Once they swaggered, but now they’ve shriveled.

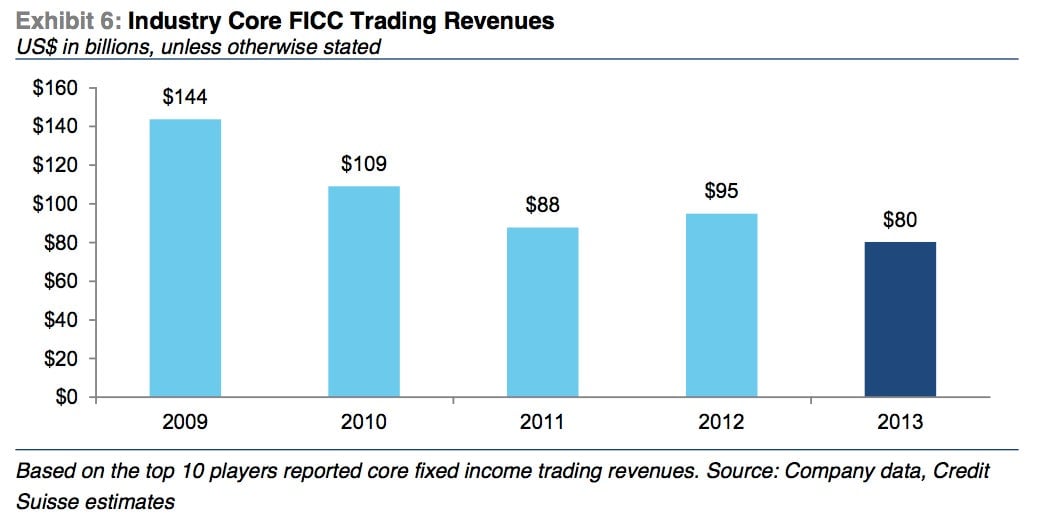

Fixed-income, currencies, and commodities trading units (FICC) generated $144 billion in revenue for the top 10 banks in 2009. Last year, that figure was $80 billion, down 44% from the peak, according to a recent research report by Credit Suisse analysts.

The report highlights FICC activity at 10 big banks, including JPMorgan $JPM Chase, Citigroup $C, Bank of America $BAC, Deutsche Bank, and Goldman Sachs $GS. And it attributes at least some of the decline in FICC trading revenue to a drop in the trading of government bonds, complex derivative interest rate securities, and esoteric debt like commercial and home loans. We’ve already noted a similar declining trend in FICC at banks like Goldman Sachs, where FICC once represented 60% of the firm’s overall revenue.

Here’s a look at the decline in trading revenue over the past four years, based on Credit Suisse’s research:

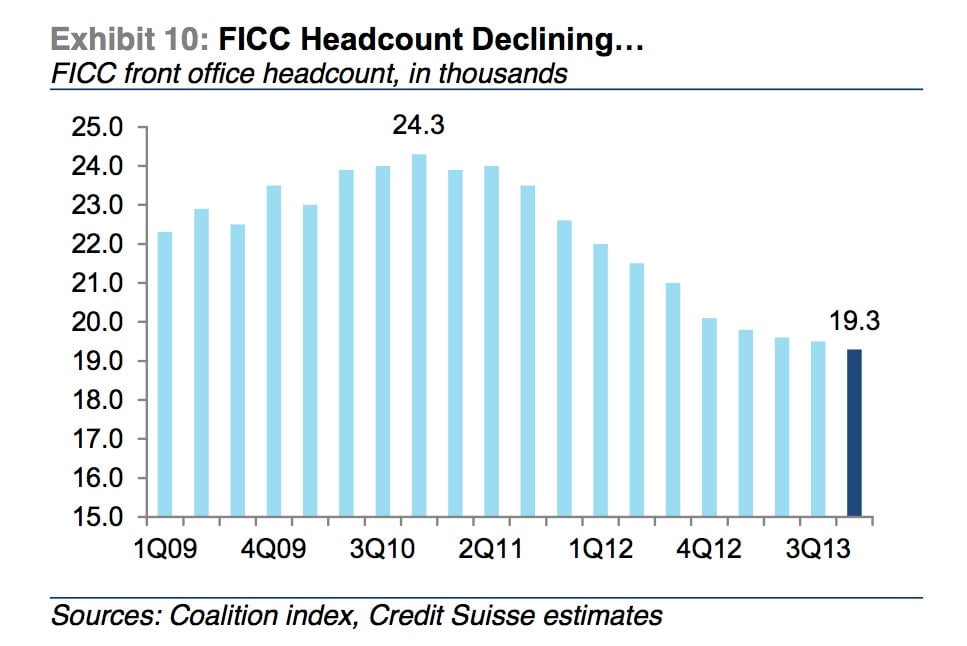

And when trading revenue disappears, so do traders. Credit Suisse data indicates headcount fell by nearly 21% from its peak at the end of 2010:

These trends aren’t likely to end anytime soon. Firms like JPMorgan and Citigroup have already signaled that they are expecting to see fixed-income trading down significantly, which could contribute to weak first-quarter results.