The tantalizing future of robot taxis is just on the horizon, as self-driving cars are scheduled to hit the road as early as 2019. Money is going through a transition that could be just as revolutionary, as our finances may also soon be able to drive themselves, says Kenneth Lin, CEO of Credit Karma.

The tantalizing future of robot taxis is just on the horizon, as self-driving cars are scheduled to hit the road as early as 2019. Money is going through a transition that could be just as revolutionary, as our finances may also soon be able to drive themselves, says Kenneth Lin, CEO of Credit Karma.

Lin thinks “autonomous finance” could come about in the next five or so years. And eventually, all of our most important financial decisions could be automated without asking for permission. After all, do you know the best time to refinance your mortgage (and where to get it)? Your student loan? Your car loan? Me neither.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

He envisions a time when computers refinance our debts when it’s most advantageous, while investing our cash into longer-term investments (and rebalancing them) when it makes sense. Life insurance and other protections would be on autopilot. The technology has its roots in the fintech projects cropping up now.

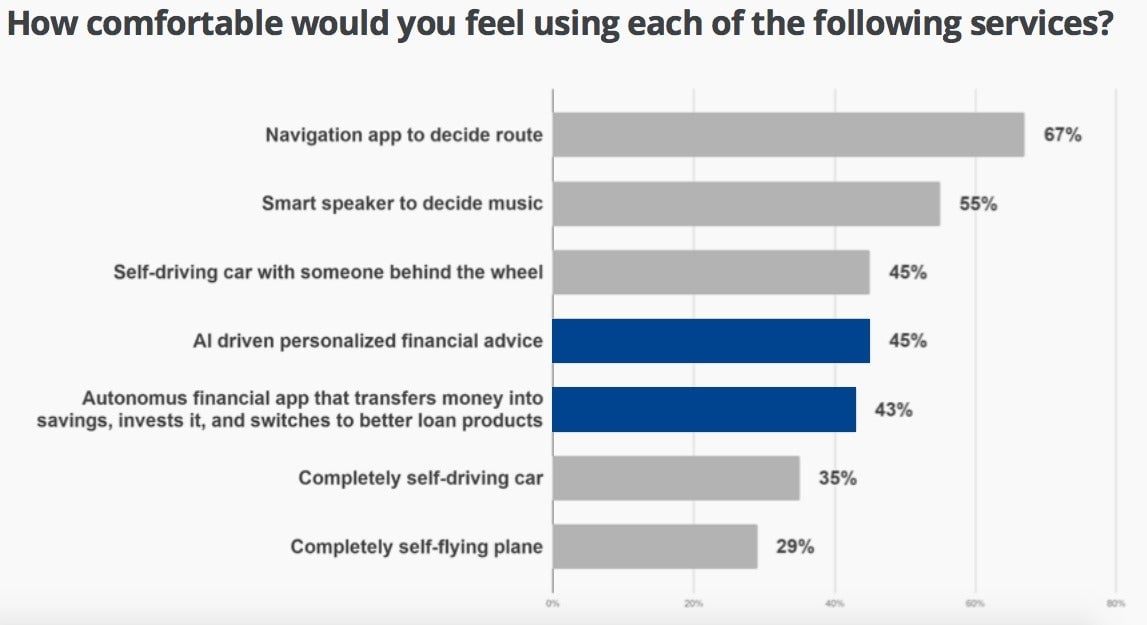

American overspending on auto loans amounted to $37 billion last year, according to a Credit Karma presentation at MoneyConf in Dublin. For home mortgages, that amount comes to almost $100 billion. Consumers, meanwhile, are more comfortable with autonomous financial advice than they are fully self-driving cars and planes. (Yet we are strangely controlling when it comes to music selection.)

Wealthfront, a robo advisor, is pursuing a future similar to Lin’s vision. CEO Andy Rachleff said this week at a CB Insights conference that the company wants to automate all of its customers’ finances. A client could one day deposit her paycheck with Wealthfront and the company would take care of just about everything else from there.

This brighter, better future seems pretty Utopian, which of course means it’s not assured. With every industry where automation is proliferating, the cyber risk will have to be contained if consumers are going to trust it, for example.

Robo advisors managed $98.5 billion in 2016, more than double the year before, according to Charles Schwab $SCHW, which has a robo service. Schwab predicts the segment’s assets will climb to $460 billion by 2020. That compares with Edward Jones, a 96-year-old incumbent with around 20,000 advisors, that managed some $1 trillion as of October. In a sign that algorithms may not have been wooing enough new customers, Betterment, originally an all-digital service (paywall), added a human advisor option last year.

But Lin thinks these concerns are manageable and that self-driving finance isn’t even that radical. Just as wealthy people have long enjoyed chauffeurs to drive them around, the elite have also benefitted from specialized financial advice to help them get the most out of their money.

If all goes well, ordinary people will soon have the benefit of optimized finances. If so, some of us might find we have enough extra cash for that self-driving car.

June 15: A philosopher thinks technology could make anarchists’ dreams come true