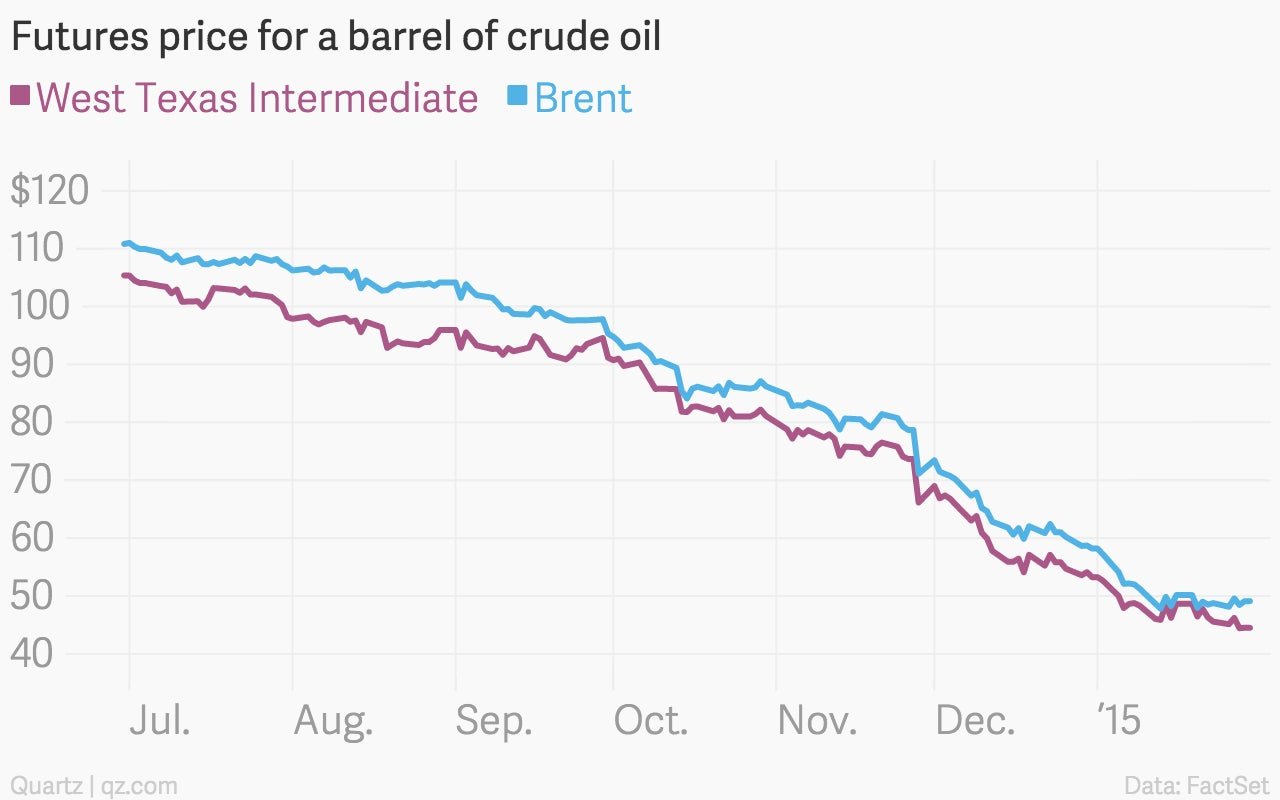

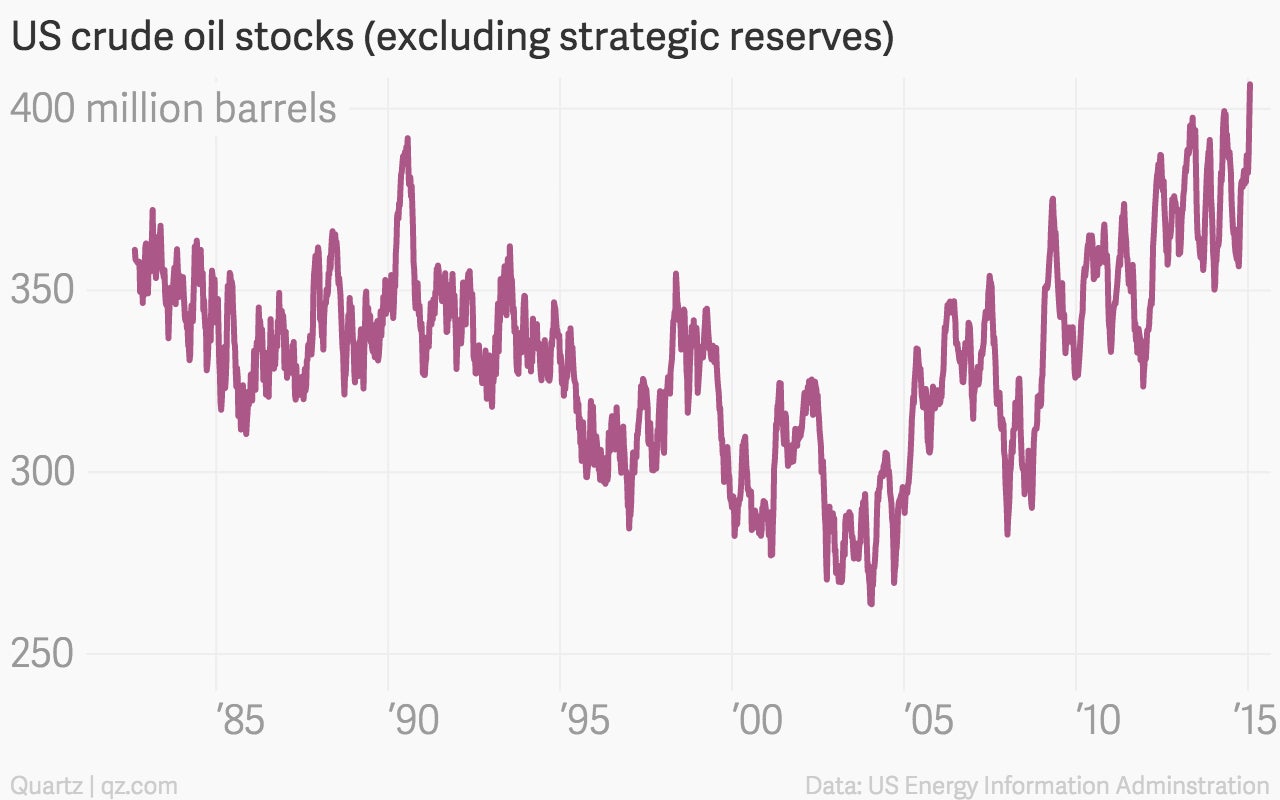

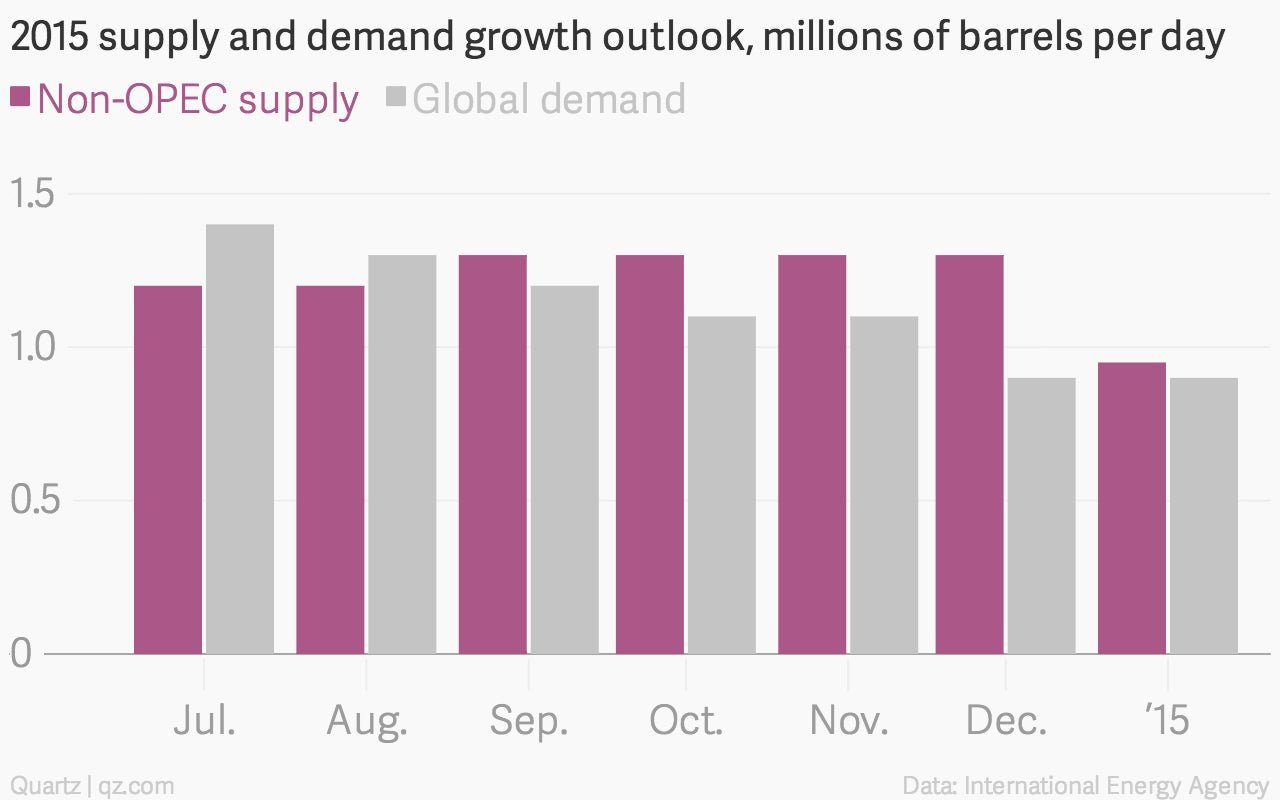

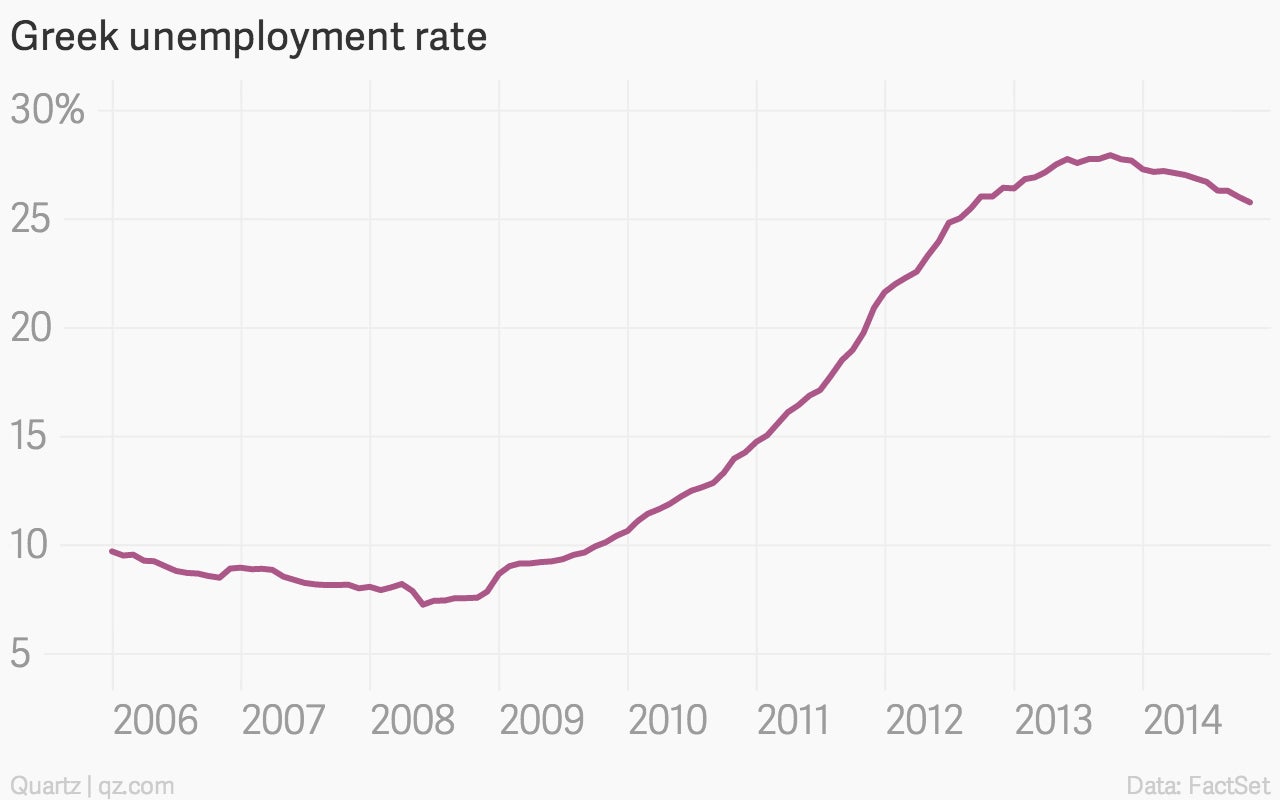

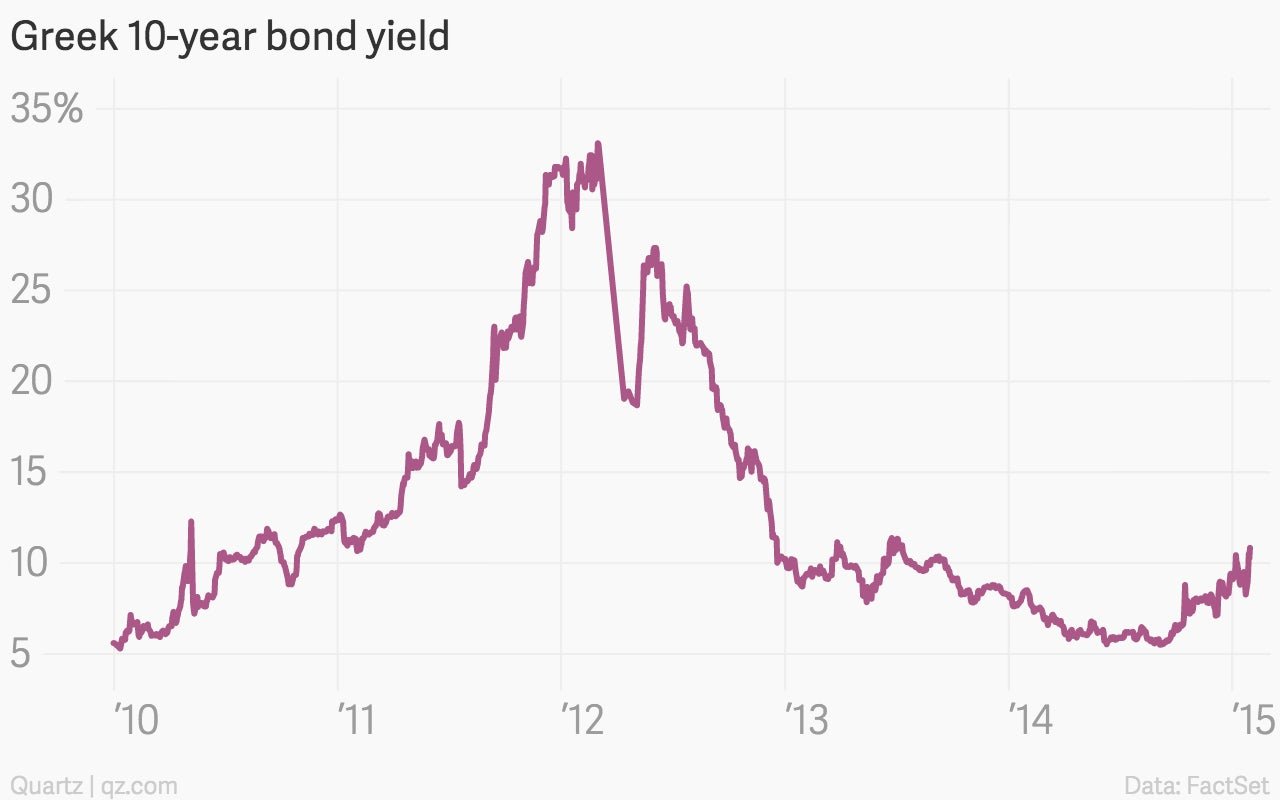

Oil and central bank action dominated economic headlines in January, but lots of other chart-able stuff happened this month. (We’ve got your back, Greece.)

Let’s start with oil, though—because it’s hard to overstate the impact of what’s happening there.