School was in session in the euro zone last night, and the lesson was on competitiveness. Specifically, it was on the gaps between productivity (too low) and labor costs (too high) in some European countries, which make them less competitive than others. European Central Bank president Mario Draghi lectured the 17 euro-zone heads of state for two hours, starting at 11pm yesterday. Apparently, there were lots of charts involved.

“Draghi effectively said, ‘there are two ways to close this gap, either reduce labor costs or raise productivity’, and he said that the bigger the gap in a particular country, the less room there was to act to close it,” an in-the-know diplomat told Reuters. German Chancellor Angela Merkel, meanwhile, found it “very interesting.”

Lack of competitiveness drives up unemployment. Germany is among the euro zone’s most competitive countries. Sure enough, its unemployment rate is a super-healthy 5.9%. Workers in Italy and Spain are too expensive relative to what they actually produce—and their respective unemployment rates were 11.7% and 26.0% in January.

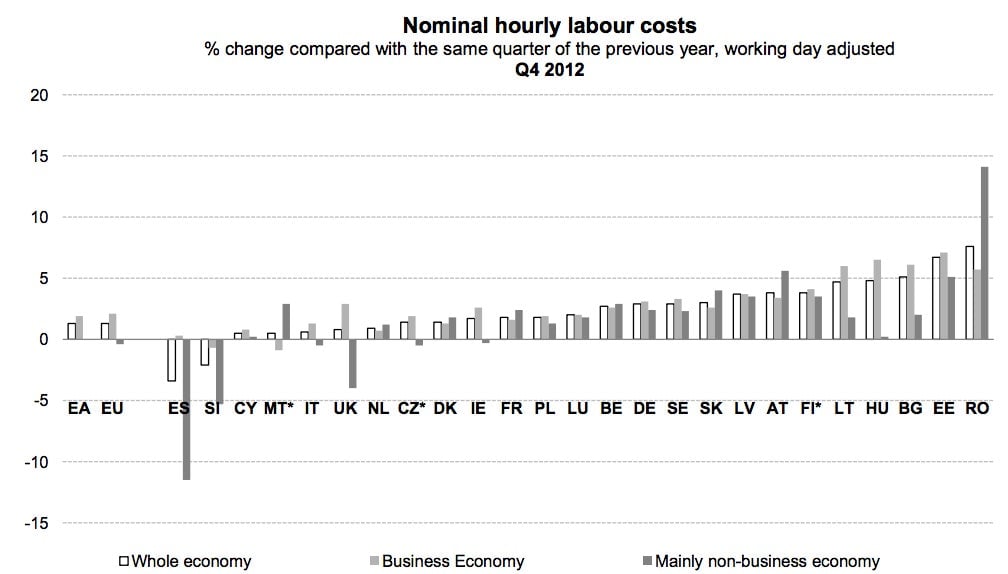

Trends in unit labor costs (which divide labor costs by real output) therefore can signal that adjustment is underway. And lo, we have some fresh data on that today, as Eurostat reported Q4 2012 labor costs. Here’s a look at the individual country breakdown (pdf):

The biggest fall in labor costs last quarter was in Spain: 3.4%, year-on-year. That’s good, since they had risen slightly in the first three quarters of 2012. But other problem countries—Italy, Ireland, Portugal and France—all increased, by between 0.6% and 1.8%. The slightly better news is that Germany’s rate rose 2.9%, slightly reducing the gap between them and it.

Even if all the ailing economies were like Spain, though, their falling labor costs wouldn’t fix competitiveness in the long term. For one thing, the world outside the euro zone teems with labor that can be had for even less. And while lower wages could help employment, they also risk suppressing domestic demand, which would be economically destructive.

Draghi’s other solution—raise productivity—is better in the long run. But that requires investing in skills, infrastructure and technology, among other things. We’ve already covered why businesses aren’t likely to do that in several of the problem countries. And unfortunately, with austerity still the euro-zone watchword, governments won’t be doing too much of it either.