Update (3:26 PM ET): Portugal’s governing coalition today saw its second major loss in two days, as Paulo Portas, the foreign minister and leader of the Democratic and Social Center-People’s Party (CDS-PP), tendered his resignation.

Meanwhile, EU authorities have given Greece three days to deliver on promises it’s made to the troika—the group composed of the International Monetary Fund (IMF), the European Central Bank, and representatives of European countries, which is monitoring the euro debt crisis.

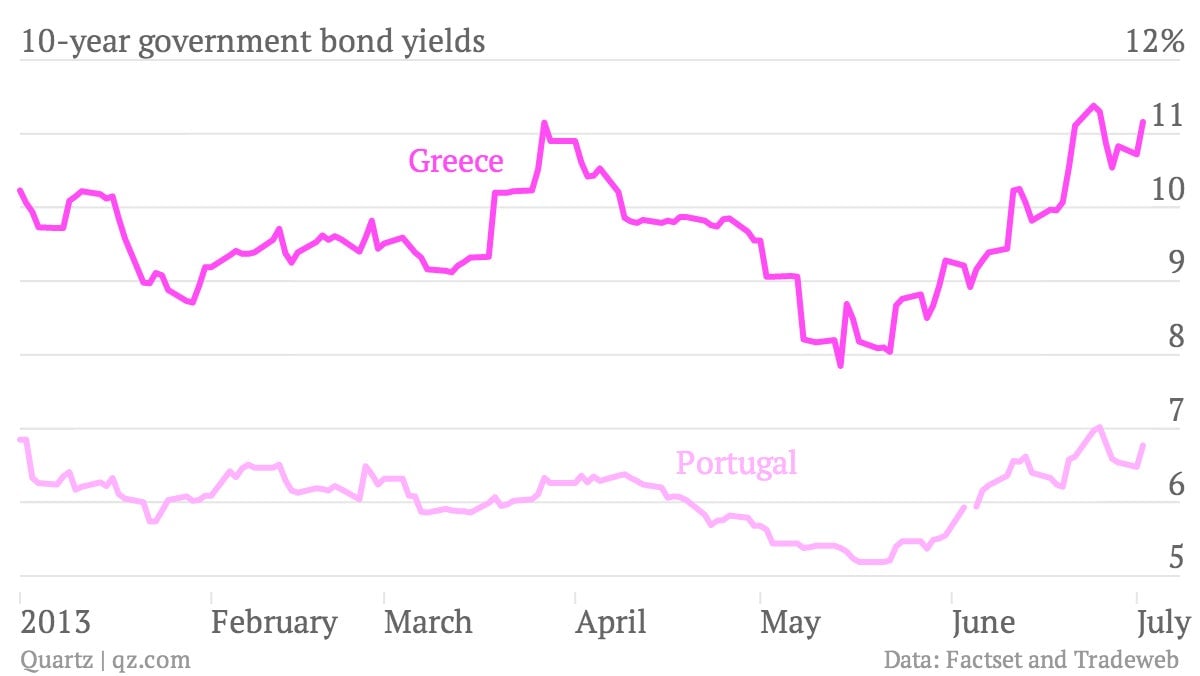

Clearly, Greece and Portugal are fighting to be the most scary country in the euro this week.

Portugal faces new political unrest with the loss of Portas and CDS-PP’s 24 votes in parliament. Although the failure of the coalition wouldn’t necessarily wrest government control from prime minister Pedro Passos Coelho’s Social Democratic (PSD) party, they would face deeper rivalry from other parties. Coelho didn’t accept Portas’s resignation, and said that he wouldn’t resign himself or call for new elections.

Portas’s resignation comes just on the heels of another: that of Portugal’s finance minister, Vitor Gaspar. An independent, Gaspar was one of the most vocal advocates of fiscal austerity, which has taken a toll on Portugal’s economy. Although he was quickly replaced, the move suggests even deeper unrest at the top.

Not to be outdone, Greece now faces an ultimatum from the troika, one it will have a hard time fulfilling. The IMF has promised that it will no longer cut euro-zone leaders any slack in meeting their commitments to Greece’s €240 billion ($313 billion) bailout plan, because doing so would violate the fund’s rules. So euro-zone officials, unhappy with the progress Greece has made on privatizing state-owned industries and laying off public-sector workers, is dropping a lot of the IMF’s burden over to Greece. It’s unclear exactly how much money the country will have to raise to satisfy its creditors, but some estimates peg the budget shortfall at €3-4 billion.

All in all, not such a great outlook for two of Europe’s weakest economies. That weakness has carried over to the yield on both countries’ sovereign bonds (i.e., the price each would have to pay if they borrowed in the open markets today).