust loans, China’s onshore corporate bond market is nearly the same size, 9 trillion yuan ($1.5 trillion), making up around a quarter of China’s $6-trillion shadow finance sector (which refers to credit issued outside the traditional deposit-and-loan model). More worrying for investors than that market’s size, argues David Cui of Bank of America $BAC/Merrill Lynch in a recent note, is the incentive schemes that drive debt issuance—and how those have left retail investors and major banks vulnerable to unacknowledged risk.

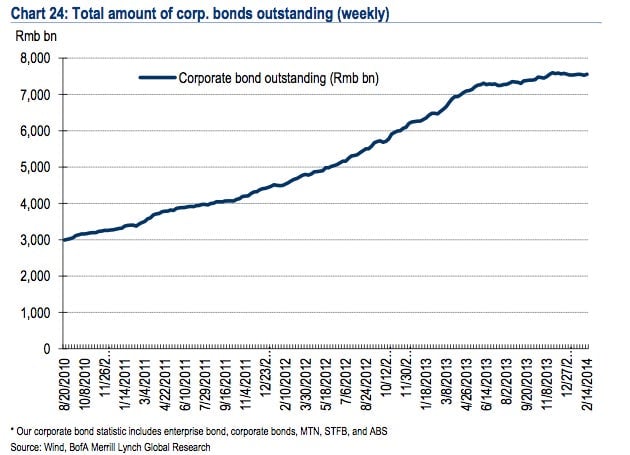

China’s onshore corporate bond market has exploded in recent years, jumping from 800 billion yuan in 2007. While high interbank rates have discouraged issuances in the last nine months, outstanding corporate bond debt is more than 9 trillion yuan, says BofA/Merrill Lynch. Around 38% of that is owned by banks, says BofA/Merrill Lynch.

The absence of risk explains a good deal of this surge in corporate debt issuance. Until a small solar company’s recent default, no company had defaulted on a corporate bond in recent history. That lack of risk has made bonds unusually cheap across the board. Since they’ve been essentially guaranteed a return, banks often hold bonds to maturity (registration required), as Diana Choyleva of Lombard Street Research says. Meanwhile, “the government can use them as ATMs to bankroll its fiscal expansion without having to worry about its credibility,” writes Choyleva.

A regulatory power struggle is another force behind the bond boom. Four regulators currently oversee the market; eventually, one or two will likely be put in charge. In order to boost their claim, each regulator competes to expand their corner of the market as quickly as possible. In the rush to increase the number of bonds, there’s less supervision of credit quality, says Cui.

Then there’s demand. Aside from banks, the other sector doing big bond-buying is wealth management products (WMPs), retail investment products that bundle shadow loans. These now account for around 30% of the corporate bond market, up from 20% in late 2011, says BofA/Merrill Lynch.

The fact that most WMP customers assume that their investments are protected from default means they reward high yield over risk-management. That encourages WMP managers to pile into the riskiest corporate bonds. Another big holder of corporate bonds is the booming sector of online money-market funds, including Alibaba’s Yu’e Bao.

These fund managers are given an additional sense of security from China’s six bond-rating agencies. The fact that their revenue comes from the ratings fees they charge the bond issuers discourages pessimistic assessments. This skews the ratings to the point where Cui and his team consider anything rated AA and lower to be fairly risky.

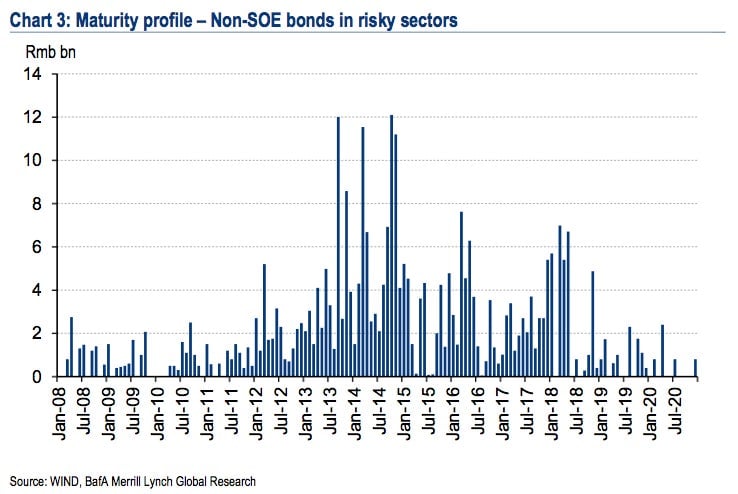

This series of perverse incentives means that a rash of defaults could trigger an “unpredictable” chain reaction throughout China’s financial system, says BofA/Merrill Lynch. Of course, when that theory will be tested is anyone’s guess. But based on this chart of peak-maturing periods for the riskiest bonds—including those of private companies in sectors with overcapacity, such as coal, property, solar and transport—we should see some defaults this year: