How the US post office can save America—and itself

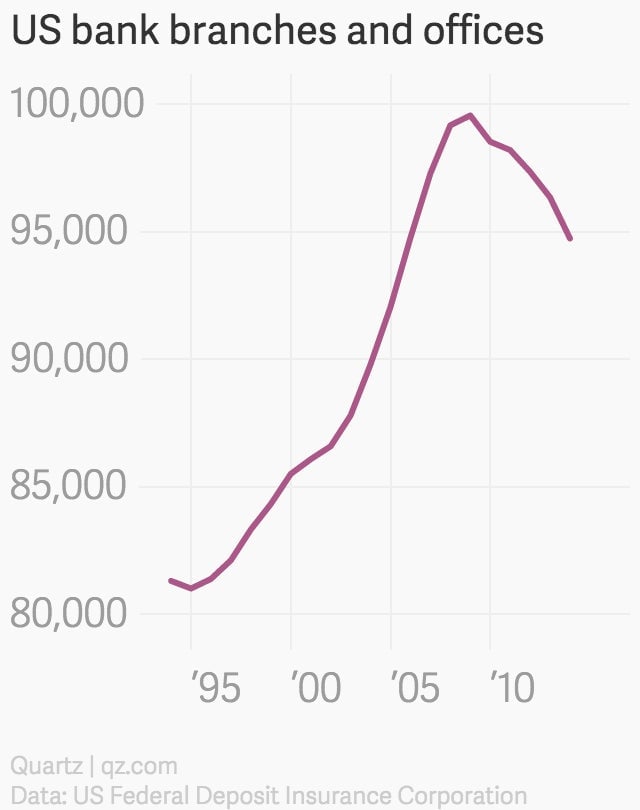

Since the financial crisis, more than 4,800 bank branches have disappeared from the American retail landscape.

Since the financial crisis, more than 4,800 bank branches have disappeared from the American retail landscape.

But in many parts of America, the decline of the bank branch has barely been noticed

That’s because in these neighborhoods, banks have already been gone for decades.

The departure of banks from poorer, mostly minority neighborhoods beginning in the 1970s has forced millions of American to manage their financial lives using a patchwork system of payday lenders, check cashing joints, and prepaid debit cards. Such services offer few of the protections of the traditional banking system in exchange for nosebleed fees and transaction costs. (The recent RushCard debacle, in which thousands of people were unable to access their funds for more than a week in some cases, underscores the precarious nature of fringe finance.) In other words, it’s a bad deal.

In her new book, How the Other Half Banks, University of Georgia law professor Mehrsa Baradaran traces the historical origins of the US banking system, with particular emphasis on the regulatory shifts that began in the late 1970s. These changes enabled banks to consolidate across state lines and leave less profitable—read poorer—portions of the populace to their own devices. And she puts forth her own modest proposal for how to change the status quo by leveraging an American institution struggling itself to stay relevant: The US Postal Service.

Baradaran stopped by Quartz’s New York offices earlier this week. Here’s our discussion, lightly edited for clarity and concision.

Quartz: So bring us up to speed. How did we end up with the situation we have now in terms of the share of the unbanked in the US? My understanding from the book is that deregulation and ability of banks to charge more fees on accounts, essentially allowed banks to dissuade people from having accounts.

Mehrsa Baradaran: I think the fees are symptom and not the cause. Banks are going to compete for the higher-return revenue. That’s what banks always want to do. And before, we were forcing them not to do that. Once we stopped forcing them, market forces took over. Banks are obviously going to go and try to get the higher-net-worth people in the highest-net-worth locations, and that’s why you’ve got these banking deserts.

One of the more infuriating points of the book was where you talked about a report that showed from 2008 to 2013, banks shut down nearly 2,000 branches—93% of which were in neighborhoods that were below the median income level of the US.

It’s kind of like redlining, but economic redlining. You’ve got banks merging much more so than before, and weaker banks sort of being swallowed up into the whole. And so of course they’re going to shut down their least profitable branches and that’s obviously going to be inner city, low income, largely minority neighborhoods.

And is there a correlation between the decline of bank branches in those areas and the growth of fringe banking, like check-cashing facilities?

Absolutely, there’s a direct causation, not even a correlation. John Caskey in his book Fringe Banking shows exactly that: As soon community banks leave, the fringe bankers come in to fill the void. There was no such thing as payday lending before the 1980s, and now there are more payday lending outlets than Starbucks $SBUX or McDonald’s.

There have always been loan sharks—let’s be clear about that. But the large-scale industry of payday lending was not something that we had in America.

Can you talk a little about the demographics of those who use payday loans and other fringe financial products, like pre-paid cards, instead of bank accounts?

Those who don’t have bank accounts and use prepaid cards, that’s lower income, around $30,000 in annual income. So that’s a lot of people.

But there’s also a big pool of underbanked folks. They have a bank account. But they rely on fringe lenders for their day-to-day needs. They have jobs and steady paychecks, because you need to have a paycheck and you also need to have a bank account to get a payday loan. It is the middle class. … the people that come in are your neighbors, middle-class folks who don’t have a big savings buffer and sometimes need an emergency loan.

You make the point people are not going in blind when they get a payday loan. They know it’s a bad deal, but they just feel like their back is against the wall.

Look, the poor are not stupid. Speaking for myself, I think a lot of people who use payday loans are much more personal financially savvy than I am. They have to be. A lot of time they take out one loan to pay for the other and they’re arbitraging interest rates and pre-payment penalties. They know exactly what they’re doing. There just aren’t that many alternatives.

So for a person who needs money, it’s a very rational choice to take out a payday loan. Often the alternative is to go to your friends and family. There’s a lot of downside there. Or you go to the black market. And there are still people who go to loan sharks. But I would take a payday lender, any day, over that.

Bank branches have largely left lower-income neighborhoods. And you point out that one of the institutions that hasn’t left those neighborhoods is the post office. Can you talk to me a little bit about the postal banking idea.

First of all, I want to say it is totally not revolutionary. Postal banking was proposed in the US starting in 1873. After 40 years, it was passed in 1910 and it lasted until 1966. Every other developed country has this.

Here’s the point. You’ve got all these banking deserts and banks that have left these areas, and the post office remains. They already operate in cash. They have a nationwide network. And so they’re well-poised to offer very simple financial services and small loans.

One of the push-backs to that idea is that, “Postal workers deliver letters they’re not trained to be bankers.” But you make the point that the people who are working in check-cashing facilities are not the same as people working on Wall Street, they’re essentially retail employees.

Postal bank employees would not be underwriting, they would not be doing an IPO. It’s not rocket science and it doesn’t take particularly special training.

We’ve seen Bernie Sanders make some proposals on post office banking. I think Elizabeth Warren has brought it up.

I’ve been working with all of them behind the scenes. I first wrote this article three years ago proposing postal banking, and in 2014 the Post Office Inspector General’s office did a white paper on postal banking, and since then there’s been a lot of movement in this. And recently there’s been a little bit more of an uptick, with Bernie Sanders.

The problem is just not going to go away. In fact it’s just going to get worse. There’s more and more bank consolidation, and fewer banks and higher inequality. You’re going to see this gap grow wider. So I think it’s time to revisit the postal bank.

Could you talk a little bit about what kind of loans you envision these banks making? I think that’s one of the places where a lot of people will say, “Is there going to be political pressure to loan people money that essentially taxpayers will be on the hook for if there are losses?”

So there’s two ways we could structure loans. One could be like a payday loan, you know, secured against your future income. It would operate the same way but with much lower interest charges. Now a lot of payday loans—because they have such high interest and high fees—are meant to be rolled over and over again. But the post office can do more like an installment loan. You could pay it back slowly over maybe five or six paychecks. But again, we’d cap them at like $500 to $1000 dollars. We’re not talking huge, risky loans.

The other way you could do it—and the way the UK does this—is essentially you have a checking account which you could overdraw by some amount. And you have a negative balance. You accrue interest on that negative balance until you push it back up to zero. And so that’s the way that you’re essentially loaning. And when your paycheck comes, it repays the negative balance. The interest rate would be some non-usurious rate. That would be another way for simple lending.

In terms of the political odds of pushing this through, you’ve written an interesting history of what transpired in 1910. Essentially the post office bent over backwards then to explain to the banks, “We’re not trying to steal your depositors. You’re not interested in this business anyway, we’ll just do it.” Do you think the post office will have to make the same argument this time around?

Yeah. You have to, one, convince the banks that we’re not after their customers. You have to get banks off your back, because the banking lobby is very, very strong—especially the community banks. You saw with Walmart $WMT. Walmart tried to become a bank, that got shut down quickly and efficiently. But I really think it’s an honest argument to say, “These are not your customers you do not make these loans. You are not interested in this business.”

Now the sector that you do worry about is, of course, the payday lenders and check cashers. But I honestly think with a straight face we can say, “Tough.”

It’s a hard political argument to make to defend payday lenders and check cashers.

In chapter four or five of the book, I talk about the public’s antipathy toward usury. Nobody likes payday lending. Yes, maybe this industry goes out of business, but tough. We’re okay.

So what do you think the chances are that we get another postal banking system anytime soon?

You know, it took 40 years the first time, I hope it doesn’t take 40 years this time. I think that you have to get the banks at ease. And I think you have to really convince people that there’s postal banking, or we lose the post office. The post office has reached its maximum credit line from Treasury, so it’s either cut costs dramatically or add revenue. And this is a way for them to add revenue without taxpayer funds. It really is a no-brainer, I think.