While we may never see another phenomenon like the iPhone during its early days, that doesn’t mean Apple’s best years are behind it. A closer and (with apologies) longer look at Apple’s numbers paints a picture of a company that’s more adept than most at playing the long game.

While we may never see another phenomenon like the iPhone during its early days, that doesn’t mean Apple $AAPL’s best years are behind it. A closer and (with apologies) longer look at Apple’s numbers paints a picture of a company that’s more adept than most at playing the long game.

Apple’s Dec. 2016 quarterly results, announced Jan. 31, were better than expected. Revenue reached $78.4 billion, an all-time record that beat Apple’s usually dead-accurate guidance of $76 billion to $78 billion. iPhone numbers, 69% of company revenue, also reached an all-time high of 78.3 million units. Company executives themselves were surprised by a higher-than-expected proportion of the dual-camera iPhone 7 Plus model, which pushed the entire iPhone line’s ASP (average selling price) up to a $695.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Apple’s unexpectedly strong numbers caused Wall Street’s doomsaying visionary sheep to suddenly tell rosier AAPL share price tales. In his piece “Apple analysts scramble,” Philip Elmer-DeWitt compiles the sudden changes of heart ands highlights a special apostate:

Most yardage covered: Colin Gillis of BGC Partners, who took his target all the way from $85 a share to $125—still behind the scrimmage line, but only a few bucks short of Thursday’s close ($128.53). (For more of Gillis’ backfield maneuvering, see my July 28, 2016 update.)

Apple’s recent numbers are worth a closer look, not just because they tell use what Apple has done, but because they give food for thought about what’s to come.

(For complete details, turn to Apple’s 10-Q SEC filing and pay particular attention the MD&A section—my favorite—starting on page 22. If you like graphs, Six Colors provides a very neat visual breakdown of the 10-Q in Apple’s record quarter by the numbers. You should also read the transcript of Apple’s earnings call, the source for most of the quotes, below, and look at Andrew Cunningham’s sensible analysis on ArsTechnica.

Before looking at Apple’s devices, let’s start with the intangibles: The Services category brought in $7.17 billion, a 18% increase (unless otherwise specified, all percentages are versus the same quarter last year). In the earnings call, Tim Cook mentions “over 150 million paid customer subscriptions,” and expects the Services business to be “the size of a Fortune 100 company this year,” with a goal “to double [its] size in the next four years.”

Apple’s services and devices (primarily iOS) are in a healthy and robust symbiotic relationship. As Apple’s services becomes richer and more varied, devices become more desirable and sales go up, which makes service and content providers more attracted to the platform, which drives up sales of devices…

We’ll hear more about services when Apple actually gets into the original content business, meaning doing what Netflix $NFLX and Amazon $AMZN already do. And where will that content come from? Perhaps tellingly, Cook had this to say about acquisitions just before he spoke about Apple’s plans for providing content [as always, edits and emphasis mine]:

[W]e are always looking at acquisitions. We acquired 15 to 20 companies per year for the last four years. And we look for companies of all sizes, and there’s not a size that we would not do based on just the size of it. It’s more about the strategic value of it.

For reference, Netflix’s latest quarterly letter to shareholders shows a small profit, $67 million, on $2.35 billion in revenue, and a negative Free Cash Flow of $639 million, this after 10 years of streaming.

* * *

Moving to the Mac: In a surprising reversal of the previous quarter, Mac revenue, $7.24 billion (+7%), beat Services by a hair. This was the Mac’s highest revenue number ever, with 5.37 million units sold (+1%).

A first observation: The Mac kept growing in a declining market, even as Apple had trouble meeting demand. As Cook said:

We were supply constrained for the new MacBook Pro throughout the December quarter and are just now coming into supply/demand balance.

Second, the ASP increased 6%, from $1,270 to $1,348. Cook also notes, in a dig at Microsoft $MSFT:

Our latest data shows most Mac customers are buying their first Mac, with the vast majority of them coming from a Windows PC.

It’d be nice to have some clarity on this “latest data,” but it’s clear that the noise surrounding the perplexing MacBook Pro launch didn’t deter customers. As Father Horace @asymco Dediu likes to tweet: “Every time an expert laughs, a cash register rings.”

* * *

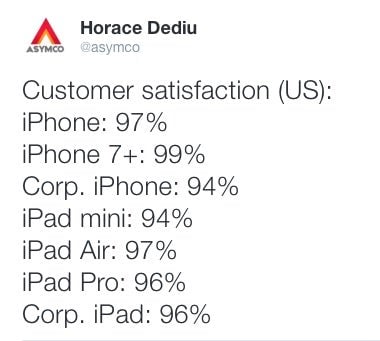

Down one device size, the iPad continues to lose altitude: $5.5 billion in revenue (-22%), with a negligible increase in ASP, $422 vs. $418. Despite the disappointing number, management continues to profess optimism regarding the iPad’s future, pointing to an “85% share of the US market for tablets priced above $200” and to very high customer satisfaction, as attested by Dediu’s extraction from the earnings call:

Cook’s assertion, twice repeated, of being “very bullish on the iPad beyond the 90-day clock,” leads one to assume there will be substantial changes to the iPad line in the not-too-distant future. Not just tweaks to the hardware—lighter, faster, a stylus holder—but something that fulfills Cook’s proclamation that the iPad is “the clearest expression of our vision of the future of personal computing.” Perhaps we’ll see new iPad hardware and software at Apple’s yearly Developer Conference, traditionally held in early June.

* * *

Down still another size: iPhones. As noted, they make up 69% of the company’s revenue, a weight some find excessive, proof that Apple is too iPhone-centric. This is ignoring the simple facts that there has never has been a product category like the smartphone, which is on its way to equipping two billion people, and there has never been a success like the iPhone, which will soon pass the trillion dollar revenue mark.

Here too, management professes optimism about the product and sees the market as “still in the early innings of the game.” This might be especially true for Apple as the company has avoided the race to the bottom. It continues to position the iPhone as an aspirational product, one that users of cheaper devices want to own, when their circumstances improve.

The iPhone 7 wasn’t without its detractors (as usual). Recall the aggressive blogosphere reactions to the removal of the analog headphone jack: “Taking the headphone jack off phones is user-hostile and stupid. Have some dignity.” But yet again, as Horace said, the cash register kept ringing. (That said, Apple management’s characterization of the change as “courageous” was unseemly, revealing an unfortunate frame of mind that I hope has been reexamined.)

* * *

Smaller still: the Apple Watch. As usual, no numbers. We have to resort to Apple’s professed satisfaction:

It was also our best quarter ever for Apple Watch, both units and revenues, with holiday demand so strong that we couldn’t make enough… best-selling smartwatch in the world and also the most loved, with the highest customer satisfaction in its category by a wide margin.

Somewhat reliable numbers are provided by Strategy Analytics, putting last quarter’s volume at 5,2 million units and a 63% market share.

Last year, Apple claimed to be the world’s number two watchmaker, second only to the Rolex group. I personally don’t think that’s as important as being the number one smartwatch maker. Long-time lovers of traditional watch brands, Rolex, Omega, and many others, aren’t ready to ditch their jewelry and mechanical marvels.

The fate of Apple’s smartwatch competitors is more revealing. The most notable, Fitbit, plans to lay off about 110 people after it saw its shares plunge by 17% following disappointing Holiday sales. Pebble, an interesting maker of simple, inexpensive watches was acquired… by Fitbit.

A more ignominious fate awaited Basis. Acquired by Intel $INTC for more than $100 million in 2014, its watches were recalled for overheating in Aug. 2016, and service to Basis owners was terminated last December.

Android Wear watches haven’t taken the world by storm, in spite of being promoted by powerful players such as Samsung, LG, and Huawei. This might change as Google $GOOGL and its partners are about to push out new software and hardware as soon as this week. Google has the financial and technical wherewithal to keep the effort going, as do its best partners…but only if they see sufficient sales volume.

The latter question reminds us of the hype surrounding the Apple Watch introduction. Exaggerating just a little, this was going to be Apple’s Next Big Thing. Heralded by celebrity-studded events in the US and in Europe, the hype hasn’t paid off, at least not yet. Today, Apple has refocused its Watch efforts on Health and Fitness, an area where Apple, with its ability to couple hardware and software, has a significant advantage over Google. We’ll have to see if future hardware iterations will bring new sensors, greater computing power without draining the battery, and make the Watch less dependent on the iPhone.

* * *

Last on the size scale, the AirPods. They’re still hard to come by, the Apple site says “six weeks.” Luckily, I placed an order through the French Apple site minutes after the US site had sold out. A competent and pleasant Austin-based Apple employee helped me navigate credit card straits over the phone, and my AirPods were delivered on Dec. 20, in time for the family Xmas reunion. They’re as good as advertised—good sound, no Bluetooth headaches—and the tiny white container is small enough to be carried in your pants pockets. Availability aside, an unmitigated success.

At the end of this lengthy if incomplete survey, one thought imposes itself: Apple plays the long game and seems to play it well.

A reliable measure of Apple’s ambitious expectations is its R&D expense: It keeps climbing, 19% higher than last year. Another sign can be found in the Off-Balance Sheet section of the 10-Q. This year, Apple has committed $24 billion in manufacturing purchase obligations—money promised to suppliers. That’s a 16% increase over last year’s $20.7 billion. This doesn’t mean that the company’s output will increase by a similar amount, but it’s always a reliable trend indicator. For example, we saw the same number go down from $21.6 billion in Dec. 2014, to $20.7 billion in 2015, a timeframe in which Apple revenue also declined.

I’ll conclude with a fun but profound epigram from Benedict Evans, who thinks he’s found Apple’s long game plan: