It looks like the most frequently cited justification for fiscal austerity in the aftermath of the global financial crisis is based on a boneheaded Microsoft $MSFT Excel error.

When advanced economies began slumping in 2008, the immediate debate was whether to boost growth with short-term deficit spending or reduce government debt. Advocates of the latter approach often cited an exhaustive survey by economists Kenneth Rogoff and Carmen Reinhart (pdf), who found that economic growth slows after a country’s debt grows to 90% of its GDP. Countries in that band—like the US, UK, Greece, Ireland, Italy, and Japan—were apparently risking long-term prosperity for short-term relief.

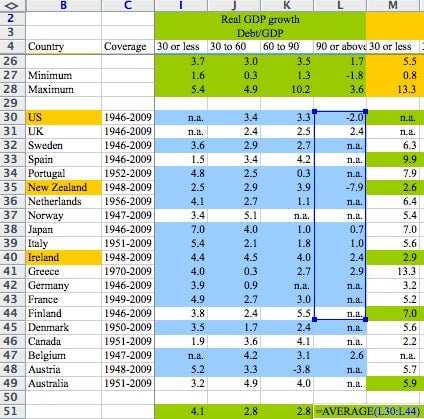

But new research suggests that the magic 90% number isn’t so magic after all, as the Roosevelt Institute’s Mike Konczal explains. Three economists at the University of Massachusetts, Amherst, set out to replicate the Rogoff-Reinhart findings and instead found the spreadsheet equivalent of a typo, which you can see in the image above. That blue grid in column L should go down five more cells, the new research claims. In other words, Denmark, Canada, Belgium, Austria, and Australia weren’t included.

And that’s not all: They question the way that the Reinhart and Rogoff included different countries in their averages, giving 19 years of high-debt growth for the UK the same weight as one year of high-debt recession in New Zealand. Reinhart and Rogoff also excluded some high-debt, high-growth countries from their count, although it’s not clear why.

I’ve emailed Reinhart and Rogoff for their response but haven’t heard back.

Factoring in these concerns, the new study finds that “the average real GDP growth rate for countries carrying a public debt-to-GDP ratio of over 90 percent is actually 2.2 percent, not -0.1 percent.”

That’s a bit of a fly in the ointment for austerians everywhere, although, as the Economist’s Ryan Avent points out, the study didn’t launch the movement for austerity, it merely served as its primary public defense. Likewise, the new study is no reason to assume that a high debt-to-GDP ratio is a particularly good thing, either. Far better to consider the individual circumstances and challenges faced by different economies: Just because Greece and Japan have stratospheric debt levels doesn’t mean they merit the same kind of management.

The new results shouldn’t be too much of a surprise, however: The comparison between the US and UK economies—and their respective embraces of temporary stimulus and debt reduction—has already raised the question of whether austerity promotes growth. Even the International Monetary Fund has changed its tune from the early days of the crisis, suggesting that maybe it’s time to be a little more profligate.

Update: While we wait for a full response from Rogoff and Reinhart, here are brief comments they made defending their work to the FT’s Robin Harding:

Update II: You can read their full response here; while they cite other studies with similar results and suggest that the differences found by the new research are small, they don’t respond to specific critiques. Our Matt Phillips notes that US history offers its own critique of the paper, and here are some examples of how influential the two economists have been.